Divorce brings financial uncertainty that requires immediate attention and careful planning. Creating a comprehensive divorce financial planning checklist helps you navigate this complex process systematically.

We at Christine Sue Cook, LLC understand that organizing your finances during divorce feels overwhelming. The right preparation protects your financial future and reduces stress during an already difficult time.

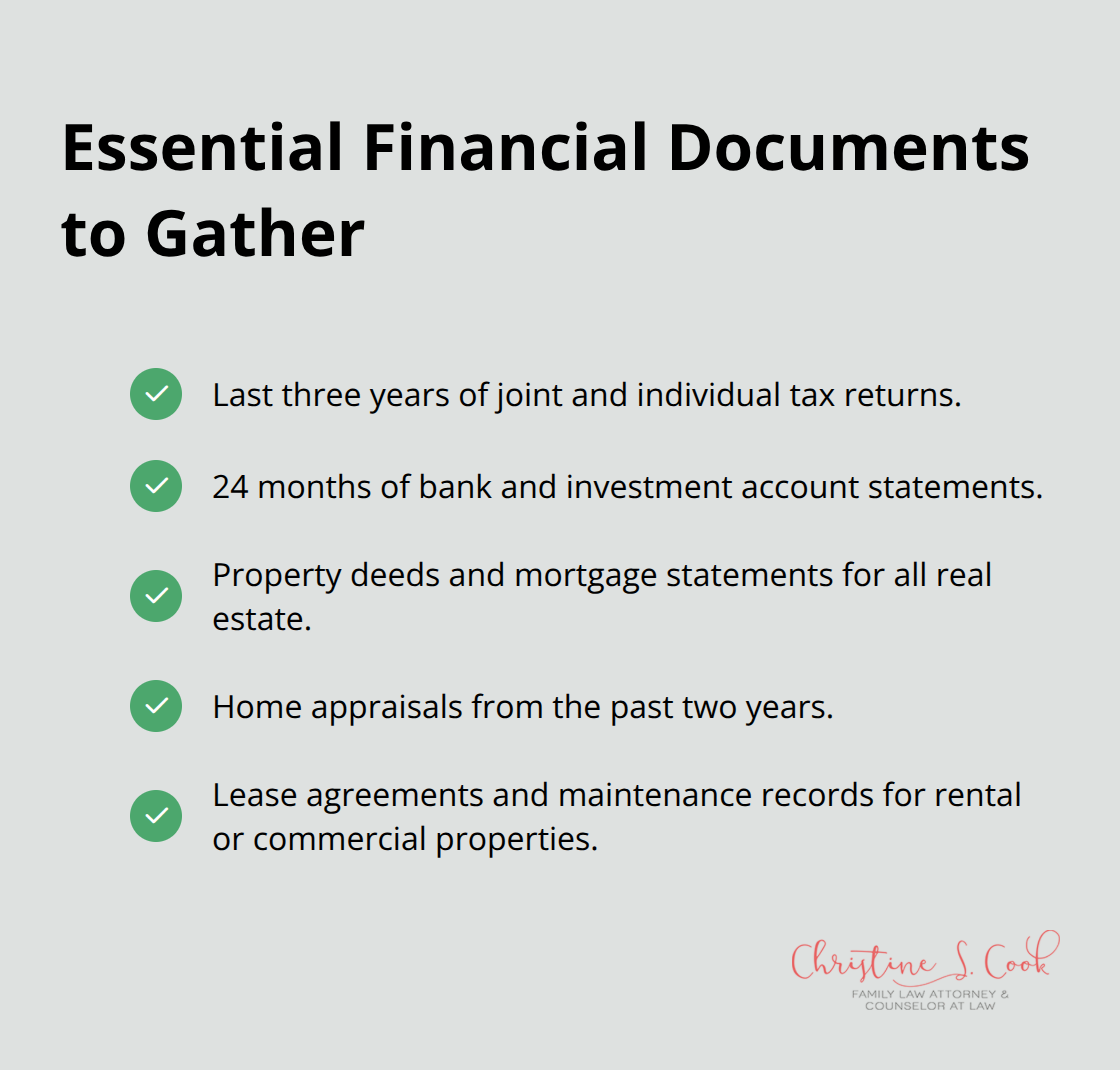

Start with the last three years of joint and individual tax returns from both spouses. These documents expose hidden income sources, unreported cash payments, and business deductions that spouses often forget to mention. Tax returns show actual income versus claimed income, which matters significantly during asset division.

The IRS requires accurate reports, which makes these documents your most reliable source for income verification. Request copies directly from the IRS if your spouse controls access to tax documents. This approach prevents tampering or selective disclosure that could harm your case.

Collect 24 months of statements from all accounts (checking, savings, money market, and investment accounts) held individually or jointly. Financial institutions typically charge fees for statements older than 12 months, but this expense pays for itself during negotiations.

Look for unusual transfers, large withdrawals, or new accounts opened during marriage troubles. Investment statements reveal retirement contributions, employer matches, and account values that determine your future financial security. Many spouses attempt to hide assets by transferring funds to family members or business accounts, which makes complete records essential for fair distribution.

Property deeds show ownership structure and purchase dates, which determines whether real estate qualifies as separate or marital property. Mortgage statements reveal current balances, payment histories, and equity calculations needed for property division.

Home appraisals from the last two years provide baseline values, though current market conditions may require updated assessments. Commercial property, rental units, and vacation homes require separate documentation including lease agreements and maintenance records that affect net value calculations.

With these essential documents in hand, you can move forward to assess your complete financial position and understand exactly what assets and debts you face in your divorce.

Calculate your precise monthly income from all sources including salary, bonuses, rental income, business profits, and investment returns. According to the National Center for Health Statistics, divorce affects 672,502 individuals annually with a rate of 2.4 per 1,000 population. Add up every expense category: housing, utilities, insurance, food, transportation, childcare, and discretionary spending. Track expenses for 90 days with bank statements rather than estimates, which typically miss 30-40% of actual expenditures according to financial planning research.

Create a comprehensive asset inventory with current market values, not purchase prices or tax assessments. Retirement accounts like 401(k)s and IRAs require professional valuation because early withdrawal penalties affect their true worth. The Survey of Consumer Finances shows that married couples hold an average of $129,000 in retirement assets, which makes accurate valuation essential for fair division. Document all debts including credit cards, mortgages, car loans, student loans, and business obligations.

Credit card debt averages $6,194 per household according to Federal Reserve data, but divorce often reveals hidden accounts that increase total obligations significantly.

Separate property includes assets owned before marriage, inheritances, and gifts received individually during marriage. However, commingled separate assets with marital funds convert them to marital property in most states. Equitable distribution states divide property equitably rather than equally, while community property states tend to divide assets equally. Property appreciation during marriage typically counts as marital assets even when the original property was separate. Professional appraisals become necessary when property values exceed $50,000 or when ownership disputes arise over business interests or real estate investments.

With your complete financial position mapped out, you can now focus on the next step: creating a realistic post-divorce budget that reflects your new financial reality.

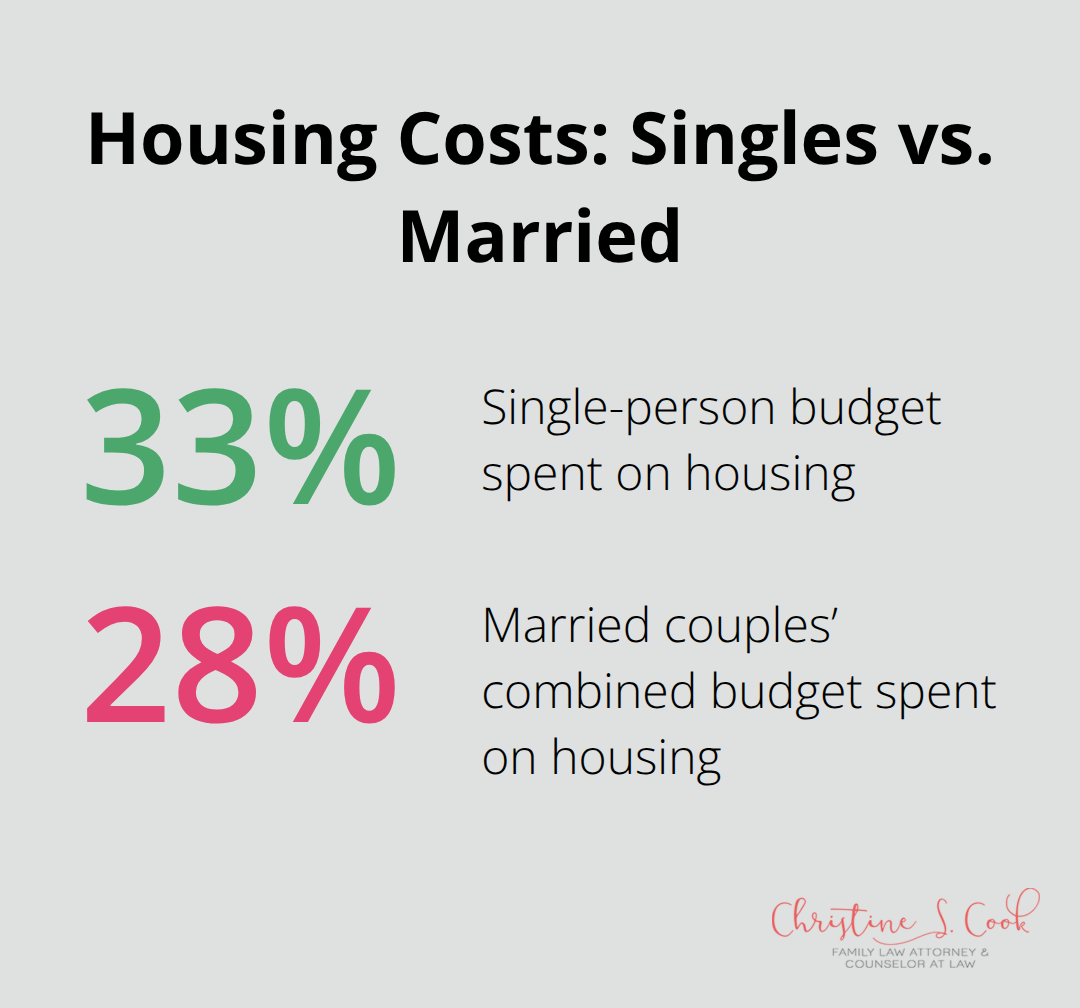

Your housing costs will increase dramatically as a single person compared to shared expenses during marriage. The Bureau of Labor Statistics reports that single-person households face significant expenses, while married couples spend $63,036 combined. This means you face substantial expenses on potentially half the income.

Housing typically consumes 33% of single-person budgets versus 28% for married couples, which translates to significant annual costs for singles. You must factor in separate utilities, internet, insurance policies, and maintenance costs that you previously shared. Childcare expenses become entirely your responsibility during custody periods (with the Economic Policy Institute showing costs ranging from $4,810 to $22,631 annually per child depending on location).

Child support calculations follow state guidelines, with states using three main models: Income Shares, Percentage of Income, and Melson Formula to determine support amounts. Spousal support varies significantly by state and marriage duration, but typically ranges from 30% to 50% of the income difference between spouses for marriages lasting 10+ years.

The Tax Cuts and Jobs Act eliminated federal tax deductions for alimony payments after 2018, which means you pay support with after-tax dollars. You must create separate budget categories for these fixed obligations because courts enforce payment regardless of your other financial pressures.

Emergency funds require 6-8 months of expenses for divorced individuals versus 3-6 months for married couples, according to financial planning standards. You lack a second income safety net during job loss or medical emergencies (which makes larger reserves essential for financial stability). Single-income households face greater vulnerability to unexpected expenses and income disruptions that previously affected only half your household budget.

Creating a post-divorce budget becomes essential for managing these increased financial responsibilities and ensuring long-term stability.

A comprehensive divorce financial planning checklist requires systematic documentation, accurate financial assessment, and realistic budget projections for your post-divorce life. The process starts with three years of tax returns, bank statements, and property documents that reveal your complete financial picture. You calculate total household income and expenses while you distinguish marital assets from separate property to understand what faces division.

Professional guidance becomes essential when you navigate complex asset valuations, support calculations, and tax implications that affect your long-term financial security. Modern divorce cases present financial complexities that most individuals lack expertise to handle (particularly when dealing with retirement accounts, business interests, or substantial real estate holdings). Qualified professionals understand both the legal and financial aspects of divorce proceedings.

Your next step involves implementation of this divorce financial planning checklist while you work with qualified professionals who specialize in divorce matters. We at Christine Sue Cook, LLC provide compassionate legal support and representation when necessary. Action now with proper planning and professional guidance protects your financial future and reduces the stress that accompanies this challenging life transition.