Make a Payment

850-572-3443

Most Florida families face a confusing choice: should you create a will, a trust, or both? We at Christine Sue Cook, LLC help families answer this question every day, and the answer depends entirely on your situation.

This wills trusts Florida overview breaks down exactly what each option does, how they work differently, and which path protects your family best.

A will is fundamentally a document that directs how your probate assets get distributed after you die. That’s it. Many people believe a will handles everything, but it covers only assets titled in your individual name without a beneficiary designation or survivorship rights. Your bank account with your name alone on it? The will controls that. Your house held as tenants by the entirety with your spouse? That passes directly to your spouse outside the will. Your life insurance policy with a named beneficiary? That goes straight to whoever you named, bypassing the will entirely.

This distinction matters because people often create wills thinking they’ve handled estate planning, when really they’ve only addressed a portion of their assets. A will also names your executor (called the personal representative in Florida), who manages the probate process, pays your debts and taxes, and distributes what remains.

Florida Statute 732.502 requires just two elements for a valid will: your signature and two witnesses present at the same time. Notarization isn’t required, though a notarized will becomes self-proved under Florida Statute 732.503, which speeds up probate admission since the court doesn’t need to track down witnesses to verify signatures.

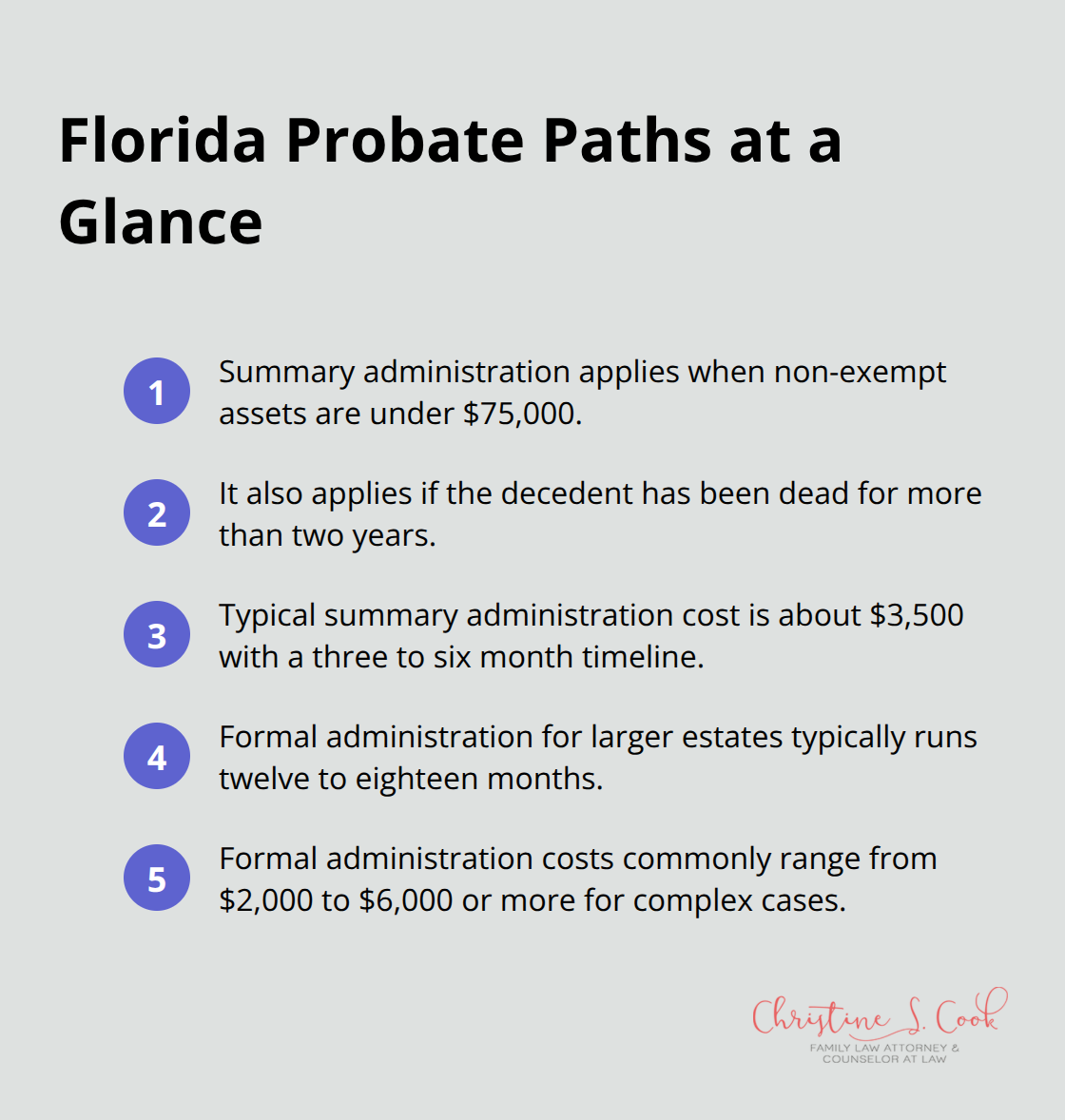

After you die, probate begins only if you leave behind probate assets. Florida offers two paths depending on your estate size. Summary administration handles estates with non-exempt assets under $75,000 (rising to $150,000 on July 1, 2026), or any estate if you’ve been dead for more than two years. This route costs roughly $3,500 and takes three to six months.

Formal administration applies to larger estates and typically runs twelve to eighteen months, with costs ranging from $2,000 to $6,000 or higher for complex situations. During formal administration, creditors receive notice to file claims under Florida Statute 733.2121. If someone fails to file within the required deadlines, they lose the right to collect.

Court filing fees run $345 to $405, and publication costs reach around $250, with attorney fees varying widely. The personal representative must post a bond (unless waived in the will), notify all interested parties, secure assets, pay eligible debts, file tax returns, and eventually distribute remaining assets to beneficiaries named in your will or, if no will exists, according to Florida’s intestacy rules.

Understanding what a will covers-and what it doesn’t-helps you see why many Florida families need more than just a will to protect their entire estate. That’s where trusts enter the picture.

A trust operates during your lifetime and continues after death without court involvement, unlike a will. When you create a trust, you transfer ownership of your assets into the trust itself, naming yourself as the initial trustee. You maintain complete control and can buy, sell, or manage those assets exactly as you did before. The trust document specifies who receives those assets when you die or become incapacitated. This structure means your assets skip probate entirely because they never belonged to you individually at death-they belonged to the trust.

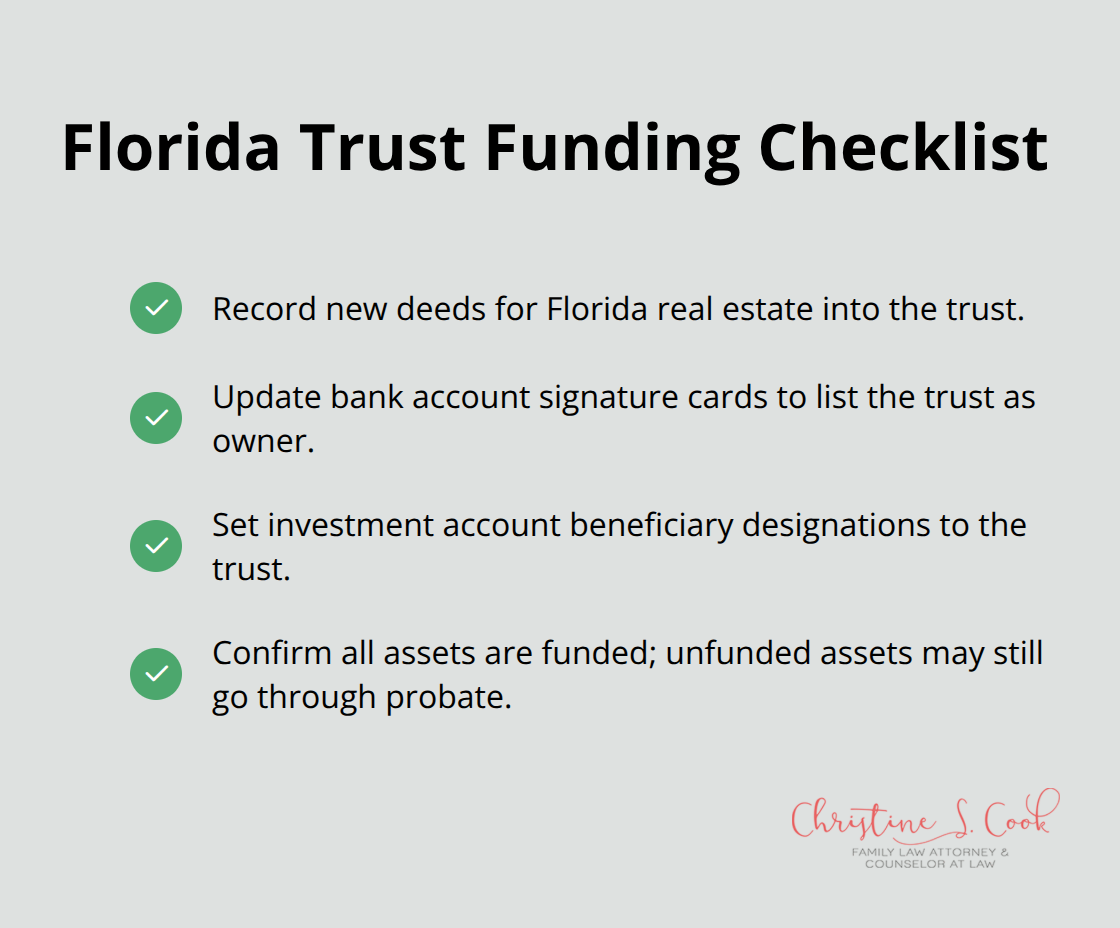

Florida Statute Chapter 736 governs trusts, and the revocable living trust has become the most practical tool for Florida families wanting to avoid probate’s costs and delays. Unlike a will that only addresses probate assets, a trust can hold bank accounts, real estate, investment accounts, vehicles, and personal property. The key difference is that a trust requires funding-you must actually transfer asset titles and ownership into the trust’s name. Many people create trusts but fail to fund them, which defeats the entire purpose.

Real estate requires new deeds prepared by an attorney to account for mortgages and homestead protections under Florida Constitution Article X, Section 4. Bank accounts need signature cards changed to reflect the trust as owner. Investment accounts require beneficiary designations naming the trust. Without proper funding, those assets still go through probate, and you’ve paid for a trust that doesn’t work.

A revocable living trust can be changed, amended, or completely revoked during your lifetime, which gives you flexibility if circumstances change. After you die or become mentally incapacitated, it becomes irrevocable, and your successor trustee manages distributions according to your instructions without court supervision. How trusts work in Florida typically costs $2,500 to $4,000 to establish with an attorney, plus funding costs for real estate deeds.

An irrevocable trust cannot be modified once created, which sounds restrictive but actually provides genuine asset protection from creditors and potential estate tax reduction. Irrevocable trusts are appropriate for specific situations like special needs planning under 42 U.S.C. Section 1396p(d)(4)(A), where a disabled beneficiary must have limited control over funds to preserve Medicaid eligibility. In Florida, a single person receiving needs-based benefits faces asset limits around $2,000 in countable assets, so an irrevocable special needs trust preserves access to government support while allowing family to provide additional care.

Irrevocable trusts also offer creditor protection that revocable trusts do not-assets inside an irrevocable trust are generally protected from the grantor’s creditors during life and from beneficiaries’ creditors after distribution with proper spendthrift language. Most Florida families benefit from a revocable trust during life combined with irrevocable provisions that activate after death for specific beneficiaries who need protection. Understanding these two trust structures helps you see why the choice between a will and a trust isn’t always straightforward-and why many families actually need both tools working together to fully protect their estate.

A will alone makes sense if your estate is small, your assets are already structured to avoid probate, or you simply cannot afford trust-based planning right now. If you own a home as tenants by the entirety with your spouse, maintain pay-on-death bank accounts, and carry life insurance with named beneficiaries, a will handles the remaining probate assets efficiently. For someone with less than $75,000 in non-exempt assets, summary administration under Florida Statute 35 costs roughly $3,500 and concludes in three to six months, making probate affordable and straightforward. A will also costs far less upfront-typically $300 to $800 compared to $2,500 to $4,000 for a revocable trust-which matters if your budget is tight.

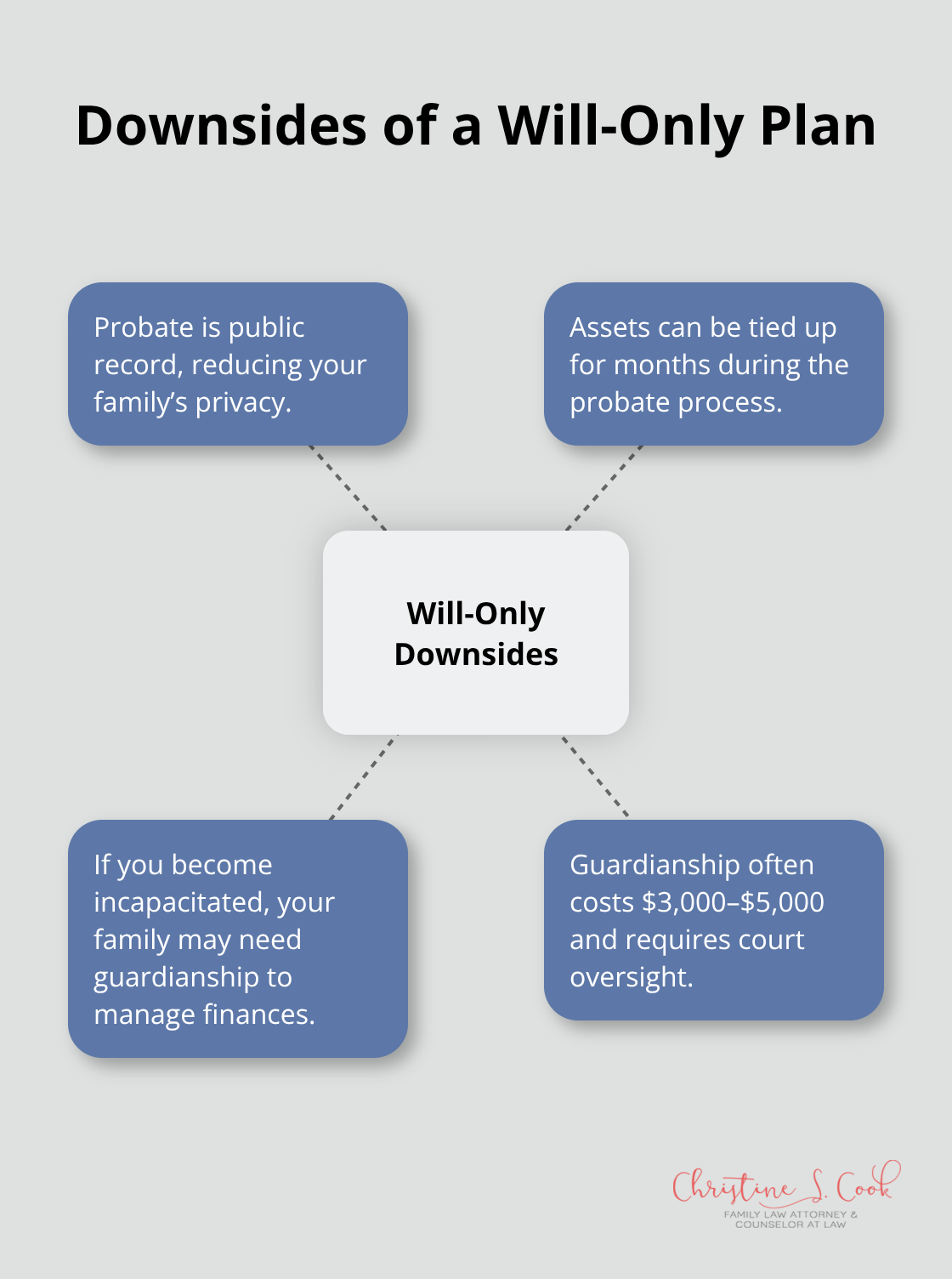

However, this approach carries real downsides. Probate becomes public record, the process ties up assets for months, and if you become mentally incapacitated, your family still needs to file for guardianship to manage your finances, which costs $3,000 to $5,000 and requires court oversight.

A trust becomes the better choice once your estate complexity increases or privacy matters. If you own real estate in Florida, hold investment accounts, or want to avoid the public probate process entirely, a revocable living trust transfers those assets outside probate without court delays. Trusts also provide incapacity planning-if you become incapacitated, your successor trustee simply manages assets without guardianship proceedings.

For blended families where both spouses have children from prior relationships, a trust prevents unintentional disinheritance by specifying exactly which assets go to which children, something a will alone cannot guarantee if the surviving spouse remarries and changes their own will. Parents of minor children benefit from trusts because assets can remain in the trust under a third-party trustee’s management rather than passing to a court-appointed guardian who may not align with your values.

If you have a disabled child or family member who receives Medicaid or SSI benefits, an irrevocable special needs trust preserves government benefits while allowing family to provide supplemental support-a will offers no such protection.

Many Florida families actually need both documents working together: a revocable living trust holds your major assets and avoids probate, while a pour-over will catches any assets accidentally left outside the trust and names your executor and guardians for minor children. This combination costs more upfront but eliminates probate costs, provides incapacity planning, maintains privacy, and ensures your family avoids months of court involvement at a time when they’re already grieving.

The choice between a will, a trust, or both depends on your family’s specific situation, not on what works for your neighbor or what you read online. A simple will costs less upfront and handles small estates efficiently through summary administration. A revocable living trust costs more initially but eliminates probate delays, maintains privacy, and protects your family from court involvement during incapacity. Many Florida families discover that combining both documents provides the strongest protection, especially when children, blended families, or special needs beneficiaries are involved.

Your answers to a few honest questions determine whether a will alone suffices or whether a trust-based plan makes sense for your situation. How large is your estate? Do you own real estate or investment accounts? Are there minor children or disabled family members who need protection? Do you want to avoid probate’s public process? This wills trusts Florida overview covers the fundamentals, but your actual plan must account for your unique circumstances, current Florida law, and tax implications.

An experienced estate planning attorney reviews your complete financial picture, identifies assets that should transfer outside probate, structures trusts properly to avoid costly mistakes, and ensures your documents comply with Florida Statute requirements. We at Christine Sue Cook, LLC help Florida families navigate exactly this decision through tailored estate planning services designed specifically for your needs. Contact us today to schedule your free consultation and take the first step toward protecting your family’s future.