Being named an executor is an honor, but it comes with real responsibilities. Florida probate administration requirements are specific and time-sensitive, and missing a deadline or misunderstanding your duties can create serious problems for you and the beneficiaries.

We at Christine Sue Cook, LLC help executors navigate this process every day. This guide walks you through what you need to know to handle your role properly.

Your responsibilities as an executor extend far beyond distributing money to beneficiaries. Florida law requires you to identify all probate assets, secure them, notify creditors and beneficiaries, file court documents within strict deadlines, pay valid debts and taxes, and eventually transfer what remains to the beneficiaries. The Florida Probate Code (Chapters 731–735) defines these duties clearly, and the court expects you to follow them exactly.

Most executors underestimate the complexity of asset classification. You must distinguish between probate assets (those owned solely by the decedent without automatic transfer) and non-probate assets like joint accounts, payable-on-death designations, and life insurance with named beneficiaries. Missing this distinction causes delays and legal exposure. Non-probate assets pass directly to their designated recipients outside the probate process, so you don’t control them-but you still need to identify them for the estate record.

You serve as a fiduciary, meaning you have a legal obligation to act in the beneficiaries’ best interests, not your own. This prohibits self-dealing-you cannot buy estate property at a bargain price or liquidate assets for your personal benefit. The court takes fiduciary violations seriously and can remove you from your role if you breach this duty.

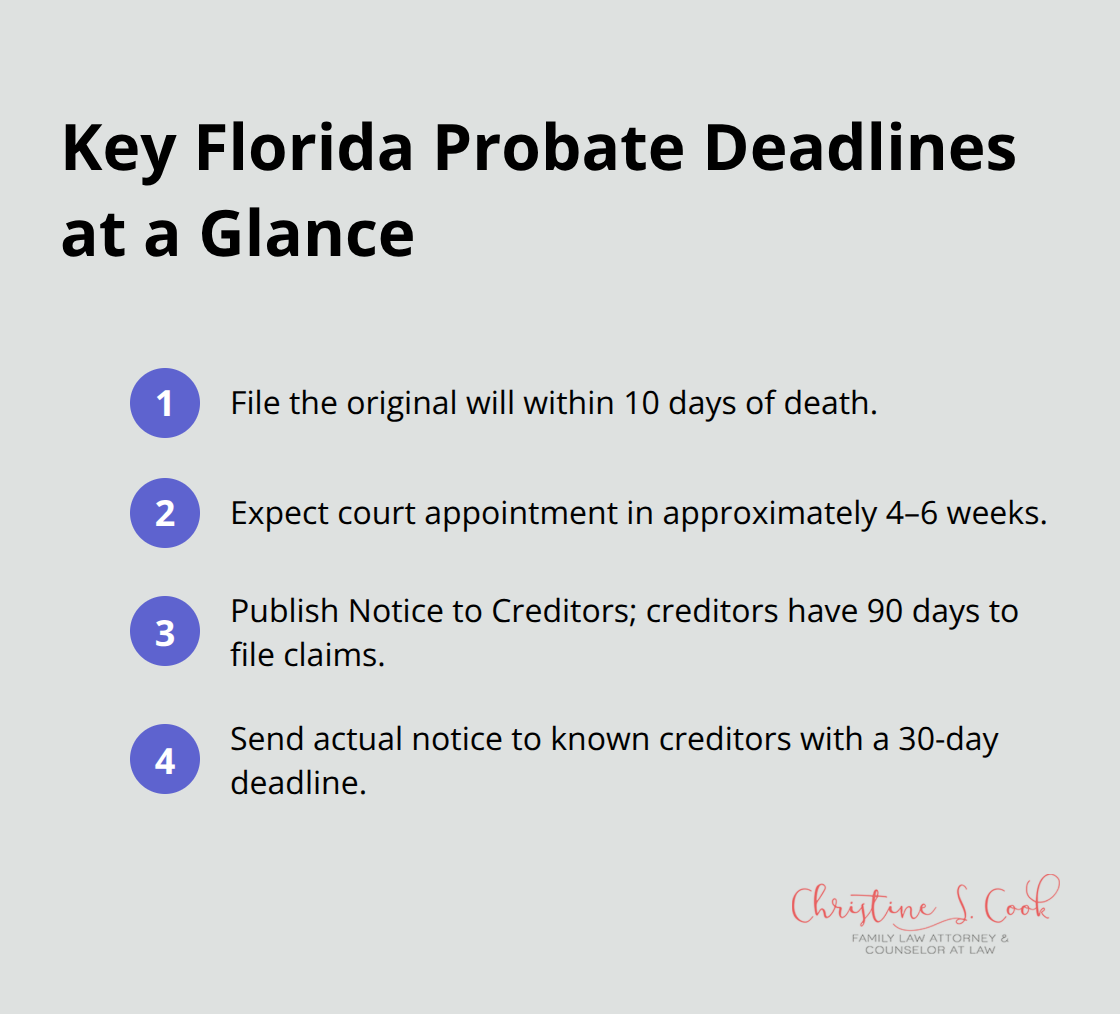

Florida law imposes strict timelines you cannot ignore. You have ten days from death to file the original will with the Clerk of the Circuit Court, and you must obtain Letters of Administration from the court before you can legally act as executor. The court typically appoints you within four to six weeks, but this varies by county. Once appointed, formal probate requires you to publish a Notice to Creditors in a local newspaper, which gives creditors ninety days to file claims. Known creditors must receive actual notice with a thirty-day deadline to submit claims.

The entire probate process in Florida typically takes five to six months for straightforward estates, though complex cases stretch twelve months or longer. If your estate qualifies for summary administration-meaning non-exempt assets total $150,000 or less and the decedent died more than two years ago or debts are paid or undisputed-the process moves faster, usually within two to three months. The three-month creditor claim period is mandatory regardless of estate complexity.

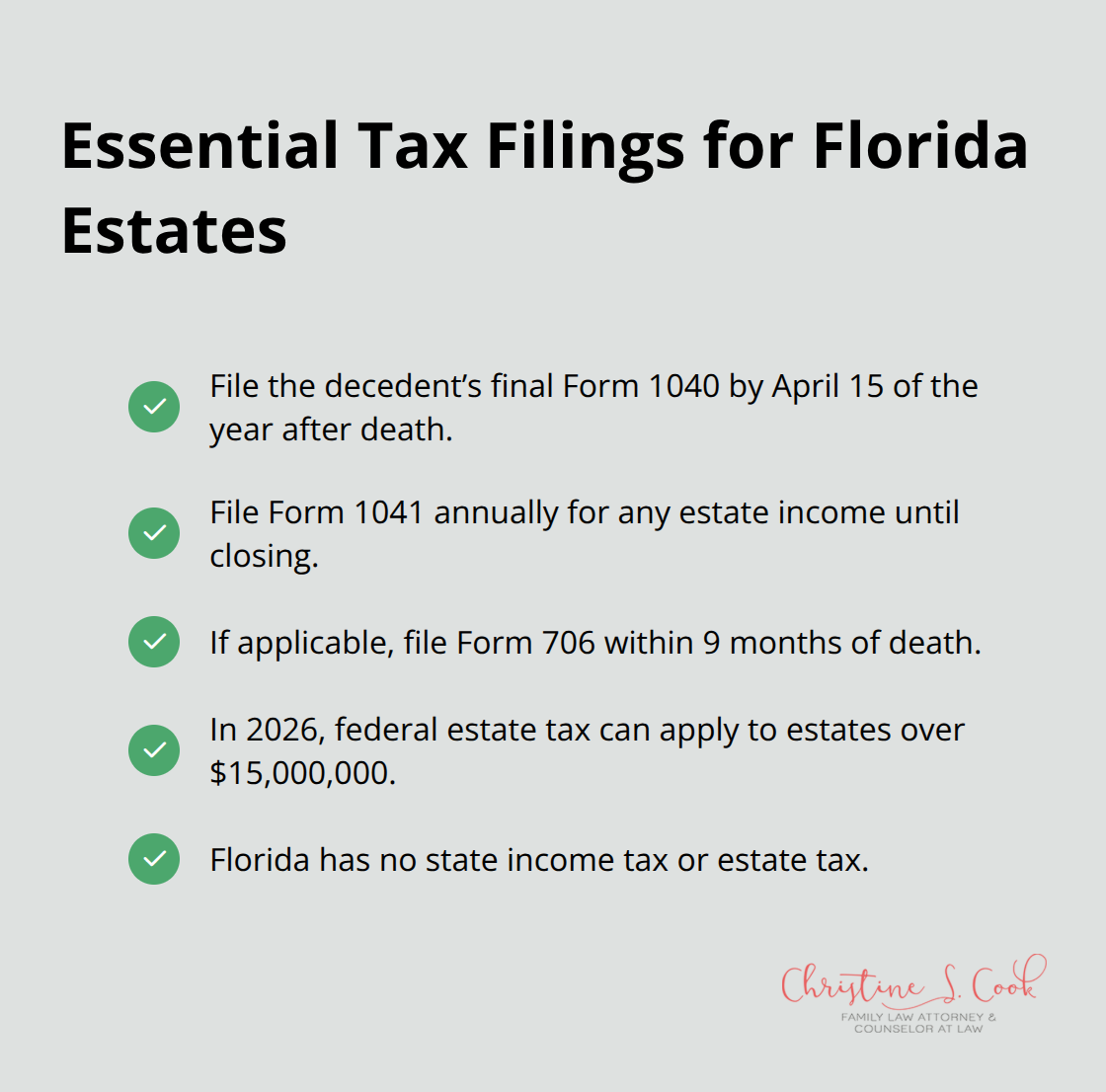

You must file the decedent’s final federal tax return, and if the estate owes federal estate taxes, Form 706 is due nine months after death. Failing to meet these deadlines can result in court sanctions, personal liability, and beneficiary lawsuits against you. A probate attorney can help you establish a filing calendar and avoid costly mistakes. Understanding these specific requirements positions you to handle the next phase: the actual steps required to move the estate through probate.

Start probate by filing a petition with the Clerk of the Circuit Court in the county where the decedent lived. You’ll submit the original will, a death certificate, and a petition for administration. The filing fee varies by county but typically ranges from $300 to $500. Once filed, the court assigns a file number and schedules a hearing, usually within four to six weeks. At that hearing, the judge reviews your qualifications and appoints you officially as personal representative, issuing Letters of Administration that prove your legal authority to act.

This document is essential-banks, creditors, and asset custodians will demand certified copies before releasing information or transferring ownership. Many executors make the mistake of trying to access accounts or move assets before receiving Letters; financial institutions will refuse, wasting weeks of effort. Obtain those letters first, then proceed.

You’ll need an IRS Employer Identification Number for the estate, which you obtain online for free at IRS.gov. This EIN allows you to open an estate bank account separate from your personal finances-a critical step for tracking all money flowing in and out. Once your account is open, publish the Notice to Creditors in a local newspaper; the clerk can direct you to approved publications.

This ninety-day notice period is mandatory and cannot be shortened, even for simple estates. During this window, you must also send actual notice to any known creditors, giving them thirty days to file claims. Many executors overlook known creditors and later face claims after distributions, creating personal liability for you.

Inventorying assets requires more than listing what you find. You must obtain professional appraisals for real estate, vehicles, jewelry, and other valuable items, typically costing $300 to $1,000 per appraisal depending on complexity. For bank accounts and investment portfolios, gather statements as of the date of death-financial institutions provide these for free. Real property values come from the county property appraiser’s office or a licensed appraiser.

Next, identify all debts: mortgages, credit cards, medical bills, funeral expenses, and any loans the decedent owed. Request a credit report for the decedent from all three bureaus to catch creditors you might miss. Funeral costs typically run $7,000 to $12,000 and must be paid first as a priority claim.

Once you’ve identified debts and assets, you cannot distribute anything to beneficiaries until all valid claims are paid and taxes are filed. This is where executors face the most pressure-beneficiaries want their money, but premature distributions expose you to liability if creditors file claims afterward.

File the decedent’s final Form 1040 federal tax return by April 15 of the year following death, and if the estate generates income during administration, file Form 1041 annually until closing. If federal estate taxes apply (estates exceeding $15,000,000 in 2026 face this), Form 706 is due nine months after death. Florida has no state income tax or estate tax, simplifying your burden compared to other states.

Only after all debts, taxes, and administrative expenses are paid can you distribute remaining assets to beneficiaries according to the will or Florida intestacy law. Document every transaction meticulously-maintain bank statements, receipts, appraisals, and correspondence with creditors and beneficiaries. This paper trail protects you if disputes arise later. As you navigate Florida probate rules and procedures, you’ll encounter situations that demand specialized knowledge-particularly when family members disagree about decisions or when assets prove more complicated than expected.

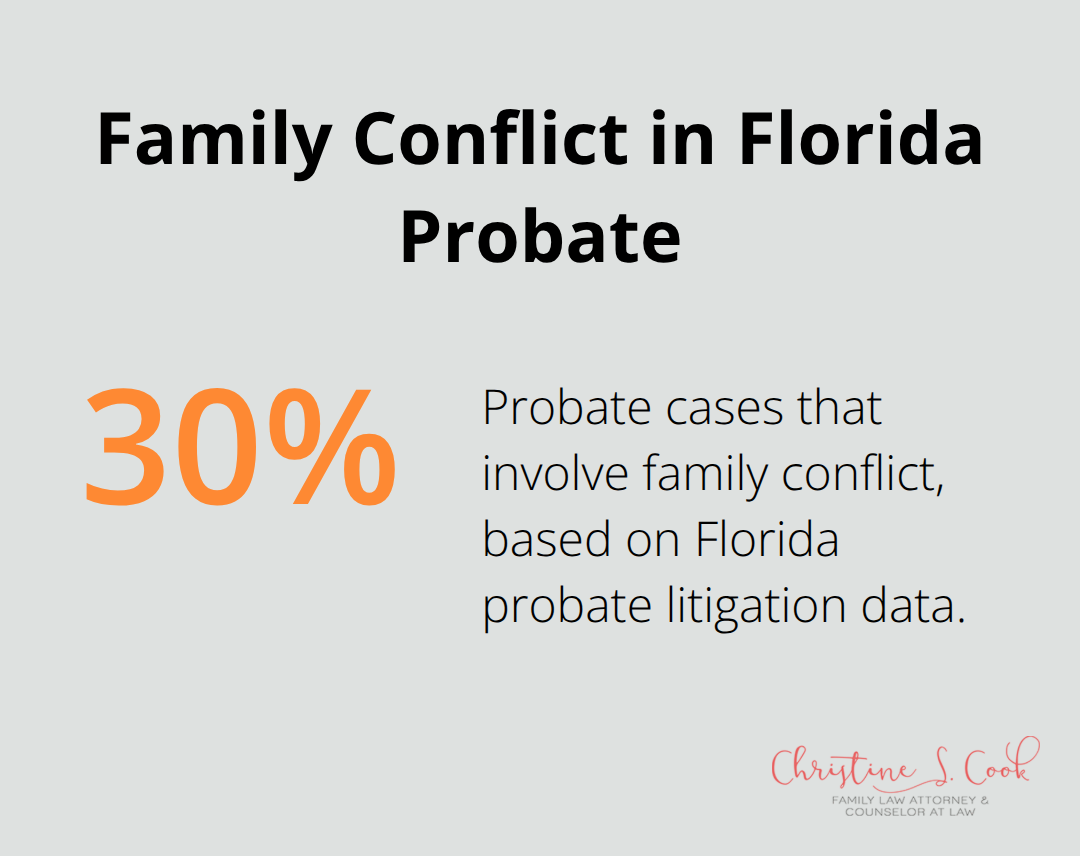

Family conflict emerges in roughly 30 percent of probate cases according to litigation data from probate practices across Florida, and it often stems from unclear communication rather than genuine disagreement about the will’s terms. When beneficiaries feel left out of decisions or don’t understand why distributions are delayed, resentment builds quickly.

Your job includes keeping beneficiaries informed about probate progress, asset valuations, and timelines-not just meeting the legal minimum notice requirements. Many executors treat beneficiary updates as optional, then face accusations of hiding information or mismanaging funds. Send written updates every two to three months detailing what you’ve accomplished, what remains, and realistic completion dates. If a beneficiary challenges your decisions or questions your authority, do not respond emotionally or attempt to defend yourself alone. Consult a probate attorney immediately; an attorney’s letter often resolves disputes faster than your explanations ever will, and it creates a formal record protecting you from later liability claims.

Tax obligations trip up executors more than any other single issue because many don’t realize the estate itself becomes a separate tax entity after death. You must obtain an IRS EIN, file Form 1041 for any estate income earned during administration, and handle the decedent’s final Form 1040 return. If the estate owes federal estate taxes, Form 706 becomes due nine months after death, and extensions cost time you may not have. Funeral expenses typically consume $7,000 to $12,000 of estate assets as a priority claim, and you cannot reduce this amount by negotiating with funeral homes after services are complete.

Real estate mortgages, credit card debts, and medical bills must be identified and paid in a specific order under Florida law, with secured debts like mortgages paid before unsecured claims like credit cards. The largest executor mistake here is distributing assets before confirming all tax liabilities are resolved; one missed creditor claim after distribution creates personal liability for you to cover that claim from your own funds.

Complex assets like closely held business interests, rental properties with tenants, or investment portfolios require professional valuation and often demand that you hire an accountant or business appraiser at costs ranging from $1,500 to $5,000 depending on complexity. You cannot navigate these valuations alone without exposing yourself to disputes over asset worth and potential tax penalties. A probate attorney can connect you with qualified professionals who understand Florida probate requirements and can provide defensible valuations that satisfy the court and beneficiaries alike.

Serving as a Florida executor demands attention to detail, strict adherence to deadlines, and honest communication with beneficiaries and creditors. The probate administration Florida requirements you’ve learned here-from filing within ten days to managing the ninety-day creditor notice period to paying taxes before distributions-protect everyone involved, including you. Missing even one deadline or overlooking a single creditor exposes you to personal liability and court sanctions that cost far more than hiring professional help upfront.

The most successful executors recognize that probate administration is not a do-it-yourself project. A probate attorney guides you through court filings, tax obligations, and disputes, while an accountant handles estate tax returns and ensures compliance with IRS deadlines. These professionals cost money, but their fees come from estate assets, not your pocket, and they protect you from mistakes that could cost thousands in personal liability.

If you’re facing executor duties in Florida, contact Christine S. Cook, LLC for guidance. Christine and her team offer free consultations to discuss your specific situation without financial pressure, and they understand the emotional weight of settling an estate while managing family dynamics and legal requirements.