A power of attorney in Florida gives someone you trust the legal authority to act on your behalf-whether you’re temporarily unavailable or facing a health crisis. This document can protect your finances, property, and personal affairs when you need it most.

At Christine Sue Cook, LLC, we’ve helped countless families understand how to grant this authority safely and thoughtfully. The right power of attorney, created with care, gives you peace of mind and protects what matters most.

A power of attorney is a legal document that transfers specific decision-making authority from you, the principal, to someone you trust, called your agent or attorney-in-fact. Under Florida Statutes Chapter 709, this authority can cover finances, real estate, healthcare decisions, or any combination you specify. The document takes effect immediately upon signing unless you include language making it effective only upon a future event, like your incapacity. Florida law recognizes four main categories: general powers of attorney that grant broad financial authority, limited powers of attorney that restrict an agent to specific tasks like selling a house while you’re traveling, medical powers of attorney focused solely on healthcare decisions, and financial powers of attorney covering money matters. The critical distinction in Florida is durability. A durable power of attorney survives your incapacity, meaning your agent can continue acting if you become mentally unable to manage your affairs. A non-durable power of attorney automatically terminates if you lose capacity, which often forces families into expensive guardianship proceedings. Most Florida residents benefit from durable powers of attorney because they provide continuous protection without court intervention during health crises or cognitive decline.

Non-durable powers of attorney create dangerous gaps. If you become incapacitated without a durable document in place, your family cannot access your bank accounts, pay your bills, or make medical decisions without court approval. Guardianship proceedings in Florida cost between three thousand and five thousand dollars and require ongoing court supervision. A properly drafted durable power of attorney costs far less and avoids court delays that can last months. Your agent can immediately handle time-sensitive matters like paying mortgage obligations, managing investment accounts, or authorizing medical treatment. This matters especially if you face sudden illness or injury. For families managing Medicaid planning, a durable power of attorney with explicit authority to gift assets and restructure property becomes invaluable. The Medicaid look-back period means timing matters, and delays caused by guardianship proceedings can eliminate your eligibility for benefits entirely.

The scope of authority you grant directly affects how much protection your agent has and how much protection you have. Florida law allows you to grant banking authority, real estate authority, insurance authority, investment authority, or healthcare authority separately. Many people make the mistake of either granting too much authority or too little. Excessive authority without clear limits creates vulnerability to misuse, while insufficient authority leaves your agent unable to act when you need them most. The best approach specifies exactly which powers your agent holds. If you grant authority to manage investments, you can reference Florida Statutes Section 518.11 to clarify whether your agent can delegate investment decisions to a professional advisor. If you grant real estate authority, specify whether your agent can sell your primary residence, commercial property, or both. This specificity prevents disputes and gives third parties like banks and title companies confidence in your agent’s authority. Your agent must sign documents as agent for you, not in their personal capacity, to avoid personal liability. Florida notaries witness approximately 180 million documents annually, and power of attorney documents represent a significant portion because third parties routinely request notarized originals before accepting an agent’s authority.

Banks, title companies, and healthcare providers often request proof that your agent actually holds the powers you claim. They may ask for notarized copies, affidavits, or even counsel opinions before they accept your agent’s authority. These requests protect institutions from liability but can slow down urgent transactions. A well-drafted power of attorney with clear language about your agent’s specific powers reduces friction with third parties. Some institutions maintain their own POA forms and may ask your agent to complete them alongside your original document. Your agent should expect these requests and prepare copies of the power of attorney in advance. When your agent signs on your behalf, they must clearly indicate their status as agent to avoid personal liability for the transaction.

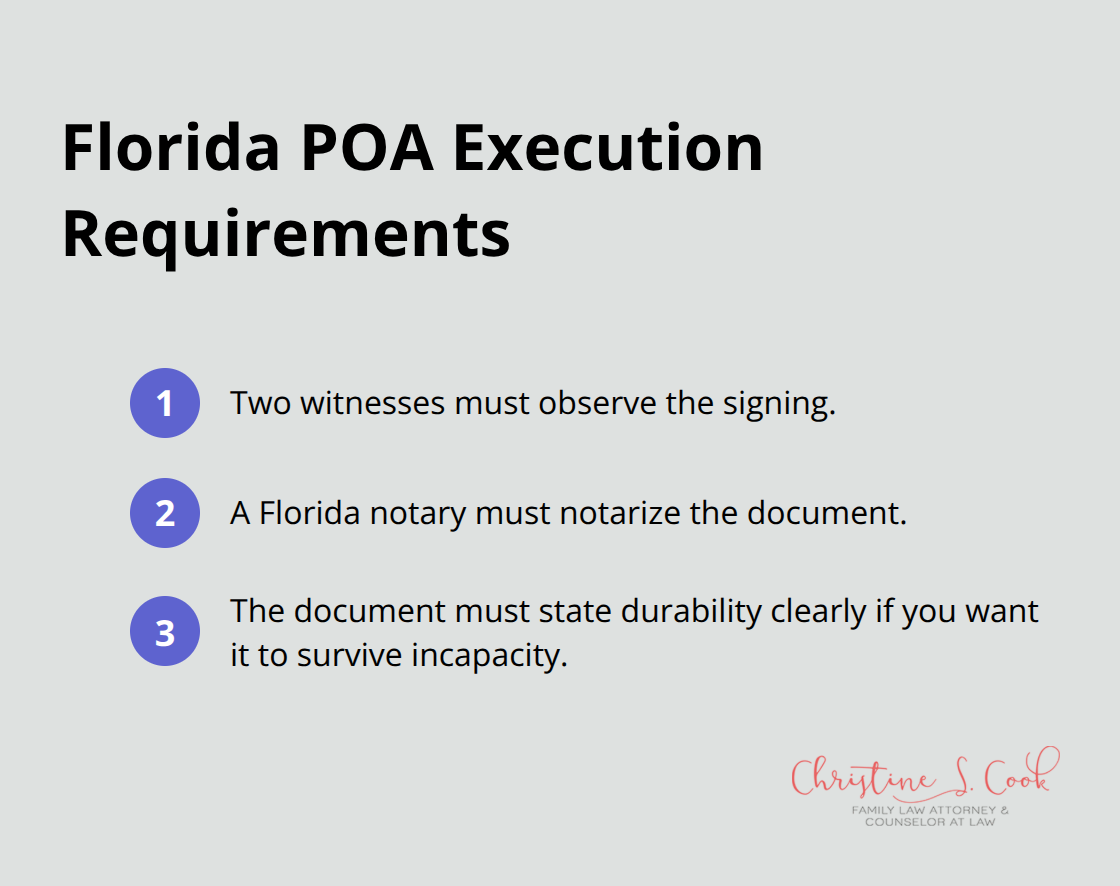

The authority you grant through a power of attorney only works if the document itself is valid and properly executed. Florida requires specific formalities-two witnesses, notarization, and clear language about durability-to make your power of attorney legally binding. Understanding these execution requirements helps you avoid costly mistakes that could render your document invalid when your family needs it most.

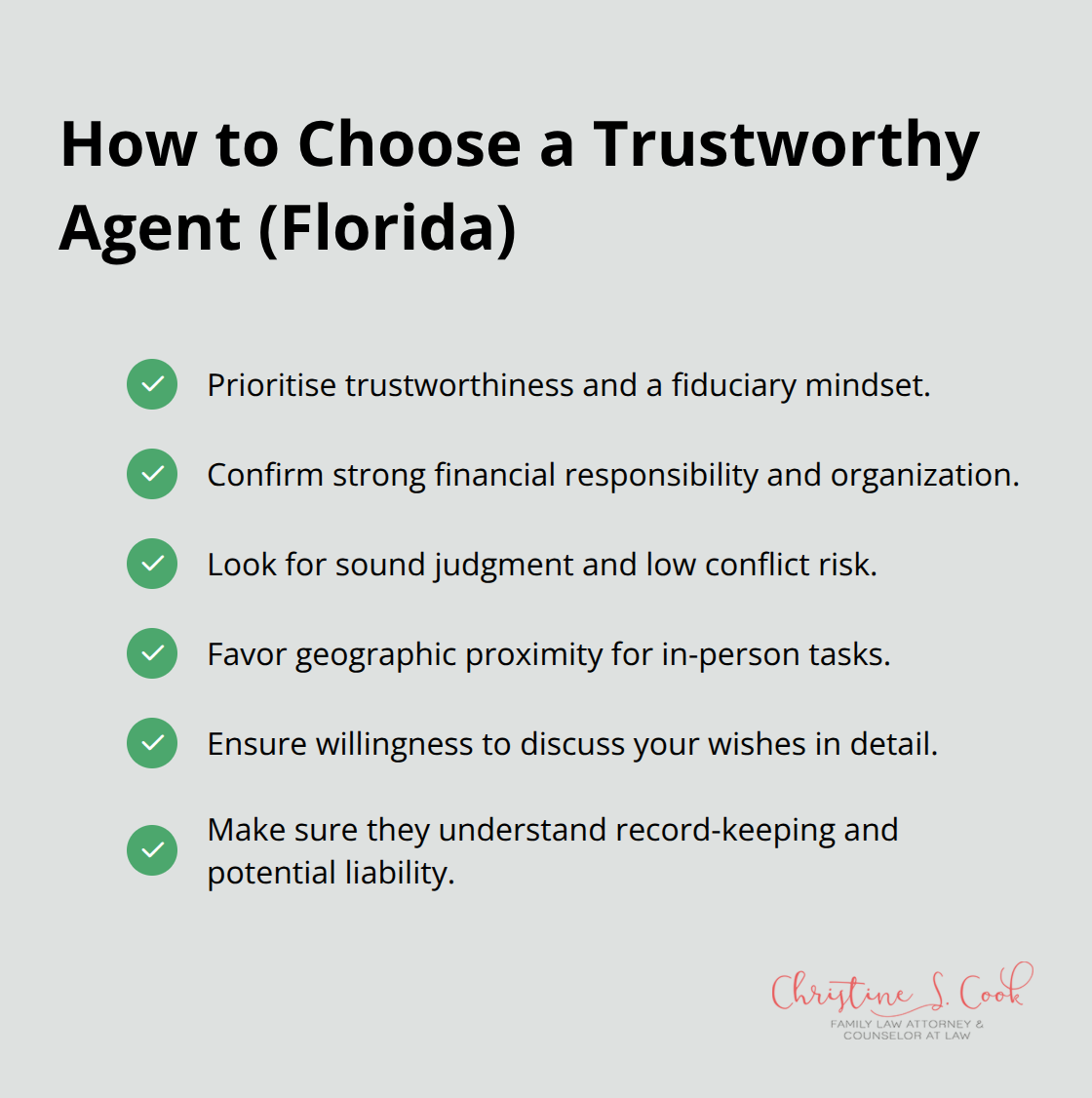

Selecting your agent ranks among the most important decisions in power of attorney planning because this person will handle your finances, property, and potentially your healthcare when you cannot. The wrong choice creates vulnerability; the right choice provides genuine security. Trustworthiness matters more than convenience or family obligation. Your agent must demonstrate financial responsibility, sound judgment, and willingness to prioritize your interests over their own.

Many families make the mistake of naming the oldest child or a spouse simply because they’re closest, without honestly assessing whether that person can handle the responsibility. An agent who struggles with their own finances, carries significant debt, or has a history of poor decision-making will likely mismanage yours. Florida law requires your agent to act as a fiduciary, meaning they must maintain detailed records, avoid conflicts of interest, and apply prudent standards when managing your assets. Agents can face civil or criminal liability for breach of fiduciary duty, so the person you select needs to understand this responsibility.

Consider whether your potential agent lives nearby and can handle in-person tasks like visiting banks or signing real estate documents. Geographic proximity matters because some institutions resist accepting remote agents, and time-sensitive matters require quick action. Your agent should also be willing to have a detailed conversation with you about your wishes, values, and specific instructions before you sign the document. If someone refuses this conversation or seems uncomfortable with the responsibility, that’s a clear signal to choose someone else.

Naming only one agent creates a dangerous single point of failure. If your primary agent becomes unavailable due to illness, death, or refusal to serve, your family faces immediate problems. You cannot act for yourself, and no one else has legal authority. Successor agents solve this problem by creating a clear chain of command.

Florida law allows you to name multiple successor agents in order of preference. When your primary agent cannot serve, the first successor automatically steps in without court involvement. This structure prevents expensive guardianship proceedings and keeps decisions moving forward during crises. The best approach names one primary agent with at least one backup and ideally a second backup. Each successor should be someone you trust completely, and you should have the same detailed conversation with each person about your wishes and expectations.

Some families consider naming co-agents who can act together, but this approach frequently backfires. Co-agents who disagree create deadlock during time-sensitive situations like Medicaid planning decisions that depend on precise timing. If both co-agents must sign every document and they cannot reach consensus, your bills go unpaid, medical decisions stall, and opportunities to protect assets disappear. Co-agents work only if they have an established history of working well together, are equally involved in your life, and genuinely want shared decision-making authority. Most families benefit far more from successor agents who provide clear, decisive action when urgency matters most.

Vague language in a power of attorney creates confusion that third parties exploit and agents misunderstand. You should specify exactly which powers your agent holds rather than granting blanket authority to do anything. If you want your agent to manage your bank accounts and investments, state so explicitly. If you want them to handle real estate but not make healthcare decisions, state that clearly. If you want them to gift assets for Medicaid planning purposes, authorize that specifically.

Florida law allows you to grant banking powers, investment powers, real estate powers, insurance powers, healthcare powers, or any combination. You can even set time limits on specific powers or restrict certain actions. For example, you might grant real estate authority but prohibit selling your primary residence without a second opinion. You might authorize gifts for Medicaid planning but cap the annual amount. This specificity prevents your agent from acting beyond your intentions and gives third parties confidence that your agent actually holds the authority they claim.

Generic online forms often fail because they either grant excessive undifferentiated authority or omit important powers your agent actually needs. A poorly drafted document either makes your agent powerless when you need them most or creates vulnerability to misuse. The cost of customized legal drafting is minimal compared to the financial damage from either scenario. Discussing your specific situation with an attorney ensures your power of attorney matches your actual circumstances and goals rather than forcing your life into a generic template. The right document empowers your agent to act decisively while protecting you from unauthorized actions-and that balance depends entirely on how clearly you define the authority you grant.

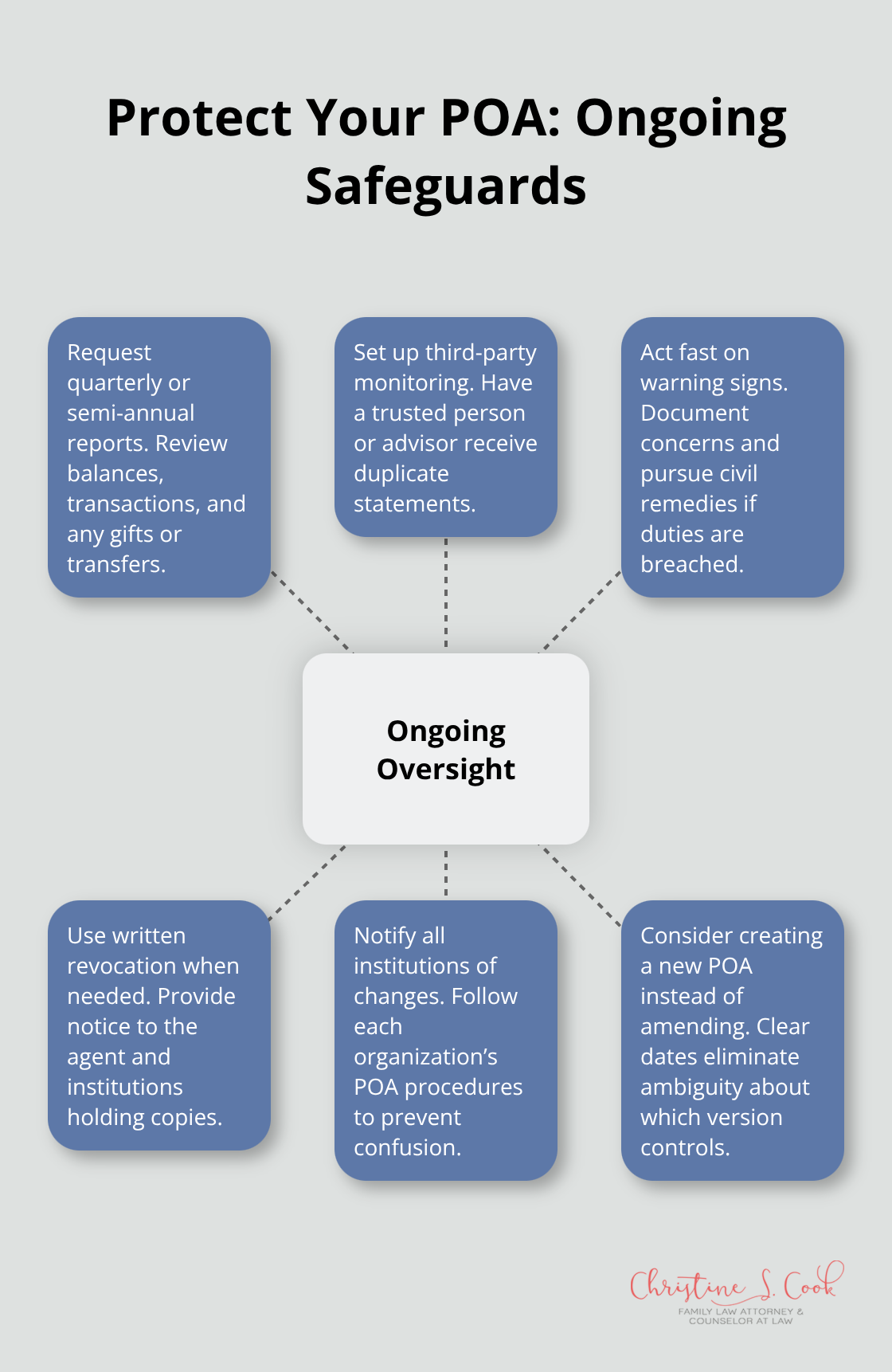

Your power of attorney document only protects you if you actively monitor what your agent actually does with the authority you granted. Many families treat the document as a one-time signing event and never revisit it, which creates dangerous blind spots. Your agent should provide you with regular account statements, receipts for major transactions, and documentation of any gifts or asset transfers made on your behalf. Florida law requires agents to act as fiduciary duties, which means they must maintain detailed records and preserve your estate plan when possible, but this duty only matters if you verify compliance.

Request quarterly or semi-annual reports from your agent that show bank balances, investment activity, and any significant transactions. If your agent resists providing documentation or becomes defensive about account access, that signals a serious problem requiring immediate attention. Some families establish a monitoring system where a trusted family member or professional advisor receives copies of statements to provide independent oversight. This approach prevents the isolation that enables financial exploitation and keeps your agent accountable for their actions.

If you discover unauthorized transactions or suspect your agent violated their fiduciary duties, Florida law allows you to pursue civil remedies depending on the severity. Document everything when concerns arise because courts require clear evidence of misuse before intervening. The sooner you act, the better your chances of recovering funds or stopping further unauthorized activity. Waiting months or years to address problems makes recovery far more difficult and allows damage to compound.

You can revoke a power of attorney at any time while you remain competent by executing a written revocation document and providing notice to your agent and any third parties who hold copies. Simply destroying the original document or telling your agent verbally does not legally revoke the authority. Florida law does not automatically revoke an existing power of attorney when you create a new one, so institutions may continue accepting your old agent’s authority unless you explicitly notify them.

Contact your banks, investment firms, healthcare providers, and insurance companies with written notice that the previous power of attorney is revoked and provide copies of the new document. Many institutions maintain their own procedures for POA changes, so ask each one about their specific requirements. Keeping a master list of every institution and person holding a copy of your power of attorney makes this notification process manageable. This documentation protects you from confusion and prevents your old agent from continuing to act after revocation.

If you modify your power of attorney rather than fully revoking it, consider whether creating an entirely new document serves your interests better than amending the existing one. A completely new document with clear execution dates eliminates ambiguity about which version institutions should recognize. Store the original executed power of attorney in a secure location, provide copies to your agent and key institutions, and maintain a backup copy in a safe deposit box or with your attorney.

A power of attorney in Florida represents one of the most practical decisions you can make for your family’s security. The document itself costs far less than guardianship proceedings, yet it provides infinitely more control over your affairs when health crises or incapacity strike. You’ve learned that durability matters, that choosing the right agent determines everything, and that monitoring your agent’s actions protects both your finances and their integrity.

Creating your power of attorney requires honest conversations with potential agents about your wishes, values, and expectations. You must name successor agents to prevent authority gaps and use clear language about which powers your agent actually holds rather than forcing your situation into a generic template. Schedule a consultation with an attorney who understands Florida estate planning and can tailor your power of attorney to your specific situation, discuss whether you need separate medical and financial powers of attorney, and provide copies to your agent, financial institutions, and healthcare providers.

At Christine Sue Cook, LLC, we guide families through this process with the care and attention you deserve. Our team understands that power of attorney planning protects what matters most and ensures your wishes guide decisions when you cannot. The peace of mind that comes from proper planning is worth far more than the modest investment required to create it.