Make a Payment

850-572-3443

Divorce reshapes your life in ways that demand clear thinking and solid information. At Christine Sue Cook, LLC, we’ve guided countless women through Florida divorces, and we know the decisions you face right now will affect your financial security and your family’s future.

This guide covers what you need to know about your rights, your money, and your legal options. Our divorce advice for women focuses on practical steps you can take today.

Florida doesn’t follow community property rules like some western states do. Instead, Florida courts divide marital assets equitably, which means fairly but not necessarily equally. This distinction matters enormously because it gives judges flexibility to award assets based on each spouse’s contributions, earning capacity, and financial needs rather than a strict 50-50 split. When you file for divorce in Florida, the court separates assets into marital and non-marital property through a process of classification and valuation. Non-marital assets stay with you, but anything purchased during the marriage-even if titled in one name-can be divided. The judge considers factors like the length of your marriage, your role as a homemaker or breadwinner, your age and health, and your earning potential going forward. If you contributed to your spouse’s education or career advancement, that counts too. Courts increasingly recognize that a spouse who stayed home to raise children while the other built a career made valuable contributions that warrant higher asset awards.

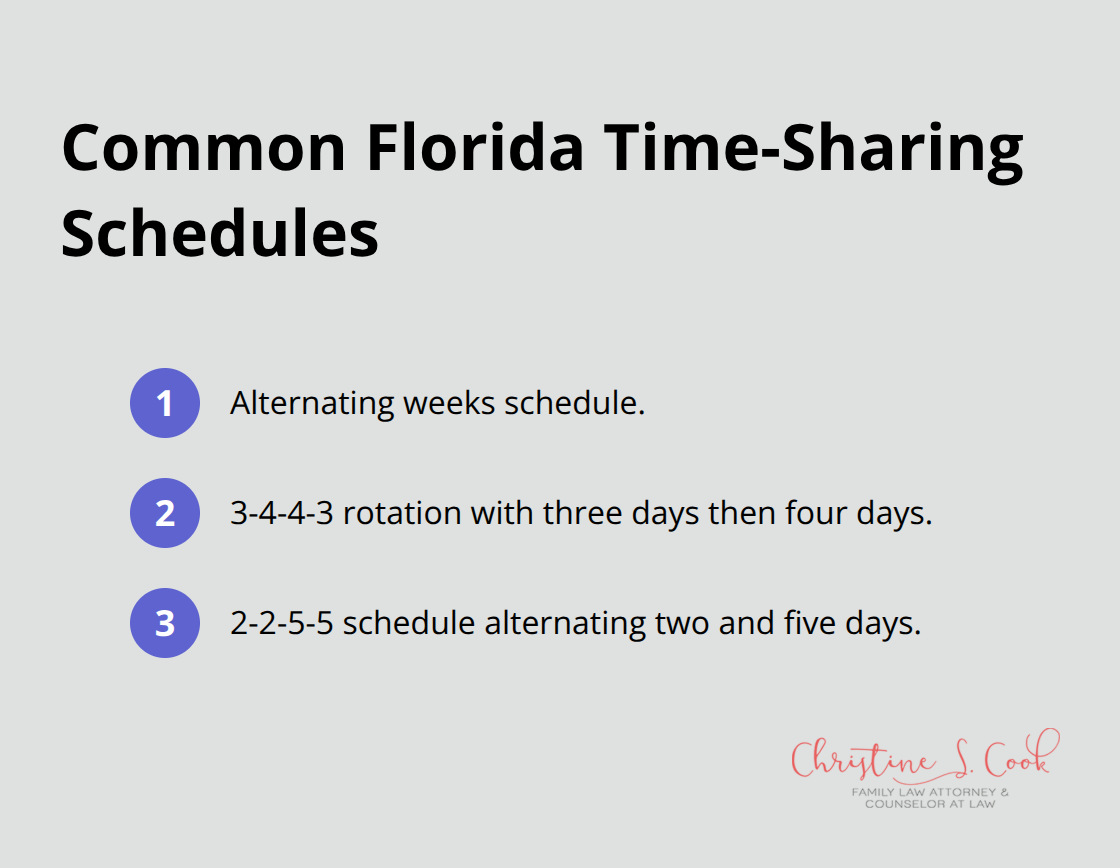

Child custody in Florida operates on two separate concepts: parental responsibility (who makes major decisions about education, healthcare, and religion) and time-sharing (the actual schedule your child spends with each parent). Florida law presumes joint parental responsibility serves the child’s best interest unless one parent has a history of abuse, violence, or substance abuse. For time-sharing schedules, common arrangements include alternating weeks, a 3-4-4-3 rotation (three days with one parent, four with the other), or a 2-2-5-5 schedule. The judge examines which parent can better foster a healthy relationship with the other parent, maintain stability in school and community, and meet the child’s physical and emotional needs. Your ability to co-parent matters more than winning a custody battle.

If both parents agree on custody terms, the court typically approves uncontested arrangements quickly, saving thousands in legal fees and emotional strain. A Guardian ad Litem may be appointed to investigate and advocate for your child’s interests, and their recommendations carry substantial weight with judges.

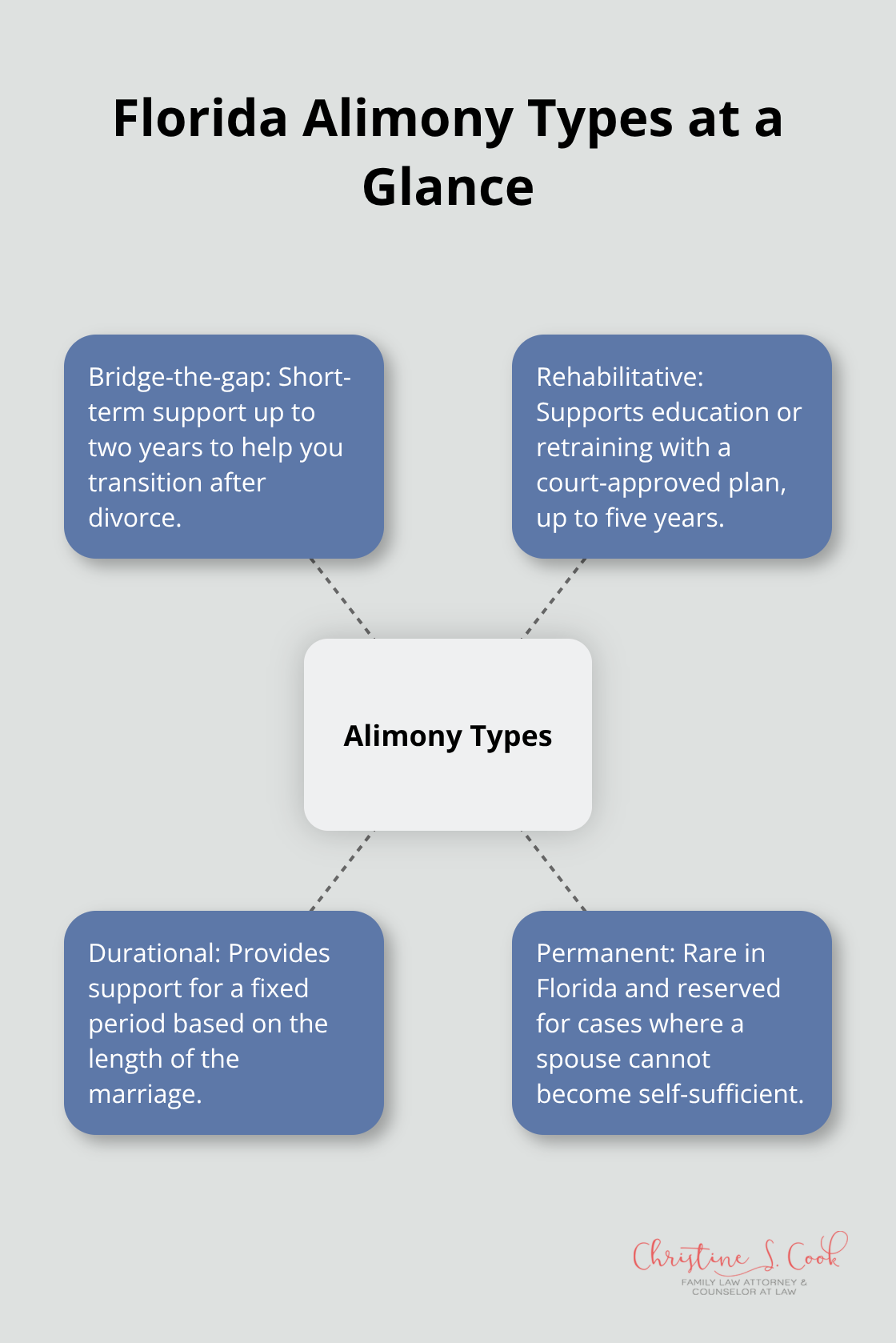

Florida recognizes four types of alimony with specific purposes and time limits. Bridge-the-gap alimony helps you transition immediately after divorce and lasts no more than two years. Rehabilitative alimony supports your education or retraining to reach self-sufficiency, with a maximum five-year duration and a detailed plan required by the court.

Durational alimony provides support for a fixed period based on marriage length. Permanent alimony is now rare in Florida and requires specific circumstances showing one spouse cannot become self-sufficient. Judges examine your standard of living during marriage, both spouses’ earning potential, the length of the marriage, and contributions like childcare or homemaking. If your ex-spouse committed adultery and that adultery caused economic harm to the marriage, the court can increase your alimony award. You can request spousal support before filing for divorce, and the court can order life insurance to secure ongoing payments. Alimony terminates automatically if you remarry or enter a supportive relationship where you cohabit, present yourselves as married, or achieve financial interdependence-so judges scrutinize long-term partnerships closely.

These three pillars-asset division, custody arrangements, and alimony calculations-form the foundation of your divorce settlement. Understanding how Florida courts approach each one positions you to make informed decisions about your case. The next section addresses how you protect your financial interests throughout this process and build stability for what comes after.

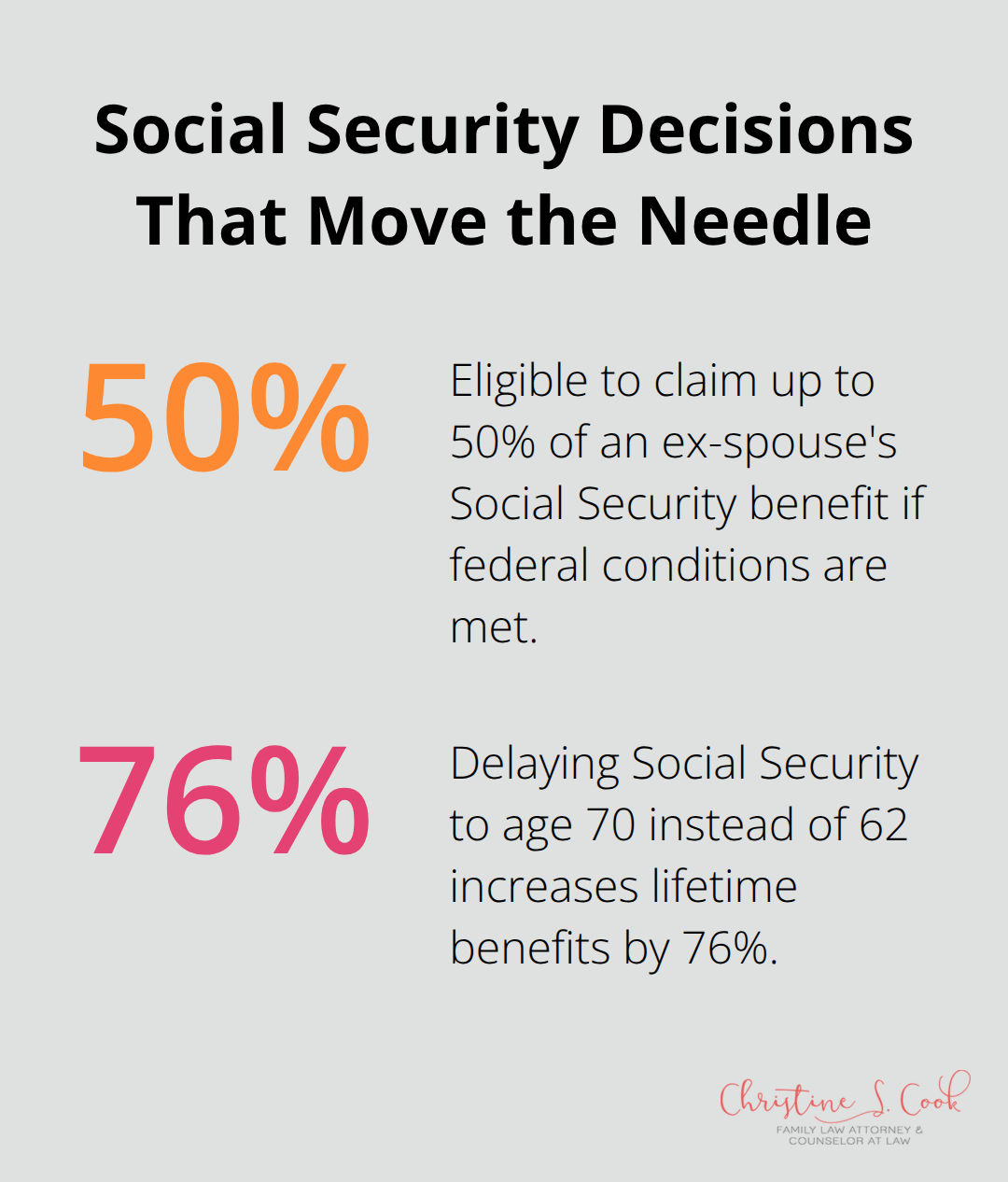

Your financial security after divorce depends on decisions you make right now, during the separation process. Before you sign anything or agree to any settlement, you need a clear picture of your complete financial situation. Collect statements for all bank accounts, investment portfolios, retirement accounts, real estate holdings, and any business interests-both yours and your spouse’s. Many women underestimate the value of retirement assets because they focus only on visible bank balances. In Florida, retirement accounts earned during marriage are marital property subject to division, which means a 401(k) or IRA your spouse built is not off-limits. If your marriage lasted longer than ten years and you remain unmarried, federal law allows you to claim up to fifty percent of your ex-spouse’s Social Security benefits while they receive their full amount, providing substantial long-term income protection.

Debt accumulated during marriage is split equitably too, so if your spouse ran up credit card balances or took out loans, you may be responsible for a portion regardless of whose name appears on the account. Courts can also order life insurance to secure alimony payments, protecting you if your ex-spouse dies before fulfilling obligations. This is why working with a skilled attorney to negotiate your settlement matters-poorly structured agreements leave you vulnerable to years of financial strain. An experienced family law attorney identifies hidden assets, calculates the true value of retirement benefits, and structures settlements that protect your independence going forward.

Open a separate bank account in your name alone and track your individual income and expenses for at least three months before settlement discussions-this data becomes your baseline for child support and alimony calculations. If you’ve been out of the workforce, your earning potential will directly influence how much support you receive and how long it lasts, so document your skills, credentials, and job market reality. Create a realistic post-divorce budget that accounts for housing, utilities, childcare, insurance, food, transportation, and a genuine emergency fund of three to six months of expenses (this safety net prevents you from returning to your ex-spouse for financial help during unexpected crises).

Your credit score will suffer during divorce unless you actively manage it: remove yourself as an authorized user on joint cards, close joint accounts after settlement, and dispute any inaccurate information on your credit report. Some single women see lower insurance costs post-divorce, but you’ll want to review health, auto, and homeowner policies immediately after finalizing your divorce to capture these savings. If you have children heading to college, divorce actually improves your financial aid eligibility because FAFSA calculations may exclude your ex-spouse’s income, potentially qualifying you for significantly more aid.

Start redirecting funds you’d previously given to joint expenses toward retirement savings immediately-women who delay Social Security benefits to age 70 instead of claiming at 62 increase lifetime benefits by seventy-six percent, creating substantial security for later years. These financial decisions you make today establish the foundation for your independence. The next section addresses how you choose the right legal approach to protect these interests throughout your divorce process.

Divorce doesn’t follow a one-size-fits-all process, and the legal approach you choose directly impacts your costs, timeline, and relationship with your ex-spouse going forward. Collaborative law and traditional litigation represent fundamentally different philosophies, and your situation determines which one protects your interests most effectively.

In collaborative divorce, both spouses and their attorneys commit to resolving disputes outside court through structured negotiation and professional involvement from financial experts, child specialists, or mediators as needed. This approach works best when both parties genuinely want to settle, can communicate without excessive hostility, and prioritize minimizing conflict for children’s sake. Collaborative cases typically resolve in six to twelve months at a fraction of litigation costs, sometimes saving twenty to forty thousand dollars compared to contested court battles.

However, collaborative law fails when your spouse refuses to disclose assets, has a history of controlling or abusive behavior, or shows bad faith negotiation tactics. If you suspect hidden income, undisclosed bank accounts, or deliberate undervaluation of business assets, aggressive court representation becomes necessary because collaborative processes depend on honest participation from both sides. Courts have subpoena power to compel financial disclosure, and judges can sanction parties who withhold information.

Women in high-conflict situations-particularly those with abusive spouses-often need assertive legal representation that doesn’t depend on cooperation. Your spouse’s behavior and willingness to negotiate should drive this decision more than cost considerations alone. If your ex-spouse has already hired an aggressive attorney, refused reasonable settlement offers, or filed motions designed to drain your resources, collaborative law won’t work regardless of your preferences.

Conversely, if both parties acknowledge the marriage is over and want to move forward without prolonged conflict, collaborative processes save time and emotional energy. Start with a confidential consultation with a family law attorney who can evaluate your spouse’s track record, assess whether hidden assets are likely, and recommend the appropriate strategy. Document any patterns of financial control, deception, or intimidation during your marriage-these patterns often continue through divorce and indicate you’ll need court protection.

The quality of your legal representation matters far more than whether you choose collaboration or litigation. An attorney who understands Florida’s equitable distribution rules, alimony guidelines, and custody standards can structure settlements that protect your long-term interests even in amicable cases. Poorly negotiated agreements leave women vulnerable to modification disputes, inadequate child support calculations, or alimony structures that don’t account for inflation or career changes.

Your attorney should explain each settlement term in plain language, show you how proposed arrangements compare to what a court would likely award, and never pressure you to accept terms quickly. Schedule consultations with multiple attorneys before deciding, ask specifically about their experience with cases similar to yours, and verify they understand your priorities regarding custody, financial security, and post-divorce independence. Your attorney should also evaluate whether your children would benefit from reduced conflict through collaborative settlement or whether your ex-spouse’s behavior makes aggressive representation necessary to protect custody arrangements.

Your divorce in Florida will test your resilience, but it doesn’t have to derail your future. The decisions you make now about asset protection, custody arrangements, legal strategy, and financial planning determine whether you emerge stronger and more secure or vulnerable to ongoing disputes and financial strain. Florida law gives you specific protections-equitable distribution considers your contributions to the marriage, custody decisions prioritize your child’s stability, and alimony calculations follow clear guidelines based on marriage length and earning capacity.

Your financial independence after divorce depends on actions you take right now: gather complete financial information, protect yourself against hidden debt, and build a realistic post-divorce budget before you sign anything. Women who delay these steps often accept inadequate settlements they later regret, and the difference between a well-structured agreement and a poorly negotiated one can mean tens of thousands of dollars over your lifetime. Choosing the right legal approach matters equally-collaborative law saves money when your spouse negotiates in good faith, but aggressive court representation becomes necessary when you face deception, control, or abuse.

We at Christine Sue Cook, LLC provide compassionate divorce advice for women tailored to your circumstances, whether you need collaborative settlement or aggressive court representation. Contact us for a free consultation to discuss your situation and secure your future with experienced guidance.