Property division is one of the most contentious issues in any divorce. Getting it wrong can cost you thousands of dollars and years of regret.

At Christine Sue Cook, LLC, we’ve helped countless clients navigate this process and walk away with agreements that actually protect their interests. This guide walks you through the legal framework, negotiation strategies, and critical mistakes to avoid when creating a property division agreement.

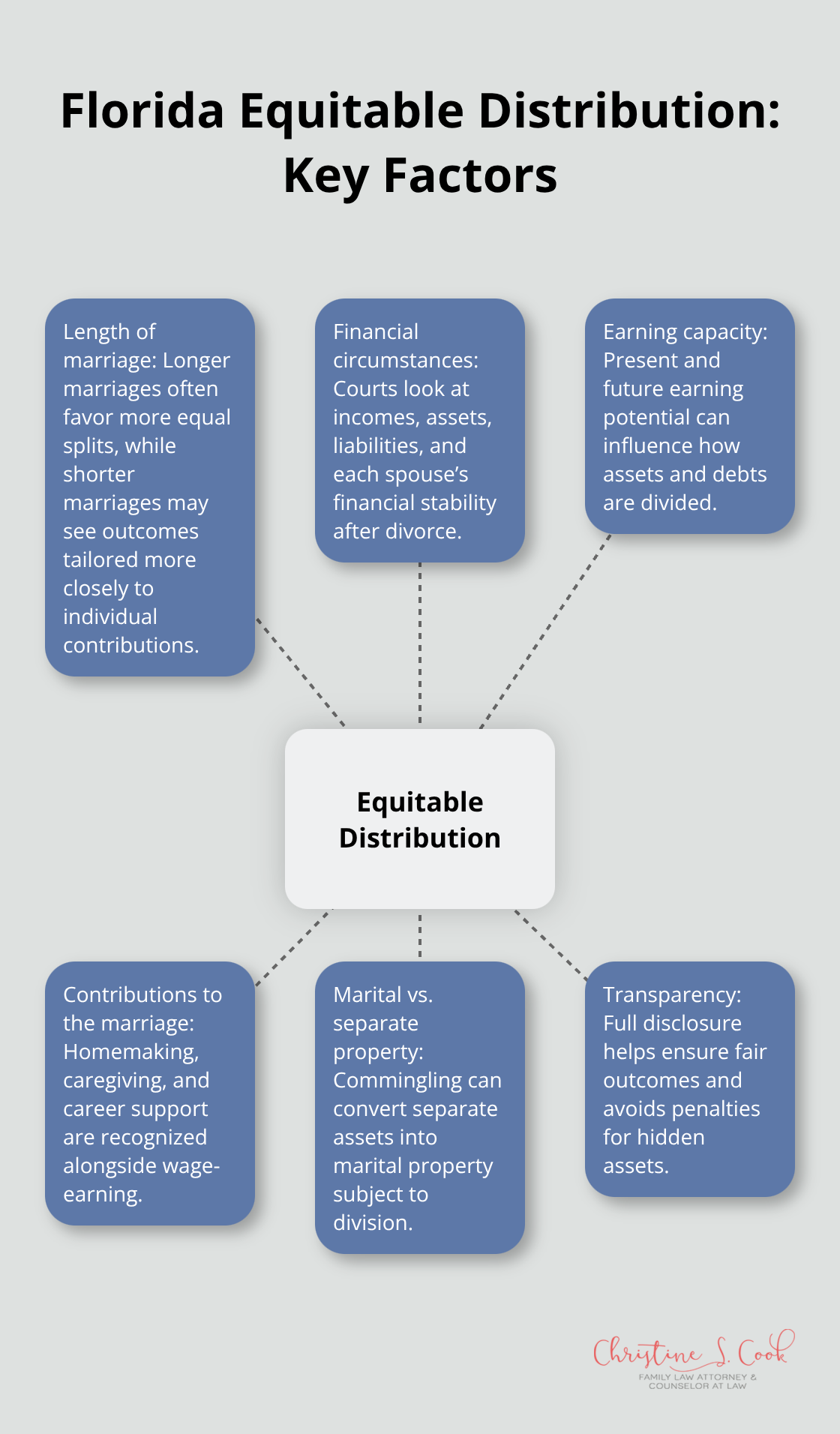

Florida uses equitable distribution, not community property, which means the court divides marital assets fairly but not necessarily 50/50. This distinction matters because it shifts the burden away from an automatic equal split and toward what a judge deems fair based on specific circumstances. In Florida, marital property includes anything acquired during the marriage, regardless of whose name appears on the title. If you purchased a home during your marriage, invested in retirement accounts, or accumulated business interests while married, courts will treat these as marital assets subject to division.

Separate property-assets you owned before marriage, inherited, or received as gifts-remains yours, but this protection disappears if you commingle funds. For example, if you inherited $100,000 and deposited it into a joint account with your spouse, that inheritance can transform into marital property over time. Courts examine the source of funds and how you treated the asset throughout your marriage. Keeping separate accounts and maintaining clear records protects your interests when divorce proceedings begin.

Courts in Florida evaluate several factors when determining what constitutes a fair division. The length of your marriage heavily influences outcomes; a 20-year marriage produces different results than a 5-year union. Your financial circumstances, earning capacity, and contributions to the marriage all matter.

If one spouse stayed home raising children while the other built a career, Florida courts recognize homemaking as a valuable contribution worthy of consideration.

The court also examines whether asset appreciation during marriage resulted from marital efforts versus market conditions. Hidden assets complicate everything, so full disclosure is mandatory. If your spouse conceals bank accounts, business interests, or real estate holdings, courts can impose penalties that shift more assets your way. Complete financial transparency from the start prevents disputes that waste time and money later. With these legal principles in mind, your next step involves gathering the documentation that proves what you own and what you owe.

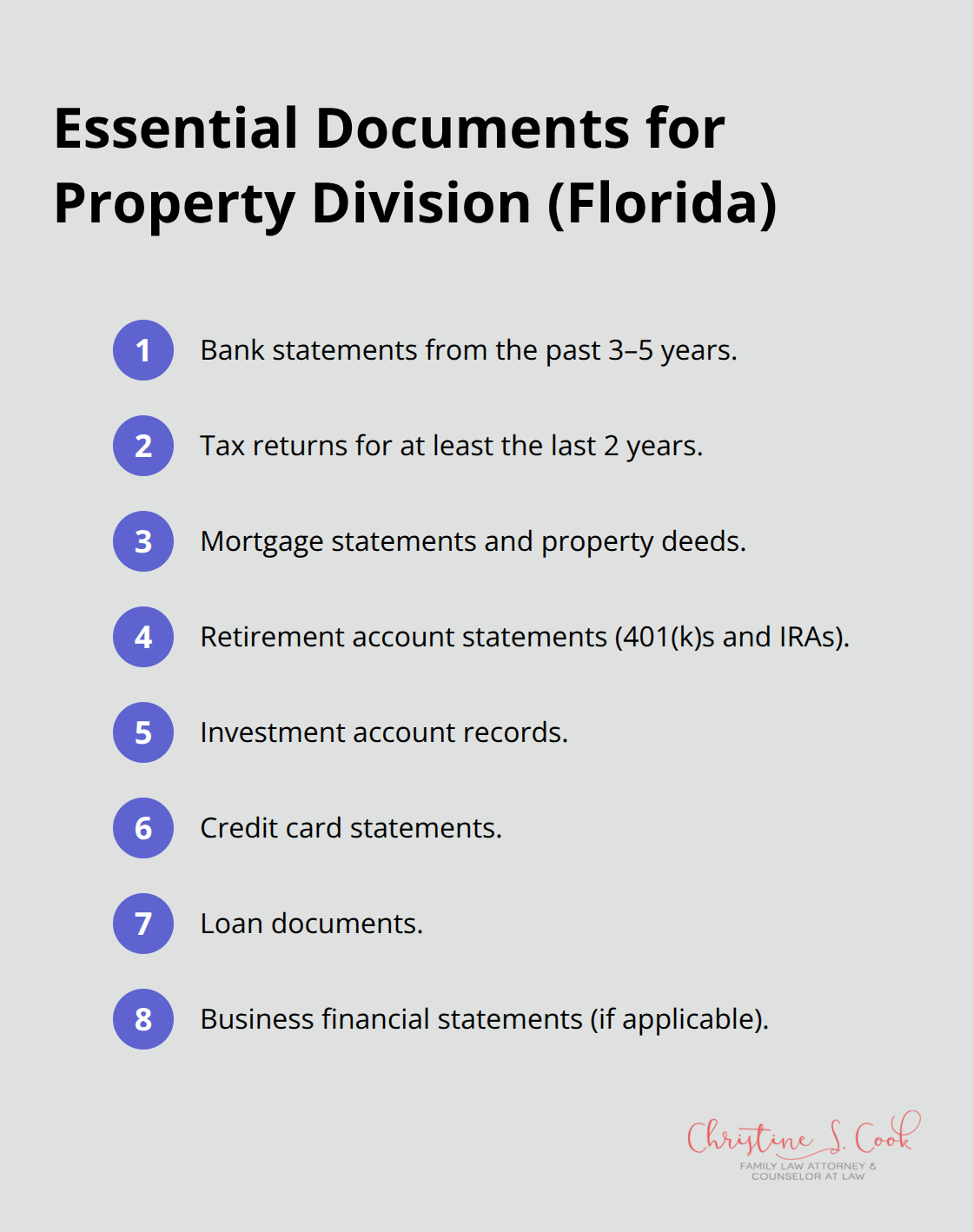

Negotiating a fair property division agreement starts with one non-negotiable step: gathering complete financial documentation before anything else happens. Most people underestimate how much paperwork matters, but courts in Florida require full disclosure, and incomplete records sabotage your negotiating position immediately. You need bank statements from the past three to five years, tax returns for at least the last two years, mortgage statements, property deeds, retirement account statements including 401(k)s and IRAs, investment account records, credit card statements, loan documents, and any business financial statements if either spouse owns a business. Store these documents in a dedicated digital folder with clear naming conventions so you can reference specific accounts without confusion.

The moment your spouse sees you have organized, comprehensive records, their leverage shrinks because they cannot claim assets were forgotten or undervalued. If you cannot locate a statement, request it from the financial institution immediately rather than hoping it surfaces later; delays create gaps that courts interpret unfavorably.

Once you have the documentation, resist the temptation to assign values yourself. Real estate requires a professional appraisal from a state-licensed appraiser, not an online estimate or your neighbor’s opinion about comparable homes. Vehicles need valuation through sources like NADA Guides or Kelley Blue Book using current market data for the specific year, make, model, and condition. Retirement accounts are valued at their statement balance as of the separation date, but complex accounts like pensions or stock options demand a certified financial planner or forensic accountant. If either spouse owns a business, hiring a certified business valuator is essential because business value directly impacts the division outcome and courts scrutinize these valuations heavily. The cost of professional valuations (typically $500 to $3,000 per asset depending on complexity) pays for itself many times over by preventing disputes that drag out negotiations for months. Many people skip this step to save money upfront, then lose far more in extended legal fees and unfavorable settlements.

Debts matter equally to assets in property division. List every liability including mortgages, car loans, credit card balances, personal loans, and tax obligations with current balances and interest rates. Courts divide debts alongside assets, so a spouse who receives more assets may accept more debt as part of the bargain, or vice versa. This balanced approach prevents one party from walking away with all the valuable property while the other carries all the financial obligations.

Working with professionals during this phase sounds expensive, but it protects you from costly mistakes. A tax advisor reviews how different division scenarios trigger capital gains taxes, depreciation recapture, or retirement account withdrawal penalties so you understand the true after-tax value of each asset.

If you divide a 401(k) without a Qualified Domestic Relations Order, the non-employee spouse faces immediate taxation and penalties that could consume 30 to 40 percent of the account value. A forensic accountant identifies hidden accounts, traced funds, and undisclosed income that your spouse might otherwise conceal. These professionals also strengthen your negotiating position because you arrive at the negotiation table with documented, defensible valuations that opposing counsel cannot easily challenge. With solid documentation and professional valuations in hand, you’re ready to move into the negotiation phase where strategy and legal expertise determine whether you achieve a settlement that truly protects your financial future.

Nondisclosure of assets stands as the single most destructive error in property division, and Florida courts punish it severely. When you fail to report bank accounts, investment holdings, or real estate, you trigger forensic accounting investigations that expose everything while damaging your credibility permanently. Courts in Florida impose sanctions including attorney’s fees, increased asset awards to the other spouse, and in extreme cases, contempt charges.

Full disclosure means every financial account, every property deed, every retirement statement, and every liability gets reported on official court forms under oath. You cannot claim ignorance about accounts in your spouse’s name alone; discovery processes force production of bank statements, credit card records, and business financial statements regardless of whose name appears. The IRS Form 1040 you both filed jointly provides a starting point because it shows income sources that must connect to corresponding accounts. If your spouse reports $150,000 in annual income but you cannot locate corresponding bank deposits, that discrepancy signals hidden assets worth investigating immediately.

Hidden debts create equal chaos because courts divide liabilities alongside assets. A spouse who conceals credit card debt, personal loans, or tax liens forces you to either accept responsibility for debts you did not create or extend negotiations while forensic accountants trace financial activity. Courts examine credit reports, subpoena credit card companies, and review loan documents to identify undisclosed obligations. Once discovered, hidden debt typically gets assigned entirely to the spouse who incurred it, but only after your legal fees multiply investigating the deception.

Tax implications wreck more settlements than any other single factor because people divide assets without understanding the after-tax consequences. When you receive a brokerage account with $200,000 in unrealized gains, you inherit a future capital gains tax bill of approximately $30,000 to $50,000 depending on your tax bracket and holding period. Your spouse receives a 401(k) worth $200,000 in current value but avoids taxes until withdrawal, making the accounts unequal despite matching valuations.

A tax professional should model three to five division scenarios showing after-tax outcomes before you accept any settlement proposal. Ignoring depreciation recapture on rental properties, Section 1231 gains on business assets, and net unrealized appreciation on employer stock costs thousands in unexpected taxes after the divorce finalizes. Courts in Florida do not automatically adjust divisions for tax consequences, so the burden falls on you to identify these issues during negotiation rather than discovering them on your first post-divorce tax return.

Creating a fair property division agreement requires discipline, documentation, and professional guidance. The three mistakes we covered-nondisclosure, hidden debts, and tax blindness-destroy more settlements than any other factors, so avoiding them protects your financial future immediately. You now understand Florida’s equitable distribution framework, know what documentation matters, and recognize which assets demand professional valuation.

The reality is that most people underestimate property division complexity until they face it directly. A property division agreement that looks fair on paper can cost you tens of thousands in taxes or hidden liabilities discovered years later. Courts in Florida require full transparency, and judges scrutinize valuations carefully, so shortcuts backfire when your spouse’s attorney challenges weak documentation and unsupported valuations.

Contact Christine Sue Cook, LLC to discuss your property division needs with an experienced family law attorney. We help clients navigate property division with both collaborative approaches when possible and aggressive representation when necessary. Take action now rather than hoping issues resolve themselves-gather your documentation, schedule professional valuations before negotiations begin, and work with legal counsel who understands that your financial security depends on getting this right the first time.