Probate can feel overwhelming when you’re grieving a loved one. The Florida probate process involves multiple steps, court filings, and timelines that most families have never navigated before.

We at Christine Sue Cook, LLC help families understand what to expect and how to move through probate with confidence. This guide breaks down each stage so you can see the path forward clearly.

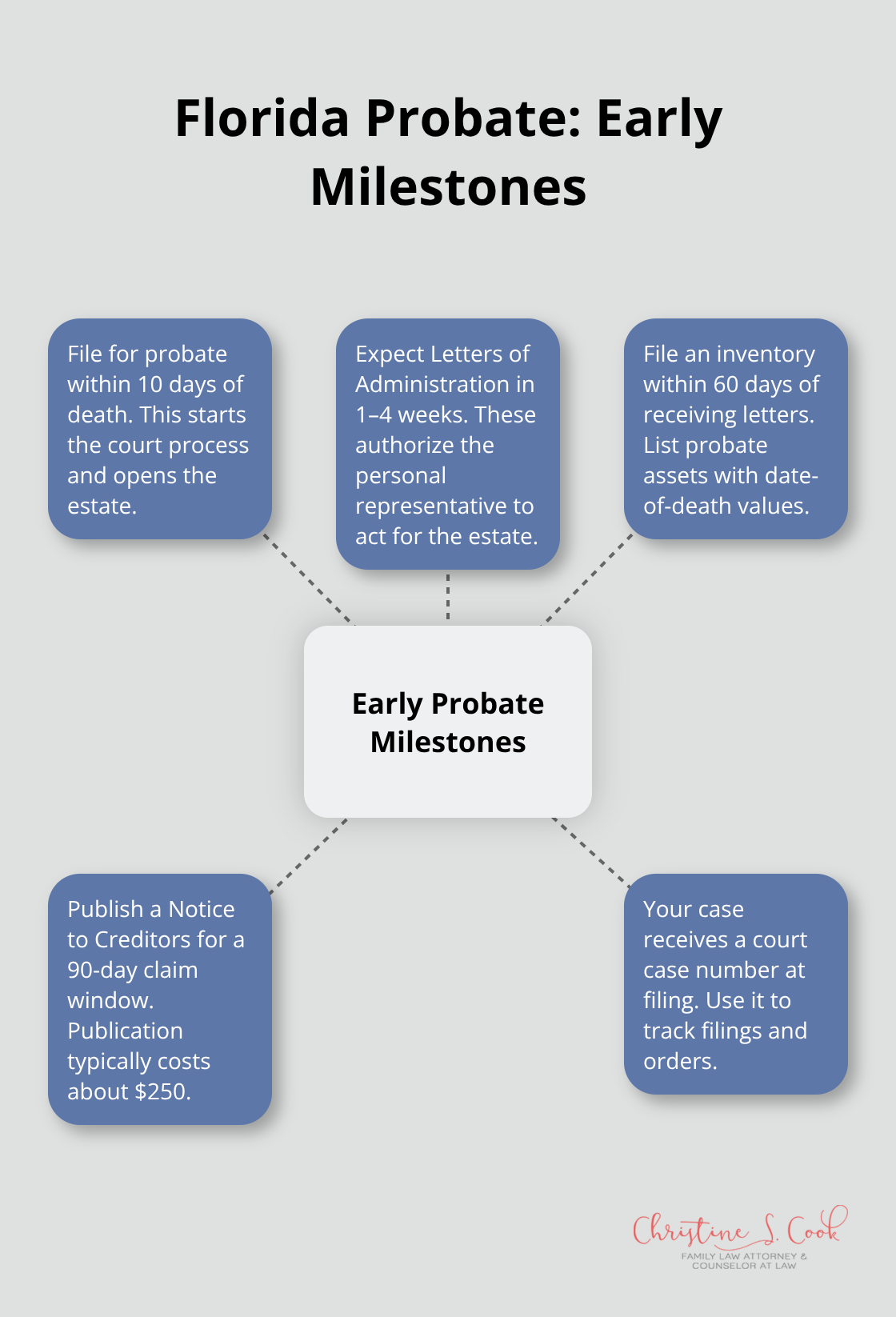

Filing for probate in Florida must occur within 10 days of the decedent’s death, regardless of estate size. You’ll file the original will and probate petition at the clerk of the circuit court in the county where the decedent lived. The filing fee ranges from $345 to $405 depending on the county, and the clerk will assign your case a number. Within one to four weeks, the court issues Letters of Administration, which authorize the personal representative to act on behalf of the estate. This document provides your legal permission to access bank accounts, manage property, and handle other estate matters. Without Letters of Administration, banks and creditors won’t recognize your authority, so obtaining this document marks your first real milestone in the probate process.

Once you have Letters of Administration, you need to locate and document everything the decedent owned. This includes bank accounts, investment accounts, real estate, vehicles, jewelry, and household items. You must file an inventory with the court within 60 days of receiving your letters, listing all probate assets and their estimated values as of the decedent’s death date. Many families underestimate how much time this takes because assets are scattered across different institutions and some accounts require death certificates to access. Create a spreadsheet with each asset, its location, account numbers, and approximate value so you don’t miss anything. Digital assets like email accounts and cryptocurrency often go unnoticed, but they’re part of the estate too. The inventory you file becomes a public court record, so protect sensitive information like account details when possible.

After probate opens, you must publish a Notice to Creditors in a local newspaper, typically running for two consecutive weeks. This notice informs creditors that they have 90 days from the date of publication to file claims against the estate. The publication cost runs about $250, and you need to provide proof of publication to the court. This creditor period applies to nearly every Florida probate. Many families want to rush distributions before the creditor period ends, but the law prohibits that. The statute protects the estate from surprise creditor claims that surface months later. During these 90 days, you should review any claims that arrive carefully, verify their legitimacy, and determine what portion the estate should pay. Valid claims get paid from estate assets before beneficiaries receive anything, so this period directly affects what heirs ultimately inherit.

The creditor period and asset inventory phase set the foundation for everything that follows. Once you’ve satisfied these initial requirements, the probate process moves into the next critical stage-managing the overall timeline and understanding the costs involved. The decisions you make now about how thoroughly you handle creditor claims and asset documentation will influence how smoothly the rest of your probate proceeds.

Simple Florida probate estates wrap up in three to six months, while more complex cases stretch into a year or beyond. The Florida Bar’s consumer guidance confirms that straightforward administrations average around five to six months from filing to final distribution. Your timeline depends heavily on estate complexity, the number of creditors, whether beneficiaries agree on everything, and whether the will itself faces challenges. A $50,000 estate with one bank account and no debts moves fast. A $500,000 estate with real property, multiple accounts, and contested creditor claims takes significantly longer.

The 90-day creditor notification period you just completed isn’t optional-it anchors your entire schedule. You cannot distribute assets to beneficiaries until that window closes and you’ve resolved valid claims. If your estate involves real property sales, tax disputes, or beneficiary disagreements, add another three to six months minimum. Managing probate timelines and costs typically involves straightforward cases taking 10-15 months from filing to final distribution, according to Florida probate standards, though this assumes no major complications arise. Setting realistic expectations now prevents frustration later.

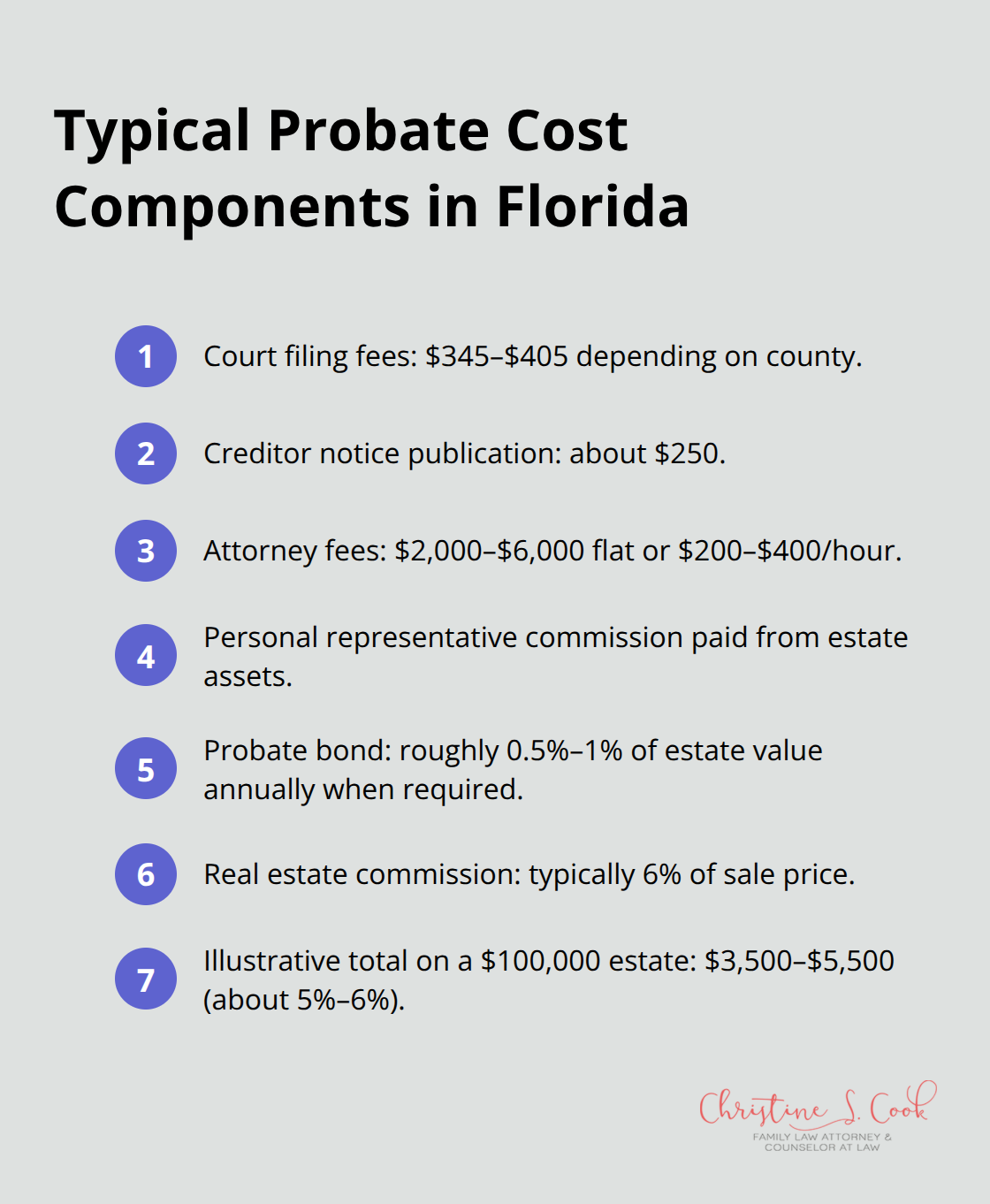

Probate costs in Florida break down into several categories that add up quickly if you’re not careful. Filing fees range from $345 to $405 depending on your county, and the creditor notice publication costs around $250. If you hire an attorney-which we strongly recommend for formal administrations-you’re looking at either flat fees or hourly rates.

Flat-fee arrangements for straightforward probate typically run $2,000 to $6,000, while hourly rates average $200 to $400 per hour depending on the attorney’s experience and location.

Personal representative fees in Florida probate are entitled to a commission payable from the estate assets without court order as compensation for ordinary services. Probate bonds, required in some cases, cost roughly one-half to one percent of estate value annually. Real estate commissions (if property sales occur) typically run six percent of the sale price. The cumulative effect matters: a $100,000 estate might cost $3,500 to $5,500 in total probate expenses, eating up five to six percent of what beneficiaries receive.

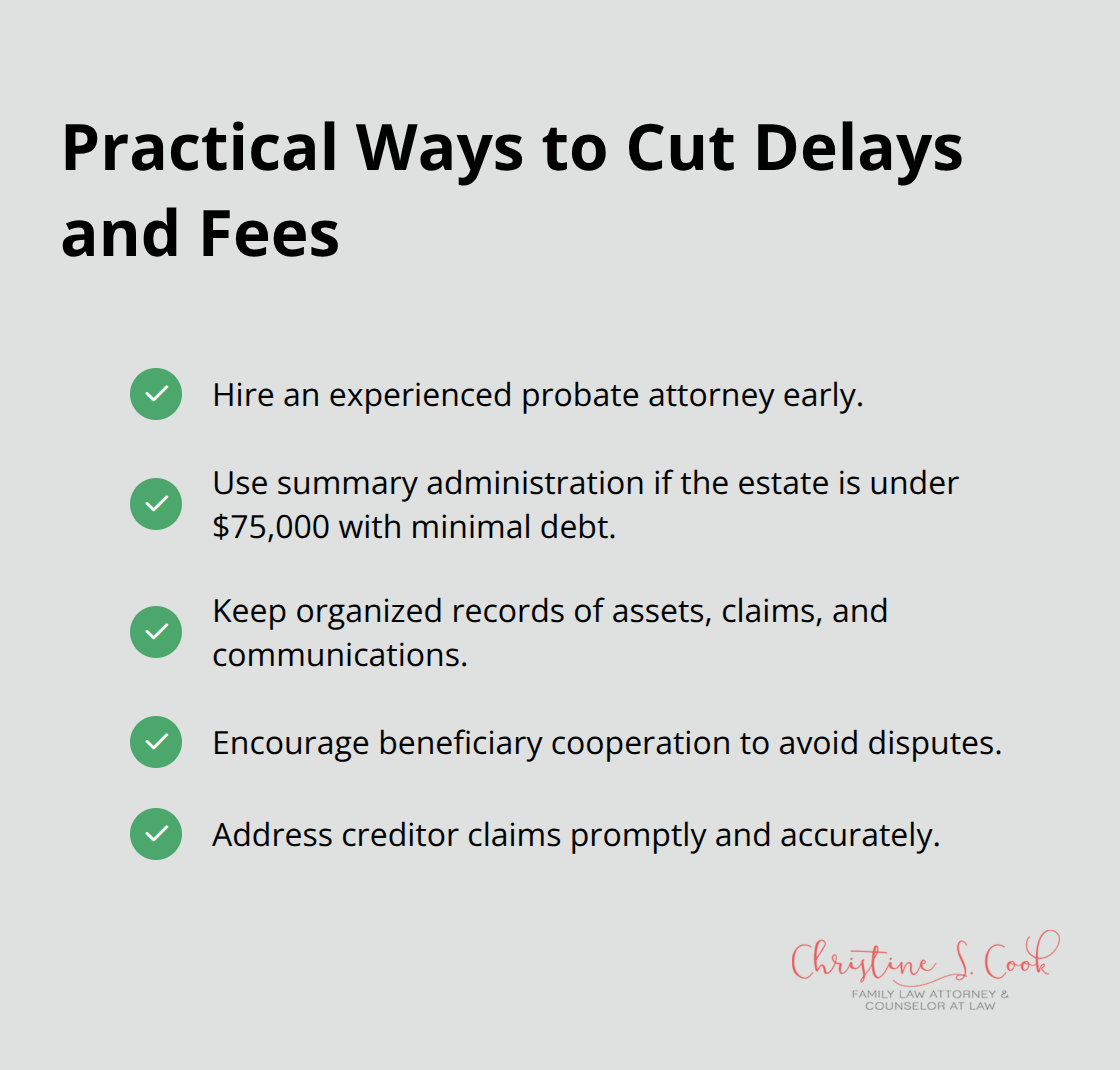

Reducing these costs requires strategic planning from the start. An experienced probate attorney prevents expensive mistakes, missed deadlines, and disputes that multiply costs exponentially. An attorney who spots issues early and handles creditor claims efficiently saves thousands in unnecessary delays and court hearings.

Summary administration, available for estates under $75,000 with minimal debt, costs substantially less-often just $1,500 to $3,000 total-and completes in weeks rather than months. If your estate qualifies, pursuing summary administration instead of formal probate saves significant time and money.

Staying organized throughout probate also cuts costs: maintain detailed records of all communications, creditor claims, and asset values so your attorney doesn’t spend billable hours reconstructing information. Beneficiaries who cooperate and avoid disputes prevent litigation expenses that can dwarf initial probate costs. These practical steps directly influence what heirs ultimately receive and how quickly the estate closes. Understanding your specific costs and timeline now allows you to make informed decisions about which probate path makes the most sense for your family’s situation.

Most families don’t realize that a will doesn’t avoid probate-it actually guarantees probate happens. A will is a probate document that tells the court how to distribute your assets after you die, which means your estate still goes through the entire court process we just described. If avoiding probate costs and timeline matters to you, a revocable living trust works differently. A trust transfers ownership of your assets into the trust during your lifetime, so those assets aren’t owned by you individually when you die. Since the trust owns the property, not you personally, those assets pass directly to your beneficiaries through the trust document without court involvement.

No probate filing, no creditor notification period, and no judge approval are needed when you use a trust. The trustee you name simply distributes assets according to your instructions. A revocable trust costs roughly $1,500 to $2,500 to set up with an attorney, which sounds expensive until you compare it to probate costs plus the months of delay. For estates over $75,000, the math favors trusts almost every time.

Pay-on-death designations and enhanced life estate deeds (Lady Bird deeds) offer simpler alternatives if trusts feel like overkill. Banks allow you to name a beneficiary on savings and checking accounts who receives the funds automatically when you die, bypassing probate entirely for that account. Life insurance policies and retirement accounts already have beneficiary designations that work the same way. A Lady Bird deed lets you keep control of your Florida home during your lifetime while automatically transferring it to your named beneficiary after death, costing roughly $250 to $350 to prepare.

These strategies work well for specific assets but don’t solve the full picture if you own multiple properties, significant investments, or want to control how and when beneficiaries receive money. A beneficiary who inherits a large sum immediately might mismanage it or face creditor problems, whereas a trust lets you stagger distributions or protect assets from your heir’s creditors. Homestead property in Florida already receives strong creditor protection under the Florida Constitution, but non-homestead real estate and investment accounts have no such shield.

If you own property outside Florida, trusts become even more valuable because ancillary probate-a separate court process in each state where you own real property-adds thousands in costs and months to your timeline. A trust handles multi-state property seamlessly without triggering ancillary probate in other states. The federal estate tax exemption sits at fifteen million dollars per individual as of 2026, so most Florida families won’t face federal taxes, but state-specific planning still matters for asset protection and efficient distribution.

Florida probate doesn’t have to feel like a mystery once you understand the filing deadlines, the 90-day creditor period, the costs involved, and the timeline you face. Most straightforward estates move through the Florida probate process in five to six months, while summary administration wraps up in weeks for smaller estates. The key is knowing which path fits your situation and staying organized throughout.

Probate becomes manageable when you have clear information and professional support. Families who file on time, document assets thoroughly, and handle creditor claims properly avoid the expensive disputes and delays that derail other estates. You also learned that probate isn’t inevitable-a revocable living trust, pay-on-death accounts, or enhanced life estate deeds eliminate probate entirely for your loved ones, saving them months of court involvement and thousands in costs.

If you’re facing probate now, contact an attorney to review your timeline and costs. If you’re planning ahead, schedule a consultation to discuss whether a trust or other strategies fit your goals. At Christine S. Cook, LLC, we offer free consultations to discuss your estate planning needs without financial pressure.