Blended families face estate planning challenges that traditional wills simply don’t address. When you remarry, your assets, children, and wishes become more complex-and one wrong move can leave your family fighting in court instead of grieving together.

At Christine Sue Cook, LLC, we’ve seen how Florida blended family planning requires a completely different approach than standard estate plans. The good news is that with the right tools and strategy, you can protect everyone you care about.

When a second marriage happens, most people assume their existing will or a simple update covers everything. This assumption costs families thousands in court fees and emotional damage. Under Florida intestate succession laws, a surviving spouse in a blended family can receive one-half of a deceased spouse’s estate, with the remainder passing to the deceased spouse’s descendants. That sounds straightforward until you realize it forces a division that may not reflect your actual wishes. If you have children from a prior marriage and want them protected, a will alone leaves them vulnerable to probate delays, contested claims, and your surviving spouse’s legal rights to challenge distributions. Standard estate plans treat all families the same, but blended families need something fundamentally different because competing interests exist from day one.

The core problem is timing and control. Without a revocable living trust, your assets enter probate when you die, which means your surviving spouse and adult children from your first marriage all have a say in how things unfold. In Florida, probate is guaranteed for assets not held in a trust or with a beneficiary designation, so a will alone does not avoid probate. Most Floridians use revocable living trusts to condition inheritances and shield their assets from probate. Your executor may face pressure from both sides of your family, and if your surviving spouse disagrees with your children about distributions, the court becomes the referee. One real-world example involved seven siblings serving as co-executors, which led to months of delays and permanently damaged relationships. A trust-based plan sidesteps this chaos because it keeps your wishes private and removes ambiguity about who gets what and when.

Beyond trusts, beneficiary designations on life insurance, retirement accounts, and annuities pass outside your will entirely, which means they can contradict your overall plan if you haven’t updated them. Many people name an ex-spouse or forget to update these forms after remarriage, accidentally leaving assets to the wrong person. Prenuptial or postnuptial agreements also serve a practical function by clarifying asset treatment upfront, reducing the chance that your surviving spouse challenges your children’s inheritance later. Without these tools working together, your blended family inherits conflict instead of clarity-and that’s where the right legal strategy makes all the difference. The next section explores the specific estate planning tools that actually work for blended households in Florida.

A revocable living trust forms the foundation of effective blended family planning in Florida because it removes your assets from probate entirely while you retain complete control during your lifetime. When you place property into a trust, your surviving spouse can receive income and use assets during their life, while your children from a prior marriage receive the remainder after your spouse passes. This structure solves the core problem that wills create: it prevents your estate from entering probate, where your spouse and adult children would fight over distributions and your personal wishes could be overridden by Florida law. The trust document itself remains private, so family members don’t see the details of who gets what, which reduces resentment and disputes. You can specify exactly how much your surviving spouse receives, whether they can access the principal or only income, and when your children inherit. If your spouse dies before you, the trust assets pass directly to your children without needing any adjustments or court involvement. This flexibility makes revocable living trusts far superior to wills for blended households because they handle competing interests without forcing a one-size-fits-all division.

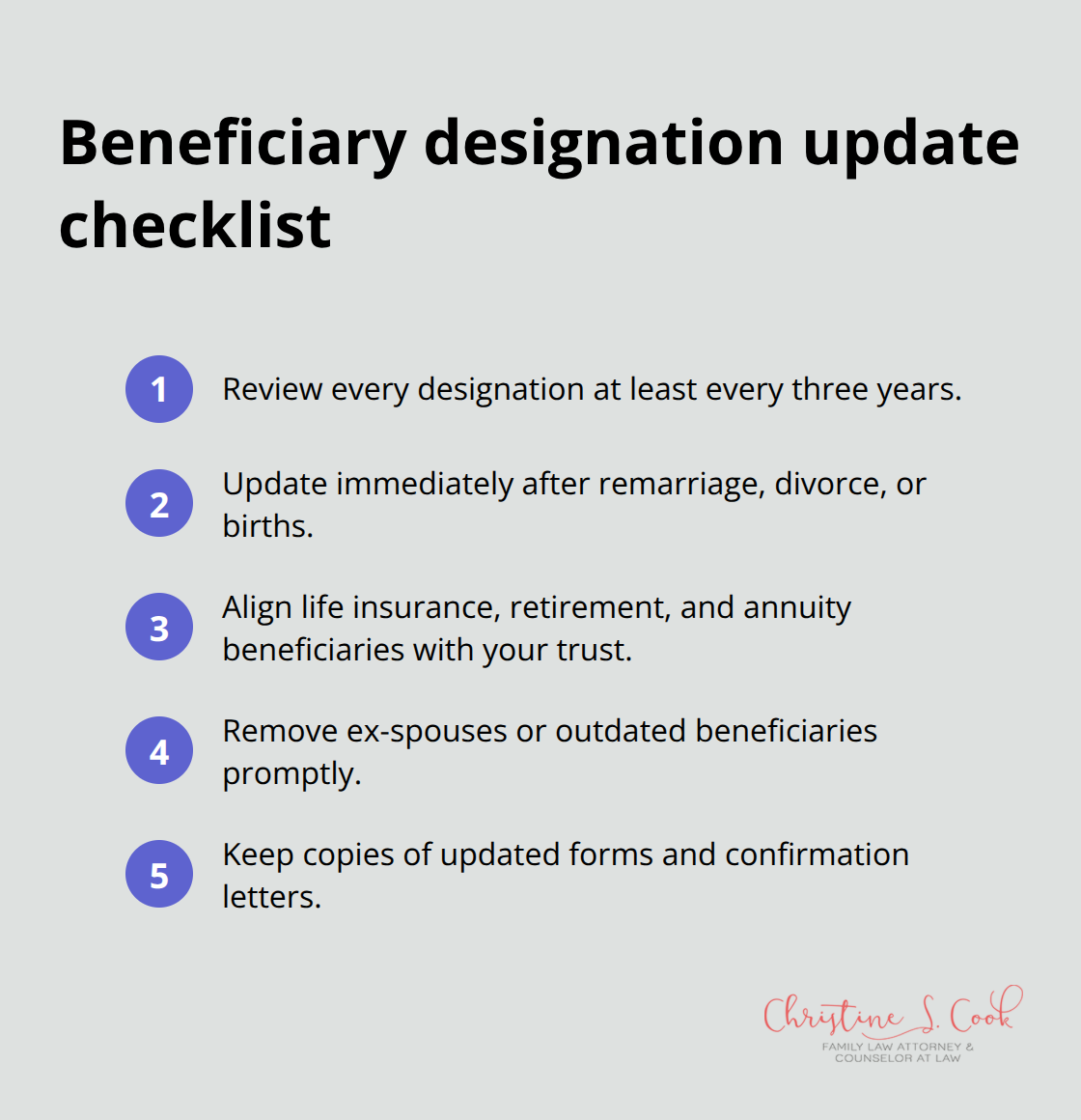

Beneficiary designations on life insurance policies, retirement accounts like 401(k)s and IRAs, and annuities bypass your trust and will entirely, which means they can either support your overall plan or completely undermine it. Many people fail to update these forms after remarriage, accidentally naming an ex-spouse or an outdated beneficiary, and once that person dies, the insurance company pays them first and asks questions later. If you have a life insurance policy with your ex-spouse listed as beneficiary and you remarry, that ex receives the full amount when you die, leaving your new spouse and children with nothing from that asset. The solution is straightforward: review every beneficiary designation at least every three years or immediately after remarriage, divorce, or the birth of children or grandchildren. Coordinate these designations with your trust so that life insurance, retirement accounts, and annuities all feed into your overall strategy rather than working against it.

Prenuptial and postnuptial agreements serve a different but equally important function by clarifying upfront whether certain assets remain separate property, whether your spouse waives rights to your children’s inheritance, or whether you each maintain separate estates. A postnuptial agreement signed after remarriage carries the same legal weight as a prenuptial agreement in Florida and can prevent your surviving spouse from using elective share laws to claim a larger portion of your estate than you intended. These agreements work best when both spouses have separate legal counsel and when they reflect genuine negotiation rather than pressure, because Florida courts will scrutinize them if anyone later claims they were unfair.

Together, trusts, updated beneficiary designations, and written agreements create a coordinated defense against the chaos that blended families face. Your assets reach the people you actually want to support, and your surviving spouse receives the protection they need without accidentally disinheriting your children. The next section examines how Florida’s specific laws-particularly homestead protections and inheritance rules-interact with these tools to either strengthen or complicate your blended family plan.

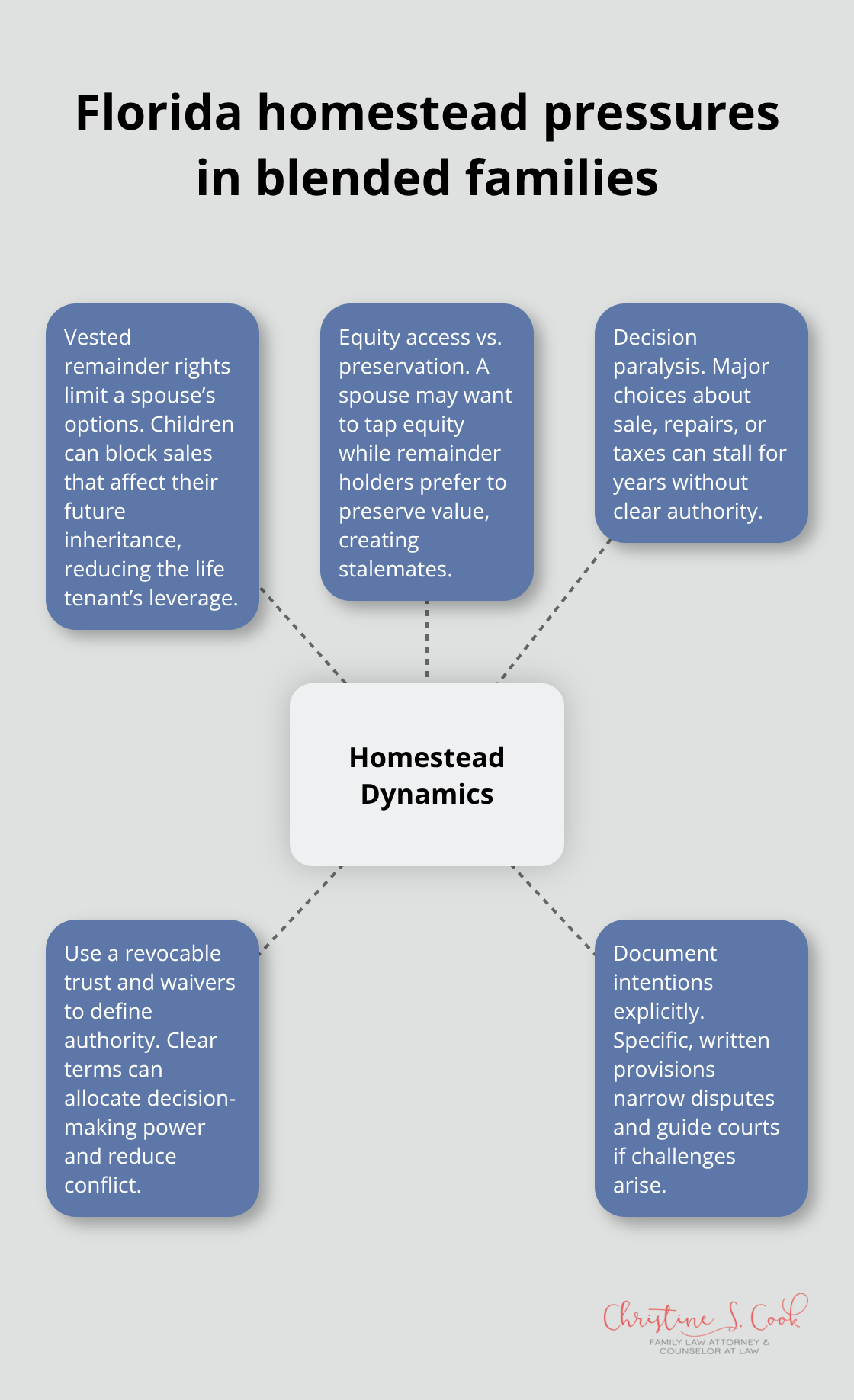

Florida’s homestead laws create three separate layers of protection that directly affect how your blended family estate plan must be structured. The first layer, called the Save Our Homes exemption, caps annual increases in your home’s assessed value at 3 percent or the inflation rate, whichever is lower. This tax benefit protects your wallet during your lifetime, but it becomes a major planning issue when you die because Florida law automatically grants your surviving spouse a life estate in the homestead if you have descendants. That means your spouse can live in the home for the rest of their life, but your children from a prior marriage own the remainder interest and must agree to any sale or major changes.

This structure sounds protective until you realize that a life tenant and remainder holders often have conflicting interests. If your spouse wants to sell the home to downsize and your children want to preserve it for eventual inheritance, Florida law gives your spouse limited leverage because the children’s remainder rights are vested and cannot be easily overridden. The tension between these two positions can paralyze major decisions about the property for years. Your spouse may want to access the home’s equity, while your children resist any sale that reduces their eventual inheritance.

Neither party has clear authority to act alone, which means even routine maintenance or necessary repairs can become sources of conflict.

The second layer, automatic creditor protection, shields your homestead from most creditors within size limits: up to half an acre inside city limits and 160 acres outside municipalities. This protection is powerful during your lifetime, but it does not prevent your surviving spouse from claiming elective share rights to the home itself. The third layer involves devise rules, which are the automatic inheritance rules that activate at your death. If you have minor children, your spouse receives only a life estate regardless of what your will or trust says, and your minor children automatically inherit the remainder. If you have only adult children, your spouse can elect to take either the entire homestead or a half-interest with your children receiving the other half. These automatic rules override your stated wishes unless your spouse waives their rights before your death, which requires a separate legal document and is not always possible or advisable.

The practical solution for blended families is to title your homestead in a revocable living trust and have your spouse waive their devise rights before the homestead is placed in the trust. This approach gives you complete control over whether your spouse receives a life estate, a fee simple interest, or something in between, and it prevents Florida’s automatic rules from forcing an unwanted division. Without this step, your blended family faces a scenario where your surviving spouse holds a life estate that blocks your children’s access to the home’s value and creates ongoing tension over maintenance costs, property taxes, and the possibility of sale. Florida courts have consistently upheld these homestead rules even when they contradict a deceased person’s clear written wishes, so proactive planning is not optional for blended households.

If you own multiple homes in Florida or split time between Florida and another state, the homestead designation itself becomes critical because only one property per person can qualify for homestead protection in any given year. Couples who winter in one location and summer in another must carefully track which property claims homestead status to avoid losing the Save Our Homes tax benefit or creating confusion about which home falls under devise protections. Florida intestacy law gives surviving spouses substantial rights that can eclipse your children’s inheritance unless you have a trust-based plan in place. If you die without a will or trust, your surviving spouse receives half your estate and your children split the other half, regardless of how long you have been married or how much you intended each group to receive. Blended families cannot rely on intestacy rules because those rules treat all spouses equally and all children equally, which rarely reflects the actual family structure or financial realities of a second marriage.

Courts in Florida have become increasingly active in interpreting blended family estate planning disputes when plans are ambiguous or when family members claim undue influence, fraud, or lack of capacity. The clearer and more specific your planning documents are, the less room exists for relatives to argue about your intentions. Courts strongly prefer written, contemporaneous documentation over testimony from family members about what they think you wanted, so a detailed trust document that explicitly addresses your blended family structure and your wishes for both your spouse and your children carries far more weight than a simple will or generic trust template.

Blended family estate planning in Florida requires coordinated tools that work together to protect both your surviving spouse and your children from prior relationships. A revocable living trust keeps your assets private while giving you complete control over how much your spouse receives, when your children inherit, and whether your homestead passes according to your actual intentions rather than Florida’s automatic devise rules. Beneficiary designations on life insurance and retirement accounts must align with your overall strategy, and a prenuptial or postnuptial agreement clarifies expectations upfront to prevent costly disputes later.

Your blended family’s unique structure demands a plan tailored to your specific wishes and Florida’s specific laws, because generic solutions fail when they ignore the competing interests that naturally exist in remarriages. Start by inventorying your current estate plan and identifying gaps-list your family structure, your assets, and your specific goals for how you want to provide for both your spouse and your children. Then contact an attorney who understands Florida blended family planning and can translate your wishes into legally binding documents that reflect your actual intentions.

We at Christine Sue Cook, LLC specialize in tailoring estate plans that honor your intentions while protecting everyone you care about. Contact us for a free consultation to discuss your situation without financial pressure, so you can explore your options and move forward with confidence that your family’s future is secure.