Becoming a trust administrator is a significant responsibility that many people don’t fully understand until they’re already in the role. If you’ve recently been named to manage a trust, you probably have questions about what comes next.

We at Christine Sue Cook, LLC have helped countless families navigate trust administration in Florida. In this guide, we’ll share practical trust administration Florida tips to help you manage assets confidently and avoid costly mistakes.

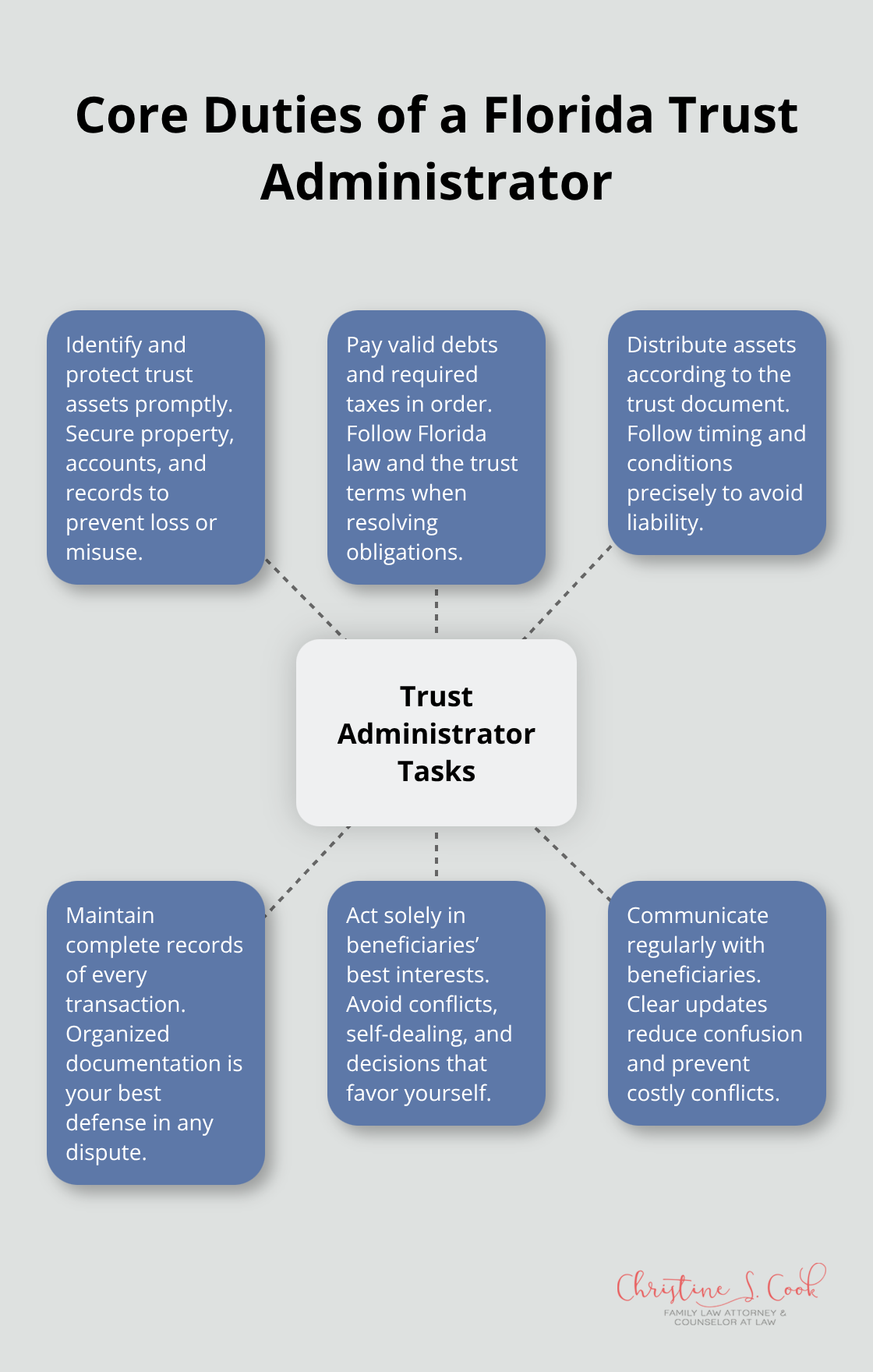

As a trust administrator in Florida, you manage four essential tasks: identifying and protecting trust assets, paying debts and taxes, distributing money to beneficiaries according to the trust document, and maintaining complete records. Florida Statute Chapter 736 requires you to follow the trust terms exactly, act only in your beneficiaries’ best interests, and communicate regularly with them. Most administrators don’t realize that their role starts immediately after the grantor’s death or incapacity-not months later. You secure assets, notify beneficiaries within a reasonable timeframe, and organize financial records as quickly as possible to move through administration faster.

Simple trusts wrap up in three to six months, while larger estates with multiple properties or complex assets can stretch nine to eighteen months. Many administrators delay these initial steps, thinking they have unlimited time, which only creates confusion and frustration for beneficiaries waiting for updates.

Your fiduciary duties carry real personal liability if you breach them. You must invest trust assets prudently, diversify investments to minimize risk unless the trust document says otherwise, keep detailed records of every transaction, and provide beneficiaries with regular accountings. Florida law holds you accountable for these obligations, and courts take violations seriously. The trustee role demands that you act with care, skill, and diligence in managing assets. Failure to meet these standards exposes you to personal liability and potential legal action from beneficiaries.

Three common errors land administrators in legal trouble. First, you fail to properly title assets in the trust’s name, which defeats the purpose of trust planning and can force assets through probate anyway. Second, you make investment decisions without considering the trust’s goals or beneficiary needs, which violates your duty to invest prudently. Third, you keep poor or incomplete records, which prevents you from proving you acted appropriately if beneficiaries later question your decisions. Another serious error is self-dealing-using trust assets for your own benefit or making decisions that favor you over other beneficiaries. This violation of your duty of loyalty can result in personal liability and damage to family relationships.

If you’re unsure about any aspect of your duties, consult a Florida estate planning attorney early rather than guessing and risking personal liability later. Christine S. Cook, LLC offers free consultations to discuss your obligations and help you establish a compliant administration process from the start. An attorney can clarify your specific responsibilities, review your trust document, and guide you through the initial steps that set the tone for successful administration.

With your duties and obligations clear, you’re ready to focus on the practical work ahead-organizing assets, making sound investment decisions, and keeping the records that protect both you and your beneficiaries.

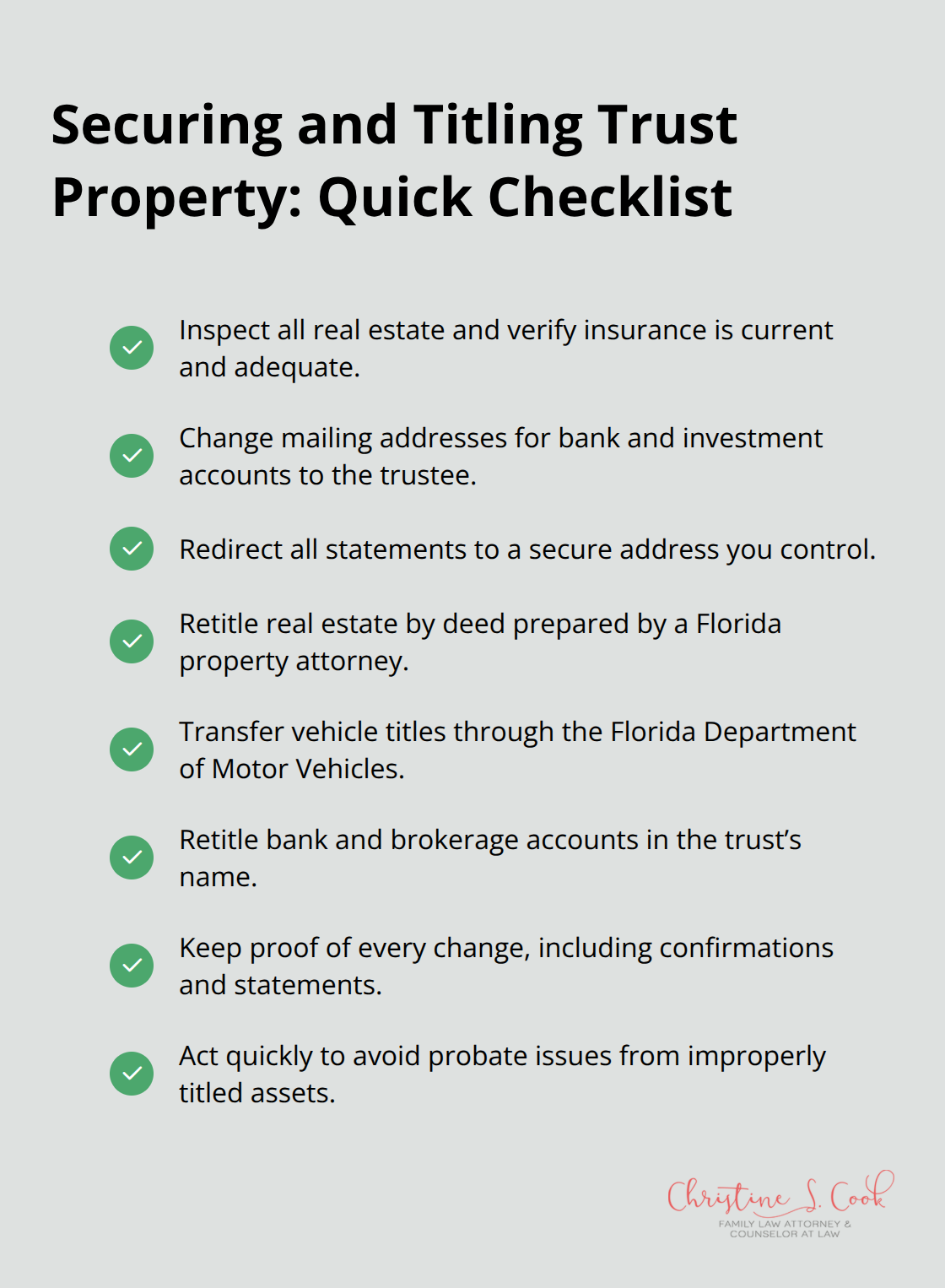

Start asset identification the day you receive notification of your role. Create a master list of everything the trust owns: real estate, bank accounts, investment portfolios, business interests, vehicles, and personal property. Contact the grantor’s financial institutions directly and request statements for the past twelve months. Most administrators waste weeks searching for accounts that a simple phone call could locate in two hours. Once you identify assets, your next step is securing them immediately.

If the trust owns real estate, inspect the properties and verify insurance coverage is current and adequate. For bank and investment accounts, change the mailing address to your own and request all statements be sent directly to you. This prevents mail from going to an empty address where it could be lost or mishandled. Title matters immediately-any asset not already titled in the trust’s name requires retitling as soon as possible.

Real estate needs a deed transfer prepared by an attorney familiar with Florida property law. Vehicles require title transfers through the Florida Department of Motor Vehicles. Brokerage accounts and bank accounts must be retitled in the trust’s name. Failing to retitle assets ranks among the most expensive mistakes administrators make because improperly titled assets may still require probate, defeating the entire purpose of the trust.

Many administrators skip this step thinking it’s optional-it absolutely is not.

Florida law requires you to invest and manage trust assets with reasonable care, skill, and diligence. You cannot simply leave money sitting in a savings account earning less than one percent annually when the trust document permits investment in stocks or bonds. You also cannot chase high-risk investments hoping for outsized returns. The standard is what a prudent person in your position would do, balancing growth with appropriate risk for the beneficiaries’ needs.

Diversification is mandatory unless the trust document explicitly states otherwise. If the trust inherited a concentrated position in a single stock, you should develop a plan to gradually diversify that holding to reduce risk. Document your reasoning for each investment decision and keep records showing you consulted with a financial advisor or investment professional if trust assets are substantial. For most trusts, hiring a CPA or financial advisor is not optional-it’s a practical necessity that protects you from liability. These professionals charge fees, but their expertise prevents costly mistakes that would far exceed their cost.

Every transaction requires documentation. When you pay a bill, keep the invoice and cancelled check or bank statement showing payment. When you make an investment, maintain the confirmation statements and transaction records. When you receive income from trust assets, document the source and deposit it into a dedicated trust account rather than mixing it with your personal funds. Your records must show the date, description, amount, and purpose of every transaction.

Create a spreadsheet tracking all income received, expenses paid, investments made, and distributions given to beneficiaries. This documentation becomes your defense if beneficiaries later question your decisions. Courts review these records when disputes arise, and administrators with thorough documentation almost always prevail. Administrators without records lose cases even when they acted appropriately, simply because they cannot prove it. Set a specific date each month to reconcile accounts and review statements. Most trust disputes arise from poor communication and missing documentation, not from honest mistakes in judgment. Spending two hours monthly on record-keeping prevents months of legal battles later.

With your assets organized, titled correctly, and your investment strategy documented, you’re ready to address the financial obligations that come next-paying debts, handling taxes, and ultimately distributing assets to your beneficiaries according to the trust terms.

The moment you’ve been dreading arrives once debts are paid and taxes are filed: you must distribute assets according to the trust document. This step requires precision because Florida law holds you personally liable if you distribute incorrectly. You need to review the trust document word-for-word to understand exactly what each beneficiary receives and when. Some trusts specify outright distributions immediately after administration closes, while others require assets to remain in continuing trusts for certain beneficiaries or release funds only when specific conditions are met. If the trust says a beneficiary receives their inheritance at age 25, you cannot distribute at age 24 no matter how much they ask. If the trust requires funds to support a beneficiary with special needs while preserving government benefits, a lump sum distribution violates the trust terms and your fiduciary duty. The trust document is your instruction manual, and you expose yourself to personal liability if you deviate from it, even if your intentions are good.

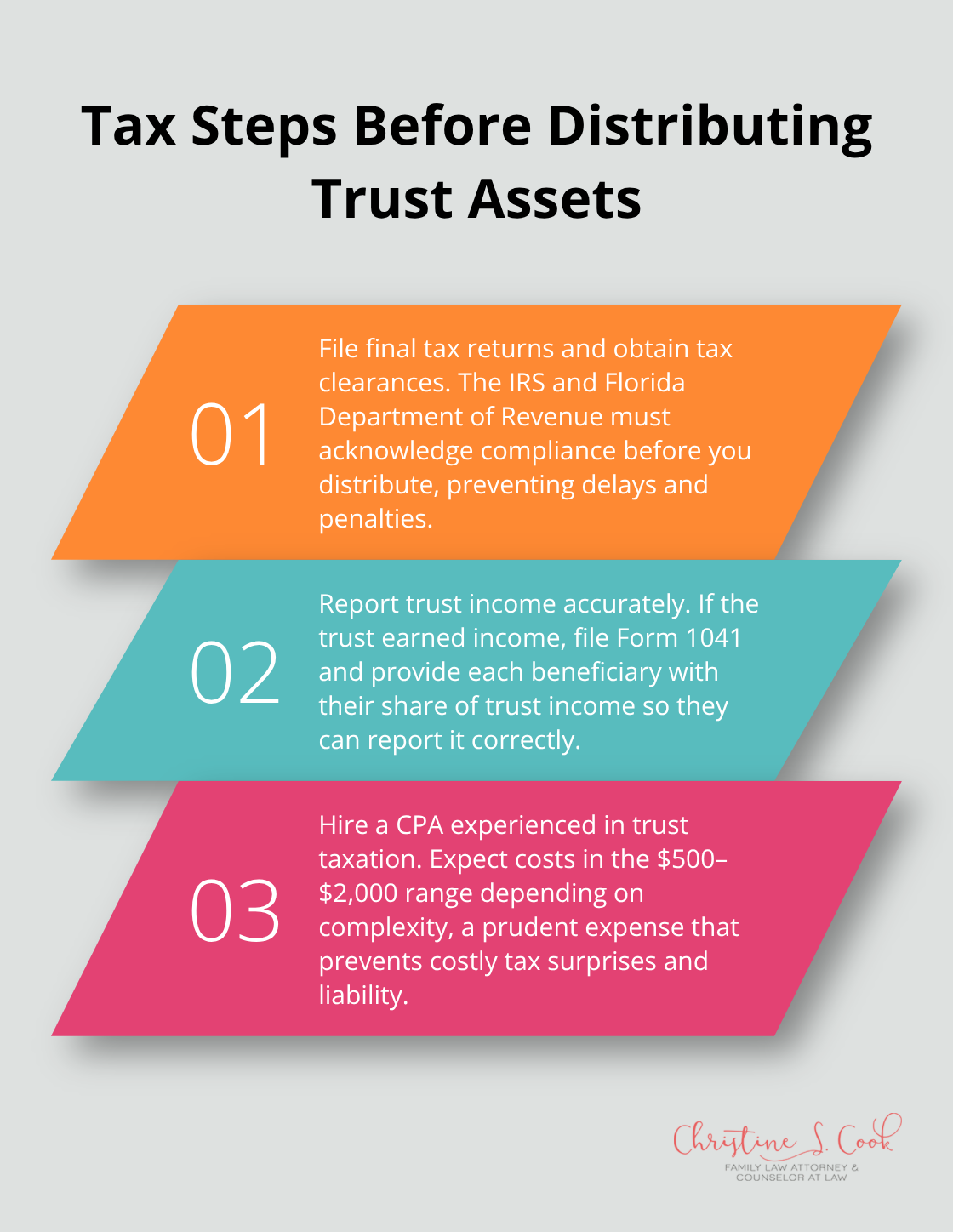

Before you distribute anything, you must file final tax returns and obtain clearance from the IRS and Florida Department of Revenue. If the trust earned income during administration, you file a fiduciary income tax return on Form 1041. Beneficiaries who received distributions need to know their share of trust income for their personal tax returns. Many administrators skip this step or rush it, which creates tax problems for beneficiaries months later.

You should hire a CPA experienced with trust taxation to handle these returns correctly. The cost ranges from $500 to $2,000 depending on complexity, but this investment prevents beneficiaries from owing unexpected taxes and protects you from liability.

You must prepare a final accounting that shows every dollar you received, spent, invested, and distributed. This accounting is not optional under Florida law. Beneficiaries are entitled to see exactly how you managed their trust assets from start to finish. Courts have held administrators personally liable for failing to provide proper accountings, even when their management was otherwise flawless. You need to contact each beneficiary in writing before distributing assets, explaining what they will receive, when they will receive it, and providing copies of the final accounting. You should address questions promptly and honestly. If a beneficiary disputes the accounting, you work with an attorney to resolve the issue before distributing assets. Once you distribute, you find it exponentially harder to recover misdistributed funds if the beneficiary has already spent the money.

Communication during this final phase prevents disputes that could cost thousands in legal fees. You provide each beneficiary with clear written notice of their distribution amount, timing, and the reasoning behind any conditions or delays. You explain how you calculated their share and answer any questions about the final accounting. Transparency builds trust and reduces the likelihood that beneficiaries will challenge your decisions later. If the trust contains complex provisions (such as staggered distributions or conditional releases), you take extra time to explain these terms so beneficiaries understand why they cannot receive their full inheritance immediately. You maintain copies of all communications with beneficiaries, as these records protect you if disputes arise later.

Trust administration in Florida demands attention to detail, clear communication, and a commitment to acting in your beneficiaries’ best interests. The trust administration Florida tips we’ve covered throughout this guide address the core responsibilities that protect both you and your family: securing assets immediately, titling property correctly, investing prudently, maintaining thorough records, handling taxes properly, and distributing according to the trust document. These steps prevent costly mistakes and reduce the likelihood of disputes that damage family relationships and drain resources on legal fees.

You now understand your fiduciary duties under Florida law and the personal liability you face if you breach them. You know how to organize assets, make sound investment decisions, and create documentation that protects you if beneficiaries later question your actions. You understand that distribution requires precision and that communication prevents conflict.

The right time to seek professional guidance is now, not after problems develop. If your trust holds real estate, business interests, or substantial assets, if beneficiaries have special needs or conflicting interests, or if you simply feel uncertain about any aspect of your role, contact Christine S. Cook, LLC to discuss your specific situation and establish a compliant administration process from the start.