Retirement accounts often represent the largest marital asset in a Florida divorce, yet many people don’t understand how they’re divided.

At Christine Sue Cook, LLC, we’ve seen countless cases where improper handling of these accounts costs clients thousands in unnecessary taxes and penalties. Dividing retirement accounts in divorce Florida requires specific legal steps and careful planning to protect your financial future.

Florida law treats retirement accounts earned during marriage as marital property subject to division, regardless of whose name appears on the account. The specific type of account determines how division happens and what legal tools you need. Understanding these differences prevents costly mistakes that can reduce your retirement security by tens of thousands of dollars.

A 401(k) plan requires a Qualified Domestic Relations Order, or QDRO, to divide it without triggering immediate taxes and early withdrawal penalties. Only the portion you contributed during the marriage is divisible; contributions made before marriage remain yours alone. If you contributed $300,000 to your 401(k) during a 15-year marriage but started the job five years before marriage, roughly two-thirds of that account is marital property.

Vesting schedules matter significantly. If your employer matches contributions, only the matched portions that vested during the marriage are divisible. The U.S. Bureau of Labor Statistics reports that employer matches typically range from 3 to 6 percent of salary annually. Many people fail to account for these matches, which can represent substantial value over time.

A 403(b) plan used by nonprofits and schools follows identical division rules to a 401(k). The QDRO must be drafted before or immediately after divorce finalization. Delaying QDRO preparation risks losing benefits if a spouse dies, since the plan pays the account holder’s estate instead of the alternate payee named in an unexecuted order.

IRAs do not require a QDRO for division; instead, the divorce settlement authorizes a direct rollover to the ex-spouse’s own IRA. This distinction matters because it speeds up the transfer process. A Roth IRA follows the same division process as a traditional IRA but carries different tax consequences.

Contributions to a Roth IRA made during marriage are marital property, but the tax-free growth inside a Roth remains protected after transfer if the receiving spouse maintains it as a Roth IRA. Many people mistakenly withdraw IRA funds as cash instead of rolling them directly to a new IRA, triggering a 10 percent early withdrawal penalty plus income taxes on the full amount. The IRS allows direct rollovers without these penalties when done through the financial institution, not through your personal bank account.

A pension earned during marriage is divisible even if you haven’t retired yet. The QDRO calculates your share based on how long you were married while earning the pension. If you were married for 10 years of a 20-year career with the same employer, roughly half the pension is marital property.

Government pensions, including those from the Florida Retirement System, accept QDROs in most cases. Military retirement pay follows the Uniformed Services Former Spouses Protection Act, which allows division only if a former spouse was awarded a portion as property in the final court order. Municipal pensions sometimes refuse QDROs, requiring your attorney to pursue alternative strategies like valuing the pension and offsetting it with other assets.

The QDRO must specify whether the ex-spouse receives a lump sum, monthly payments starting at retirement, or survivor benefits if the employee spouse dies before retirement. Each plan type carries unique requirements, and mistakes in QDRO language can cost you thousands in lost benefits or unexpected tax bills. The next section covers the legal framework that governs these divisions and the specific steps required to execute them properly.

Florida treats retirement accounts earned during marriage as marital property subject to equitable distribution, which means fair division-not necessarily 50/50 splits. Florida Statutes Section 61.076 governs this division, and the law applies regardless of which spouse’s name appears on the account. The court considers the length of your marriage, each spouse’s financial contributions, economic circumstances, and debts when determining how to split retirement assets. A 15-year marriage typically results in a more equal division than a 5-year marriage, though judges retain discretion to adjust splits based on your specific circumstances.

The critical step is identifying exactly which portions of your retirement accounts are marital versus non-marital. If you contributed to a 401(k) for five years before marriage and then continued for ten years during marriage, only the ten years of contributions and growth qualify for division. This calculation requires pulling statements from the date of marriage and the date of divorce filing to establish the marital balance accurately. Plan administrators can provide valuations at both dates, which prevents disputes over what amount actually qualifies for division.

A Qualified Domestic Relations Order (QDRO) is the legal document that actually transfers retirement benefits from one spouse to another without triggering immediate taxes or penalties. Without a QDRO, your plan administrator pays the entire account to the titled spouse’s estate, leaving your ex-spouse with minimal recovery options. The QDRO must be drafted specifically for your plan type because a 401(k) QDRO differs significantly from a pension QDRO or an IRA transfer order.

For 401(k)s and 403(b)s, the QDRO directs the plan administrator to transfer a percentage or dollar amount of the marital balance to the ex-spouse’s account or a rollover IRA. For pensions, the QDRO calculates the ex-spouse’s share using a formula based on years of service during marriage divided by total years of service, then specifies whether benefits arrive as monthly payments or a lump sum. Military retirement pay follows the Uniformed Services Former Spouses Protection Act and caps the ex-spouse’s share at 50 percent of the service member’s retired pay.

The QDRO drafting and approval process typically takes four to twelve weeks depending on plan requirements and court calendars, so delaying this step risks losing benefits if a spouse dies before the order executes. Plan administrators review QDROs for compliance with their specific plan language, and rejections can occur if the order fails to meet technical requirements. Coordinating directly with your plan administrator during drafting prevents costly delays or rejections that could extend the timeline significantly.

Tax consequences differ dramatically based on how you handle the transfer. A proper QDRO transfer between retirement accounts avoids immediate taxation because the funds stay within tax-advantaged accounts. However, taking retirement funds as cash triggers ordinary income taxes plus a 10 percent early withdrawal penalty if you’re under age 59½, potentially reducing your share by 30 to 40 percent.

The IRS allows direct rollovers from 401(k)s and pensions to IRAs without these penalties, but only when the financial institution handles the transfer directly-never through your personal bank account.

Roth IRA conversions carry special considerations because converting traditional IRA funds to a Roth during or after divorce creates a taxable event in that year, even though the transfer itself is authorized by the divorce settlement. Municipal and some federal pensions may refuse to honor QDROs entirely, requiring your attorney to pursue alternative strategies like valuing the pension and offsetting it with other marital assets of equal worth. These complexities make professional legal guidance essential to protect your retirement security and avoid unexpected tax bills that could significantly reduce your settlement value. The next section covers the common mistakes that cost people thousands of dollars and how to prevent them.

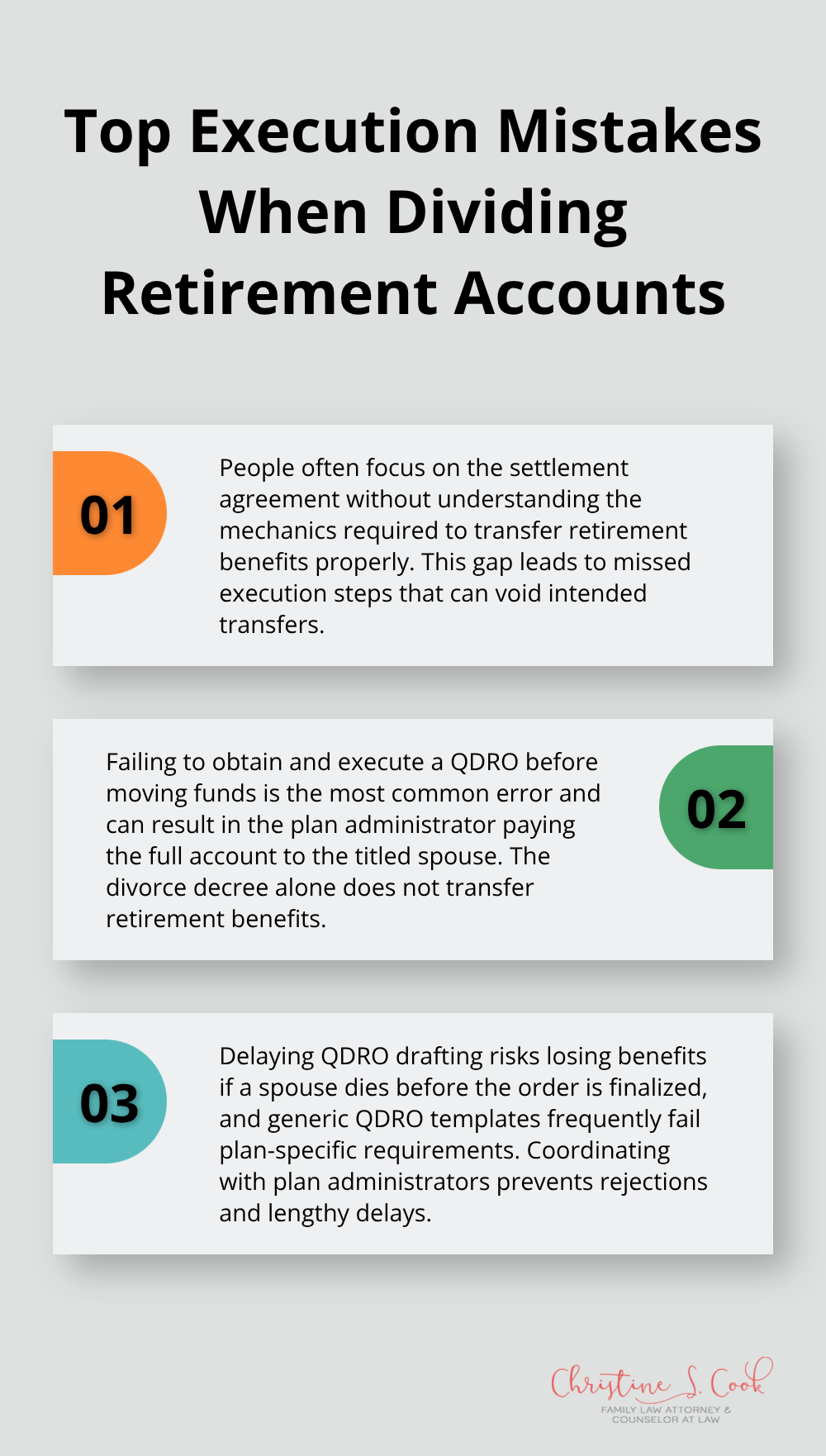

Most people make critical errors when dividing retirement accounts because they focus on the settlement agreement without understanding the execution mechanics. The biggest mistake occurs when people fail to obtain a QDRO execution requirement before transferring funds from a 401(k) or pension. Many assume the divorce decree automatically transfers retirement benefits, but it does not.

Without a QDRO, the plan administrator pays the entire account to the titled spouse’s estate, and your ex-spouse has no legal claim to the funds.

If you withdraw funds as cash without a QDRO in place, you trigger immediate income taxes plus a 10 percent early withdrawal penalty if you’re under 59½. A $200,000 401(k) withdrawal without proper QDRO authorization can cost $60,000 to $80,000 in taxes and penalties, leaving only $120,000 to $140,000. The QDRO must be drafted and submitted to the plan administrator before any transfer occurs.

Timing matters intensely here. If your spouse dies before the QDRO executes, the alternate payee designation becomes worthless, and the account goes to your ex’s estate instead of you. Draft the QDRO simultaneously with finalizing your divorce, not weeks or months later. Contact the plan administrator before settlement negotiations conclude to confirm their specific QDRO requirements and timeline. Different plans demand different language, and a generic QDRO template fails to comply with your specific plan’s rules, resulting in rejection and months of delays.

The second critical mistake involves mishandling tax consequences across different account types. Many people do not realize that direct rollovers from 401(k)s to IRAs avoid taxes entirely, while cashing out the account triggers ordinary income tax plus penalties. The IRS allows direct rollovers only when the financial institution transfers funds directly between accounts, not when you personally receive a check and deposit it.

Taking personal receipt of funds starts a 60-day rollover clock, and most people miss the deadline, converting the entire amount to a taxable distribution. Roth IRA divisions create additional complexity because the receiving spouse receives tax-free growth after transfer, but converting traditional retirement funds to a Roth during divorce creates a taxable event in that year. IRAs do not require QDROs like 401(k)s do, but improper transfer methods still trigger unnecessary taxes that reduce your actual settlement value significantly.

The third mistake involves overlooking vesting schedules and employer match contributions. Many people fail to identify which portions of employer matches actually vested during the marriage. If your employer matches 5 percent of salary but uses a three-year vesting schedule, only matches from three years before divorce finalization count as marital property.

A $100,000 balance might include only $40,000 in marital contributions if significant portions have not vested. Government and municipal pensions present unique challenges because some refuse to honor QDROs entirely, requiring alternative strategies like valuing the pension and offsetting it with other assets. Organizing your accounts systematically through property division documentation helps identify these hidden costs before settlement finalizes. These complexities demand experienced legal guidance to protect your actual settlement value and avoid costly tax surprises after divorce finalizes.

Dividing retirement accounts in a Florida divorce requires precision at every step, from identifying marital versus non-marital portions to executing a properly drafted QDRO before funds transfer. A single error in QDRO language, a missed deadline, or an improper withdrawal method can reduce your settlement value by 30 to 40 percent through unnecessary taxes and penalties. The three critical takeaways are straightforward: obtain a QDRO before any transfer occurs, understand the tax consequences specific to your account type, and verify vesting schedules and employer contributions before settlement finalizes.

Florida’s equitable distribution law gives you the right to a fair share of retirement benefits earned during marriage, but claiming that share requires following specific legal procedures that most people handle incorrectly without professional guidance. Dividing retirement accounts in divorce Florida involves technical execution that demands coordination with plan administrators and compliance with specific plan requirements. We at Christine Sue Cook, LLC handle this technical work so you avoid costly mistakes that destroy retirement security.

Your next step is scheduling a consultation to review your specific retirement accounts and understand how Florida law applies to your situation. Contact Christine Sue Cook, LLC to discuss your divorce and retirement division strategy without financial pressure. The sooner you address these accounts with experienced legal guidance, the sooner you can move forward with confidence that your retirement future is protected.