Alimony negotiations often feel one-sided if you walk in unprepared. The difference between a fair settlement and an unfavorable one comes down to how well you understand the numbers and the law.

At Christine Sue Cook, LLC, we’ve seen firsthand how alimony negotiation tips make the real difference in outcomes. This guide walks you through the financial strategies and negotiation approaches that actually work.

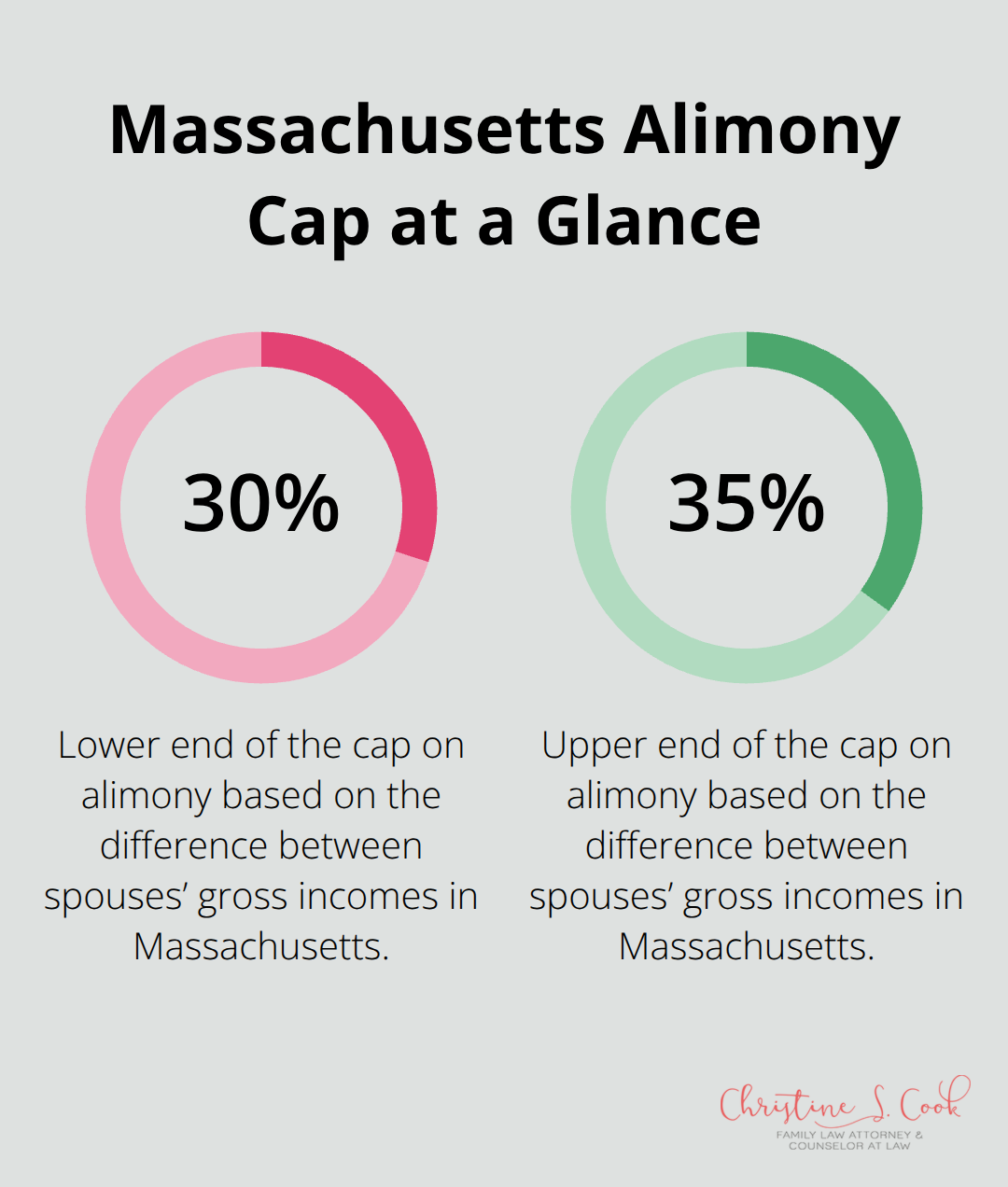

Courts don’t pull alimony numbers from thin air, and understanding how judges actually calculate support amounts gives you a concrete advantage in negotiations. In Massachusetts, courts follow the Child Support Guidelines formula, which caps alimony at roughly 30 to 35 percent of the difference between spouses’ gross incomes. This means if one spouse earns $100,000 and the other earns $40,000, the maximum support would fall around $21,000 to $24,500 annually.

However, this formula only applies if the combined parental income stays below the threshold; above that, judges exercise discretion. Courts also exclude certain income sources from calculations, such as capital gains and dividends from assets already divided during the settlement. This distinction matters enormously because it narrows what income actually counts, potentially reducing the support obligation significantly.

Judges examine salary, bonuses, self-employment income, rental income, and benefits to establish gross income. What they typically exclude are capital gains from the sale of assets already awarded in the divorce and investment dividends from divided property. If your ex-spouse receives a lump-sum distribution from a pension or retirement account as part of asset division, future earnings from that account usually don’t factor into alimony calculations. This is why forensic accountants prove invaluable-they identify which income streams count and which don’t, often revealing that apparent high earnings actually yield lower support obligations. Self-employed individuals face extra scrutiny because judges examine business expenses, depreciation, and whether income fluctuates seasonally. Tax returns from the past three to five years provide the clearest picture, and discrepancies between reported income and actual deposits signal problems that invite court scrutiny. State laws vary dramatically on these points; some jurisdictions count imputed income if someone voluntarily reduces earnings, while others don’t. Your jurisdiction’s specific rules determine whether a spouse leaving a high-paying job to pursue lower-income work affects support amounts.

Courts weigh both economic and non-economic contributions to marriage when setting alimony. If one spouse stayed home raising children while the other built a career, judges recognize that sacrifice reduced earning potential and often award higher support to compensate. Massachusetts law specifically allows courts to consider lost economic opportunity caused by the marriage. This means documenting your contributions matters as much as showing your financial need. If you postponed education, left a career, or took lower-paying positions to support family responsibilities, gather evidence-emails, calendars, testimony from witnesses-showing those choices. Courts also examine the standard of living during marriage and aim to help the lower-earning spouse maintain a reasonably comparable lifestyle. This creates leverage in negotiations because judges use this standard as a baseline. If the marital lifestyle required $8,000 monthly for housing, healthcare, and essentials, that figure anchors alimony discussions. Different states define what constitutes the marital standard of living, so research your jurisdiction’s case law. Some courts include discretionary spending like vacations and entertainment; others focus only on essentials. Understanding your state’s approach lets you frame negotiations around documented expenses that courts actually recognize.

Your understanding of how courts calculate alimony and what state laws require positions you to move forward with confidence. The next step involves building the financial case that supports your position-one backed by thorough documentation, clear evidence of your standard of living, and realistic projections about future earning potential. This foundation transforms abstract legal principles into concrete numbers that strengthen your hand at the negotiation table.

Accurate financial documentation transforms vague claims into irrefutable evidence that strengthens your negotiating position dramatically. Collect three to five years of tax returns, recent pay stubs covering the last six months, bank statements from all accounts, investment statements, retirement account statements, and mortgage or rental agreements. This paperwork establishes your actual income and expenses with precision that judges and opposing counsel cannot dispute.

Organize expenses by category-housing, utilities, groceries, healthcare, insurance, childcare, transportation, and debt payments. Create a monthly expense spreadsheet that reflects your current lifestyle, not an inflated wish list.

Courts scrutinize inflated expense claims and reduce credibility when numbers appear exaggerated. If your monthly expenses total $6,500 but you claim $9,000, judges assume dishonesty across your entire financial presentation.

The credibility you establish through accurate documentation extends to income claims and earning potential arguments. If opposing counsel cannot find inconsistencies in your expense documentation, they face difficulty attacking your income assertions or alimony requests. Consistency matters more than aggressive positioning-judges trust parties who present realistic numbers backed by evidence.

Document the standard of living during your marriage with receipts, credit card statements, and historical bank records. Pull statements from the year before separation to show what your household actually spent on housing, dining, entertainment, and discretionary items. This historical spending pattern becomes your baseline for arguing what alimony should maintain. If you and your spouse spent $8,000 monthly during the marriage but now claim you need $5,500, that discrepancy weakens your position. Conversely, if you spent $8,000 and request $7,800 in support, the consistency strengthens your credibility.

Forensic accountants or certified divorce financial analysts review your documentation, identify hidden income sources your spouse may not have disclosed, and validate your expense calculations. Their written reports carry significant weight in negotiations because they come from neutral professionals without personal stake in the outcome. If your spouse owns a business, a forensic accountant examines business expenses, depreciation schedules, and cash withdrawals to reveal whether reported income understates actual earning capacity. This investigation often uncovers additional income, substantially increasing support obligations.

Prepare for questions about future earning potential by gathering evidence of your work history, education, certifications, and any career interruptions caused by marriage responsibilities. If you left a nursing career to raise children, document your original salary, current certification status, and the timeline required to return to full-time practice. Connect these specifics to concrete dollar figures-if returning to nursing requires six months of refresher training and costs $3,000, that becomes part of your alimony justification for temporary support during transition.

This financial foundation positions you to move into negotiation strategy with confidence. The numbers you’ve assembled now anchor your discussions, and the next section shows you how to leverage this evidence when choosing between collaborative approaches and more aggressive tactics.

Knowing your baseline and walk-away point transforms alimony negotiations from emotional exchanges into strategic discussions anchored in reality. Calculate the absolute minimum you need monthly to cover housing, utilities, healthcare, childcare, and debt service. This floor number becomes your walk-away point-below it, you reject offers and prepare for court. Simultaneously, calculate the maximum alimony amount Massachusetts law permits based on the income difference formula, then reduce it by 10 to 15 percent to create a realistic ceiling. Most settlements land between these two figures.

If your documented needs total $4,200 monthly and the legal maximum supports $5,800, your negotiation range spans $4,200 to $5,200. Opposing counsel will anchor discussions at their preferred extreme, so starting negotiations at your ceiling while accepting your floor as the genuine minimum prevents you from drifting below what you actually need.

Courts award alimony as general term, rehabilitative alimony, or reimbursement support, and each type carries different implications for duration and modification. Rehabilitative alimony specifically targets self-sufficiency through education or training, making it ideal if you need two years to complete a nursing degree or certification program. Propose rehabilitative support with explicit milestones-completion of coursework by month eighteen, employment by month twenty-four-because judges favor time-limited arrangements that promote independence over indefinite obligations.

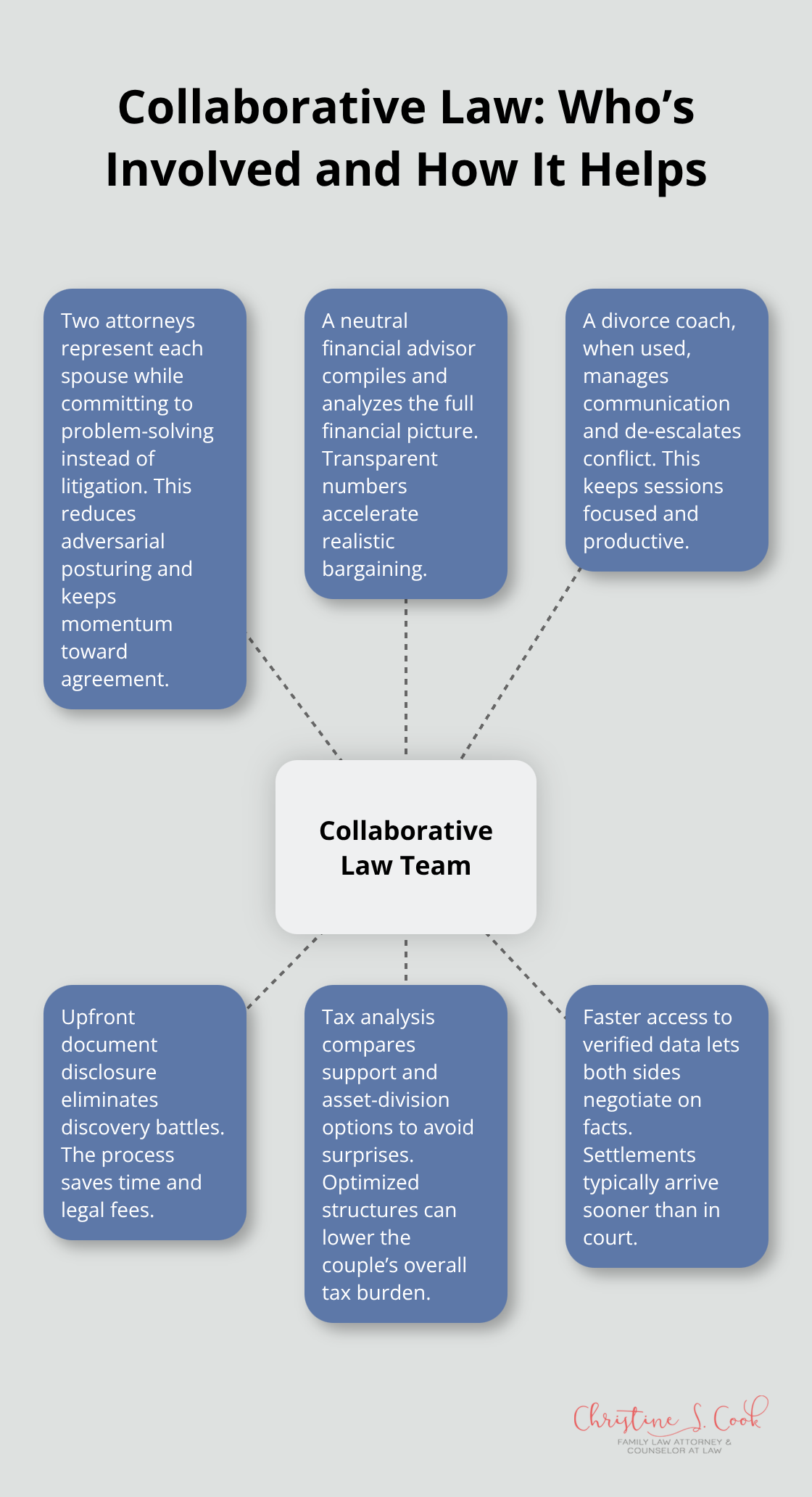

Collaborative law accelerates settlements and preserves relationships when children remain in the picture, making it substantially preferable to litigation in most situations. The collaborative process requires both spouses’ attorneys, a neutral financial advisor, and sometimes a divorce coach to keep discussions constructive. Each party discloses financial documents upfront, eliminating discovery disputes that consume months and legal fees. When both sides know the actual numbers immediately, realistic negotiation begins faster.

Financial advisors analyze tax implications of different asset divisions and alimony structures, catching problems that separate negotiations miss. If one spouse retains a retirement account while the other receives alimony, the tax treatment differs significantly-alimony payments remain taxable income for the recipient, while retirement distributions carry their own tax consequences.

A financial advisor identifies these overlaps and proposes structures that minimize combined tax liability, creating genuine win-win solutions.

Professional valuations for businesses, real estate, or complex assets prevent disputes during negotiations because both parties commission independent appraisers who provide written reports. If your spouse owns a business valued at $400,000 according to their estimate but an independent valuation shows $550,000, that $150,000 difference directly impacts alimony calculations. The higher business value increases the payer’s earning capacity and justifies higher support.

Insist on independent appraisals for any asset exceeding $50,000 in value-the cost of appraisal (typically $1,500 to $3,500) pales against the settlement impact. Settlement negotiation structured through collaborative processes ensures you access approaches that protect your interests while reducing conflict and legal expenses.

Preparation and documentation determine outcomes far more than aggressive posturing. You now understand how courts calculate support amounts, what financial evidence carries weight, and which negotiation structures serve your interests. These alimony negotiation tips transform abstract legal principles into concrete numbers that strengthen your position at the negotiation table.

Most divorces settle because both parties recognize that litigation consumes money, time, and emotional energy that could go toward rebuilding. If your spouse demonstrates good faith through collaborative law and transparent financial disclosure, settlement typically delivers faster results and lower legal fees than court battles. Neutral financial advisors identify tax-efficient structures and divorce coaches keep discussions focused on solving problems rather than attacking character.

However, some situations demand aggressive court representation when your spouse hides assets, refuses financial disclosure, or makes unreasonable demands designed to exhaust your resources. Courts have power to sanction parties who obstruct discovery, and judges respond harshly to bad-faith negotiation tactics. Christine Sue Cook, LLC offers free consultations to evaluate your situation and recommend the right approach without financial pressure.