Make a Payment

850-572-3443

Divorce can be a challenging process, especially when it comes to dividing property. At Christine Sue Cook, LLC, we understand the complexities involved in creating a fair divorce property division agreement.

Our goal is to help you navigate this process with clarity and confidence, ensuring that your rights and interests are protected throughout the negotiation.

Equitable distribution is a legal term that describes the process of dividing marital property and debt in the event of a divorce. It’s important to note that equitable doesn’t always mean equal. Instead, it aims for fairness.

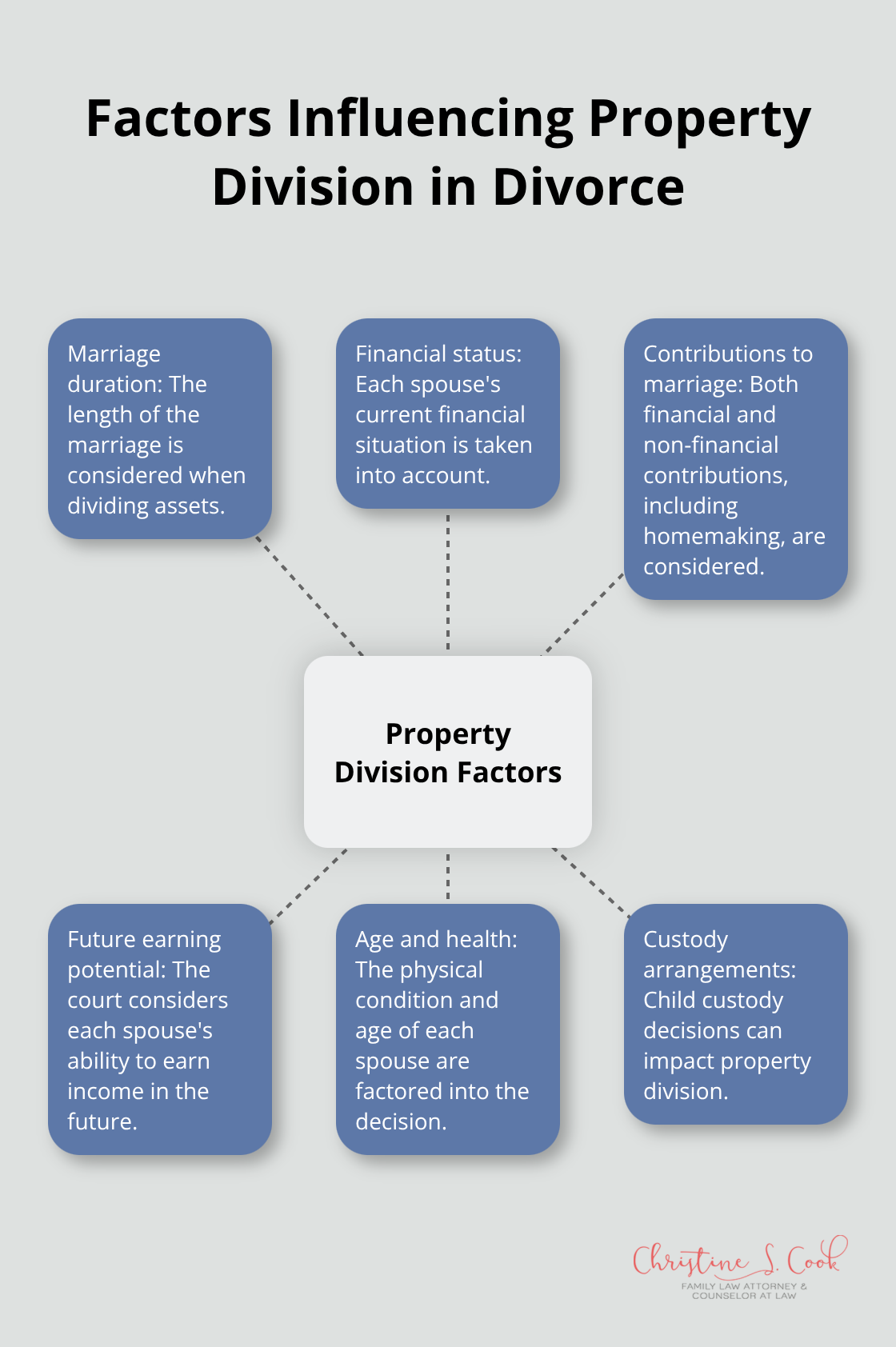

Courts weigh various factors to determine a fair division of assets. These typically include:

For instance, if one spouse sacrificed their career to raise children, a court might award them a larger share of assets to offset lost earning potential.

The distinction between marital and separate property plays a key role in equitable distribution. Marital property generally encompasses all assets acquired during the marriage, regardless of the purchaser. This can include homes, cars, retirement accounts, and even businesses started within the marriage.

Separate property typically includes:

However, separate property can transform into marital property if it’s commingled or used for the marriage’s benefit. For example, an inheritance used to renovate the family home may be considered marital property.

The classification of property can become complex, especially in long-term marriages or when assets have been commingled. Some common challenges include:

Prenuptial agreements allow spouses to override certain default marital property laws, but not all aspects of state law can be waived. These contracts (often signed before marriage) can outline how assets will be divided, potentially impacting state equitable distribution laws.

As we move forward, we’ll explore the steps to create a fair property division agreement, ensuring both parties’ interests are protected throughout the negotiation process.

The first step to create a fair property division agreement is to compile a detailed list of all assets and debts. This includes obvious items like houses and cars, as well as less apparent ones such as retirement accounts, investments, and even frequent flyer miles. Don’t overlook debts like mortgages, credit card balances, and personal loans.

A study by the Institute for Divorce Financial Analysts found that 22% of divorcing couples overlook assets during property division. To avoid this pitfall, we recommend the use of financial software or collaboration with a financial advisor to ensure a complete inventory.

After compiling a complete inventory, it’s essential to determine the accurate value of each asset. This often requires professional assistance. The National Association of Certified Valuators and Analysts reports that business valuations can vary by up to 30% depending on the method used.

For real estate, obtain a current appraisal. For complex assets (like businesses or stock options), consult with a financial expert. The goal is to establish a clear, agreed-upon value for each item to facilitate fair division.

The tax consequences of property division can significantly impact the true value of what you receive. A survey by the American Academy of Matrimonial Lawyers reveals that 62% of divorce attorneys say tax issues are often overlooked in property settlements.

For instance, selling a house might trigger capital gains tax, while liquidating a 401(k) could result in early withdrawal penalties. We always advise our clients to consult with a tax professional to fully understand these implications.

With a clear picture of assets, their values, and tax implications, you’re ready to negotiate. This can occur directly with your spouse, through attorneys, or with a mediator. Effective negotiating during mediation sessions can help you achieve the outcome you want in your legal separation.

When negotiating, focus on your long-term financial security rather than short-term gains. Consider factors like liquidity, future value, and maintenance costs of assets. For example, keeping the family home might seem appealing, but it could become a financial burden if you can’t afford the mortgage and upkeep.

At times, traditional division methods may not yield satisfactory results. In such cases, try to think outside the box. For instance, if one spouse wants to keep the family business, they might offer a larger share of other assets or agree to a longer-term payout to the other spouse.

Some couples opt for a “bird’s nest” custody arrangement where children stay in the family home while parents rotate in and out. This approach can help maintain stability for children while allowing for a more flexible property division.

As we move forward, we’ll explore common challenges that arise during property division and how to address them effectively.

The division of family-owned businesses in divorce requires accurate valuations. We recommend the engagement of a certified business appraiser to conduct a thorough assessment. An accurate and unbiased business valuation is essential to ensure that both parties receive their fair share of the marital property. This process typically involves the analysis of financial statements, market conditions, and future earning potential.

The division of pensions and retirement accounts often requires specialized knowledge of tax laws and regulations. A Qualified Domestic Relations Order (QDRO) is often necessary to divide these accounts without incurring early withdrawal penalties. A QDRO is a judgment, decree or order for a retirement plan to pay child support, alimony or marital property rights to a spouse, former spouse, child or other dependent.

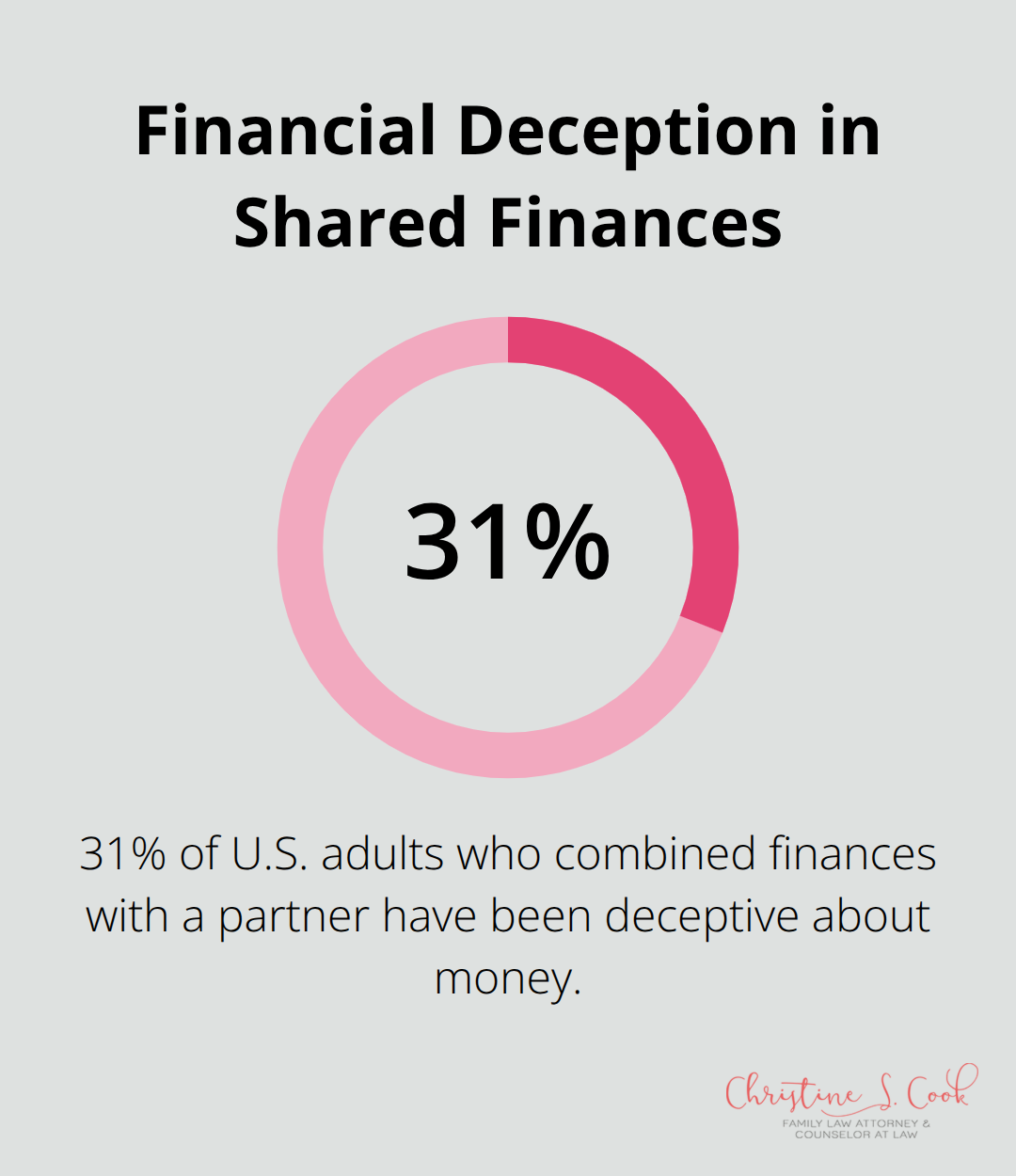

Some spouses attempt to conceal assets during divorce proceedings. The National Endowment for Financial Education found that 31% of U.S. adults who combined finances with a partner have been deceptive about money. Various strategies can uncover hidden assets, including:

Emotional ties to certain assets, particularly the family home, can complicate negotiations. While understandable, these attachments can lead to financially unsound decisions. It’s important to consider the long-term financial implications of keeping emotionally significant assets.

The division of marital debt is often as contentious as asset division. Experian reports that the average American carries $90,460 in debt. In divorce, this debt must be equitably distributed. We advise clients to obtain a comprehensive credit report to ensure all debts are accounted for. It’s important to address joint debts and potentially refinance them in one spouse’s name to protect both parties’ credit scores post-divorce.

Creating a fair divorce property division agreement requires careful consideration and professional guidance. An experienced attorney can help you understand your rights, identify assets and debts, and negotiate effectively on your behalf. A well-crafted agreement provides financial security and peace of mind for both parties as they move forward.

At Christine S. Cook, LLC, we specialize in helping clients navigate the complexities of divorce property division agreements. Our approach combines legal expertise with a deep understanding of the emotional and financial challenges involved in divorce. We work to protect our clients’ rights and achieve the best possible outcome in their property division negotiations.

We offer a range of services to support you through this process, from initial consultations to mediation and court representation (if necessary). Don’t navigate this complex process alone. Contact Christine S. Cook, LLC for expert guidance and compassionate support as you secure your financial future.