Marriage doesn’t have to end in divorce to create financial separation. Legal separation offers a structured path to protect your assets, clarify financial responsibilities, and establish clear boundaries while keeping your marriage technically intact.

At Christine Sue Cook, LLC, we help clients understand this often-overlooked option. Whether you’re concerned about debt protection, asset division, or maintaining specific legal status, this guide walks you through what you need to know.

Legal separation and divorce are fundamentally different in one critical way: legal separation keeps you married while divorce ends the marriage entirely. This distinction matters far more than most people realize. In a legal separation, you remain married in the eyes of the law, which means you cannot remarry, but you gain the financial protections and clarity of a formal court order. A divorce, by contrast, severs all legal ties and allows you to remarry. The real advantage of legal separation is that it provides a binding agreement on asset division, debt allocation, and support payments without the finality of divorce. If circumstances change or you want to reconcile, legal separation provides a bridge that divorce does not.

California and many other states recognize legal separation as equally enforceable as divorce when it comes to property division and support obligations. The court-ordered framework is what makes this work-informal separation without legal documentation leaves both parties vulnerable to disputes years later. Income earned or debt incurred during separation may still be considered part of the marital estate. One spouse can spend marital assets on a new partner during an informal separation, and without a formal interim agreement, the other spouse may have no recourse. This is why you should formalize terms quickly, even before considering divorce, to protect your long-term interests.

A legal separation order divides assets and debts according to state law, typically community property rules in states like California. The separation date becomes the anchor point-everything acquired before that date is divided according to the court’s judgment, and everything after belongs to the person who earned or acquired it. This clarity eliminates years of ambiguity. Your separate bank accounts, retirement funds, and property titles are clearly documented and legally yours. Spousal support and child support, if applicable, are spelled out in enforceable terms rather than left to informal understanding.

The American Bar Association recommends that you inventory all assets and debts for each person and document them in a formal plan, which is exactly what a legal separation accomplishes through the court. You must update beneficiary designations on life insurance and retirement accounts to reflect your separation, preventing your ex-spouse from inheriting assets you intended elsewhere. Your wills, trusts, and powers of attorney require review and rewriting to match your new financial reality. Without these formal steps, a spouse who dies during an informal separation may have their estate distributed to someone they no longer intended to benefit.

Your state’s specific requirements determine how you proceed. Some states require you to live apart for a set period before legal separation is finalized, while others allow separation without physical separation. California allows you to achieve financial separation through a judgment that divides property and debt without requiring divorce, but the process still requires filing a petition, serving your spouse, and completing financial disclosures like forms FL-160 and FL-150. The petition must outline marriage details, grounds for separation, and issues like custody and property division. Your spouse then responds, followed by negotiation to settle property, debts, and support. Once both parties agree, the court approves the separation agreement, though some jurisdictions do not require a formal hearing if the agreement is uncontested.

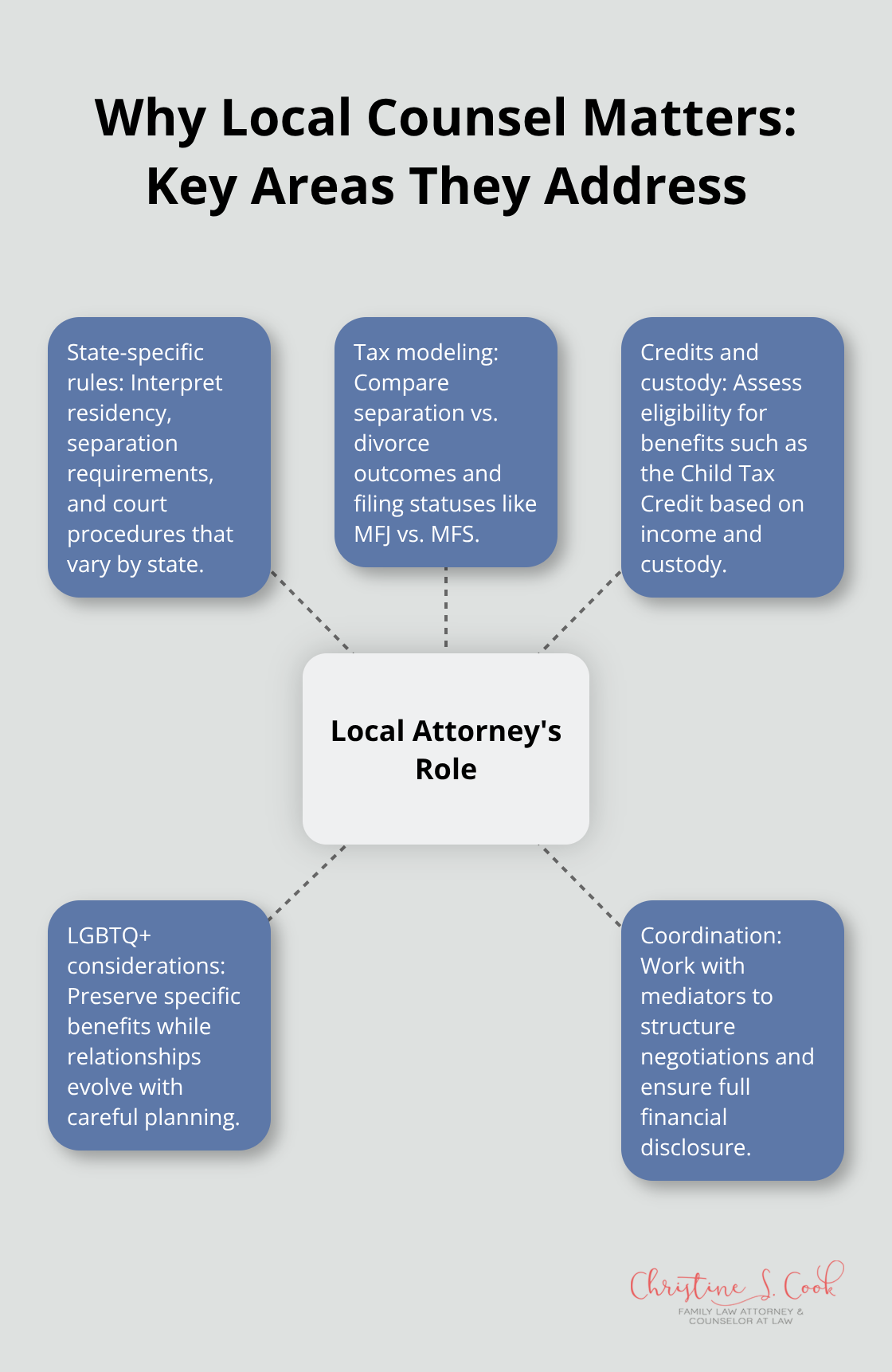

This is why you should consult a family law attorney experienced in your jurisdiction-the rules differ enough that what works in one state may not work in another. An attorney can model the tax implications of separation versus divorce, compare filing status options like Married Filing Jointly versus Married Filing Separately, and show whether certain credits like the Child Tax Credit still apply to your situation. They can also address LGBTQ+ specific concerns, such as staying married to retain certain benefits while your relationship evolves, which requires careful legal and financial planning that only a local attorney can properly advise.

Understanding these legal distinctions positions you to make informed decisions about your financial future. The next section examines the specific financial considerations that arise during legal separation and how to protect yourself in each area.

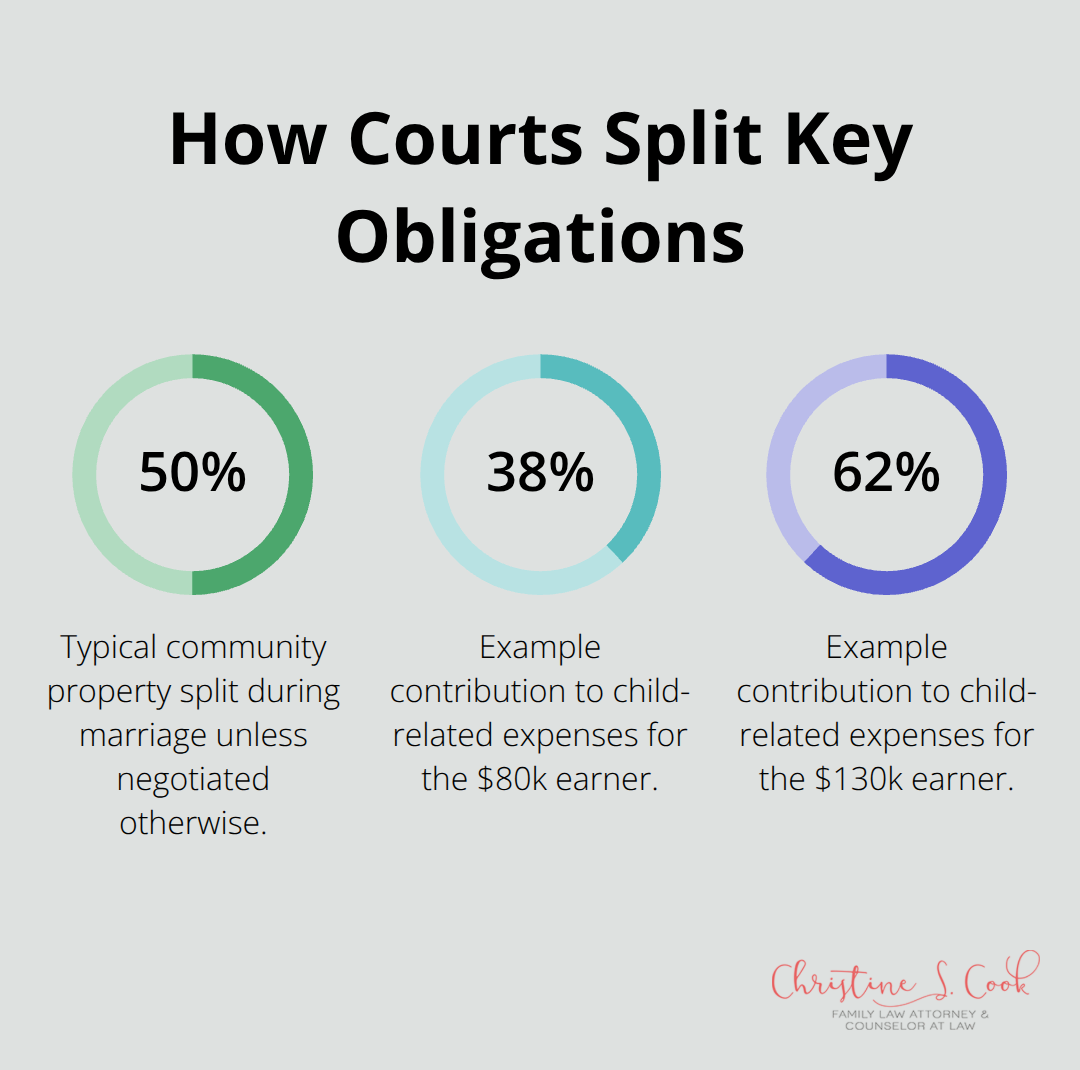

Legal separation forces you to confront financial realities that informal arrangements let you avoid. When the court divides your assets and debts, it doesn’t make the obligations disappear-it allocates them to each spouse. California’s community property rules mean that most assets acquired during marriage split 50/50 unless you negotiated otherwise, and the separation date matters enormously because it determines what counts as marital property. Everything you earned or acquired before the separation date gets divided; everything after belongs to you alone. This timing protects you from years of ambiguity. A spouse earning significantly more income during an informal separation without a formal interim agreement may see those earnings treated as marital property later, with no credit for contributions made by the lower-earning spouse.

The Consumer Financial Protection Bureau recommends building separate emergency funds for each person, which forces you to calculate what financial independence actually costs. Most people underestimate this number substantially. If you earn $80,000 annually and your spouse earns $130,000, a 50/50 split means you’re planning a household budget on roughly $105,000 combined instead of $130,000, and spousal support helps bridge that gap only if the court orders it. Many couples discover during legal separation that they’ve been subsidizing each other’s spending without realizing it-one spouse’s discretionary purchases were offset by the other’s income, masking the true cost of maintaining two households. A formal separation agreement exposes this immediately.

Spousal support in legal separation follows the same rules as in divorce, and it’s far from automatic. The court considers the length of your marriage, each spouse’s earning capacity, the standard of living during marriage, and whether one spouse sacrificed career opportunities to support the family. A marriage lasting less than ten years typically results in support lasting half the marriage length, though this varies by state. If you earn $80,000 and your spouse earns $130,000, you’re expected to contribute roughly 38 percent of child-related expenses while your spouse covers 62 percent.

The American Academy of Pediatrics emphasizes that you should budget for education, activities, and ongoing costs while communicating openly with your spouse about these expenses. You must update beneficiary designations on retirement accounts and life insurance policies within days of separation, not months later, because a spouse who dies intestate during separation may have their estate distributed according to old designations. The Internal Revenue Service allows you to claim the Child Tax Credit even while separated if you meet income and custody requirements, but this only works if you file taxes correctly and maintain proper documentation of custody arrangements.

Without a court order, you leave yourself vulnerable to disputes that could have been prevented. A spouse can spend marital assets on a new partner during an informal separation, and without a formal interim agreement, the other spouse may have no recourse. The American Bar Association recommends that you inventory all assets and debts for each person and document them in a formal plan, which is exactly what a legal separation accomplishes through the court. Your wills, trusts, and powers of attorney require review and rewriting to match your new financial reality. Without these formal steps, a spouse who dies during an informal separation may have their estate distributed to someone they no longer intended to benefit.

These financial obligations shape how you move forward, but they’re only part of the picture. The next section examines the specific steps you take to navigate legal separation successfully and protect your interests throughout the process.

You cannot navigate legal separation without concrete financial records, and most people delay this step far longer than they should. Start by collecting every document that proves ownership, debt, and income: bank statements covering the past three years, investment account statements, retirement account statements showing balances and beneficiary designations, mortgage documents, property deeds and titles, credit card statements, loan agreements, tax returns for the past three years, and pay stubs from the past six months. The American Bar Association emphasizes that you inventory all assets and debts for each person and document them in a formal plan, which is exactly what the court requires anyway. Do not wait for your spouse to produce these documents during discovery-obtain your own copies immediately from your financial institutions. A spouse with volatile income during separation can claim whatever income suits them without documentation to contradict it, which is why you need copies now, not later.

Once you have these documents, organize them by category and calculate your net worth: total assets minus total debts. This number becomes your baseline for negotiation and protection. You should also monitor your credit reports annually during separation to prevent your spouse from opening accounts in joint names or damaging your credit through negligence. The Federal Trade Commission recommends this step as essential protection during financial transitions. Create a spreadsheet that lists each asset with its current value, each debt with its balance and interest rate, and the date you acquired or incurred each item. This organization takes time but prevents disputes later when one spouse claims they forgot about an account or underestimated a debt’s value.

Hiring a family law attorney experienced in your state is not optional, despite the cost. Your attorney reviews your financial documents, identifies assets you may have overlooked, and advises whether your state’s rules favor legal separation over divorce in your specific situation. A tax professional should work alongside your attorney to model the implications of your filing status, since tax considerations can exceed thousands of dollars annually depending on income levels and the presence of children. Christine S. Cook, LLC, based in Pensacola, Florida, offers expert legal services in family law and provides compassionate solutions tailored to your specific circumstances. The firm utilizes collaborative law techniques to achieve amicable settlements and offers aggressive court representation when necessary.

Negotiating agreements outside of court works only when both parties act in good faith and understand the financial stakes clearly. Many couples attempt informal negotiation first, then discover months later that one spouse withheld information or made assumptions about shared expenses that the other spouse disputes. A mediator or collaborative divorce attorney prevents this by structuring the negotiation process and holding both parties accountable to full financial disclosure. Write down every financial agreement in a formal interim agreement before separation begins-do not rely on verbal promises or text messages. This document should specify how you handle shared expenses, how you split joint accounts, and what happens to marital assets during the separation period. Courts recognize written interim agreements as evidence of the parties’ intent, which protects you if disputes arise later.

Legal separation without divorce offers a structured alternative that protects your assets while keeping your marriage technically intact. Unlike informal separation, which leaves both parties vulnerable to disputes over assets, debts, and support obligations, a court-ordered legal separation provides enforceable protections that last. You remain married, which preserves certain benefits and allows space for reconciliation, while your finances are clearly divided according to state law.

The path forward requires three concrete steps: gather your financial documentation immediately (bank statements, investment accounts, property deeds, and tax returns), hire a family law attorney in your state who understands local requirements, and formalize your separation agreement in writing rather than relying on verbal promises. A written interim agreement protects both parties by documenting how you handle shared expenses, joint accounts, and asset division during the separation period. Financial separation without divorce works because it forces clarity where informal arrangements create ambiguity.

Christine S. Cook, LLC, based in Pensacola, Florida, specializes in helping clients navigate these decisions with compassionate guidance and legal expertise. Contact us for a free consultation to discuss your specific situation without financial pressure and understand your options before committing to any path.