Make a Payment

850-572-3443

Divorce can turn your financial world upside down, especially when it comes to mortgages. At Christine Sue Cook, LLC, we often hear mortgage and divorce questions from our clients.

This guide will help you understand your options, legal considerations, and potential challenges when dealing with a mortgage during divorce. We’ll explore refinancing, property division, and strategies to protect your credit throughout the process.

Divorce often complicates financial obligations, especially mortgages. This chapter explores the intricacies of mortgage responsibilities during divorce proceedings.

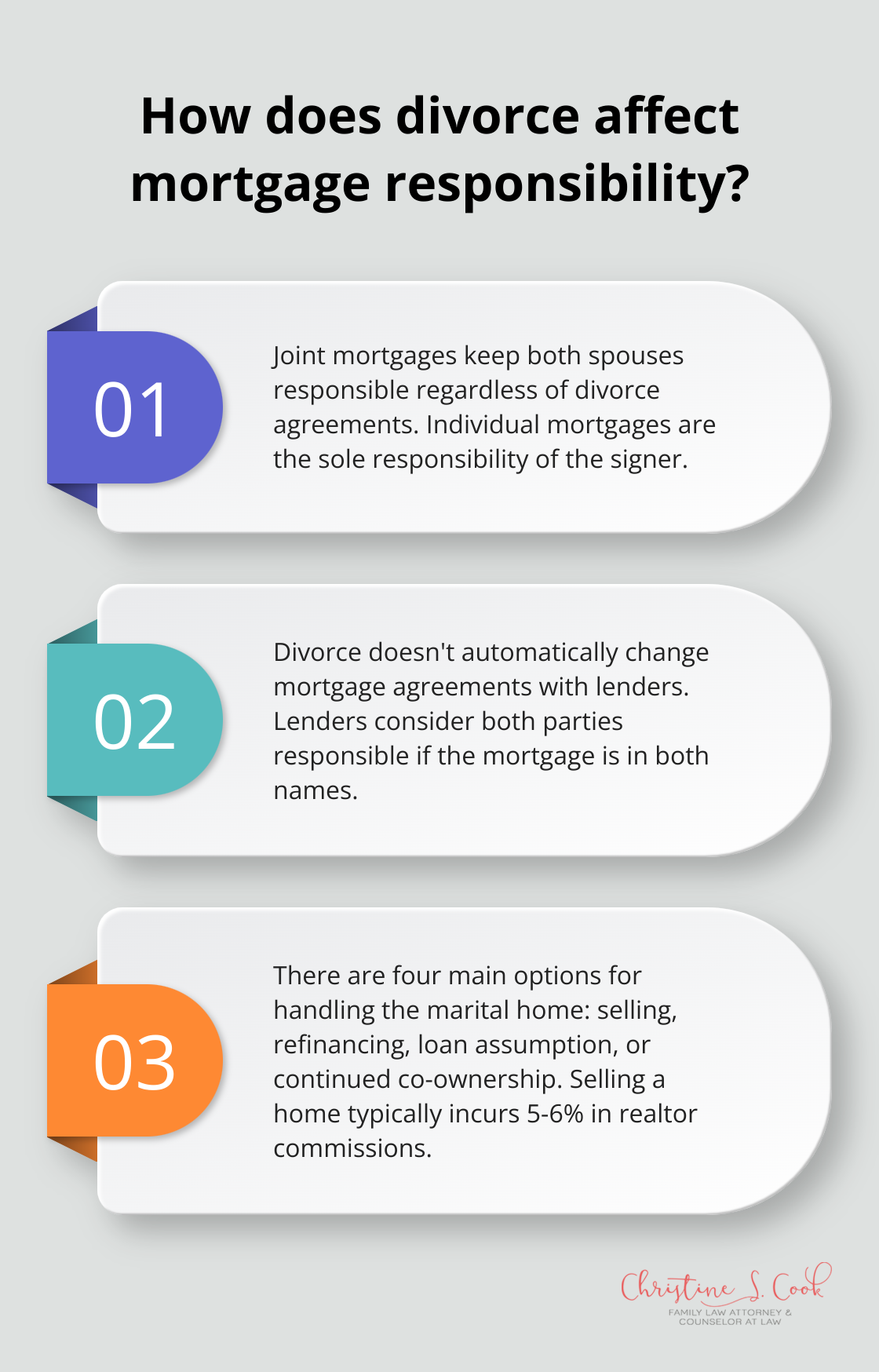

The type of mortgage you have significantly impacts your options during divorce. Joint mortgages keep both spouses legally responsible for the debt, regardless of who lives in the house or who agreed to pay in the divorce settlement. If your ex-spouse fails to make payments, your credit score could suffer, and you might face foreclosure.

Individual mortgages, however, are solely the responsibility of the person who signed for the loan. This doesn’t necessarily mean the other spouse has no claim to the property, especially if it was purchased during the marriage.

Divorce doesn’t automatically change your mortgage agreement with the lender. Even if your divorce decree states that one spouse will take over the mortgage payments, the lender still considers both parties responsible if the mortgage is in both names.

Divorce does not automatically lower your credit score. Instead, the financial decisions made during and after the divorce process play a more significant role in affecting credit scores.

Several ways exist to handle the marital home and its mortgage during divorce:

Each of these options has its pros and cons. The best choice depends on your specific financial situation, future goals, and ability to cooperate with your ex-spouse. We recommend consulting with both a family law attorney and a financial advisor to fully understand the implications of each option.

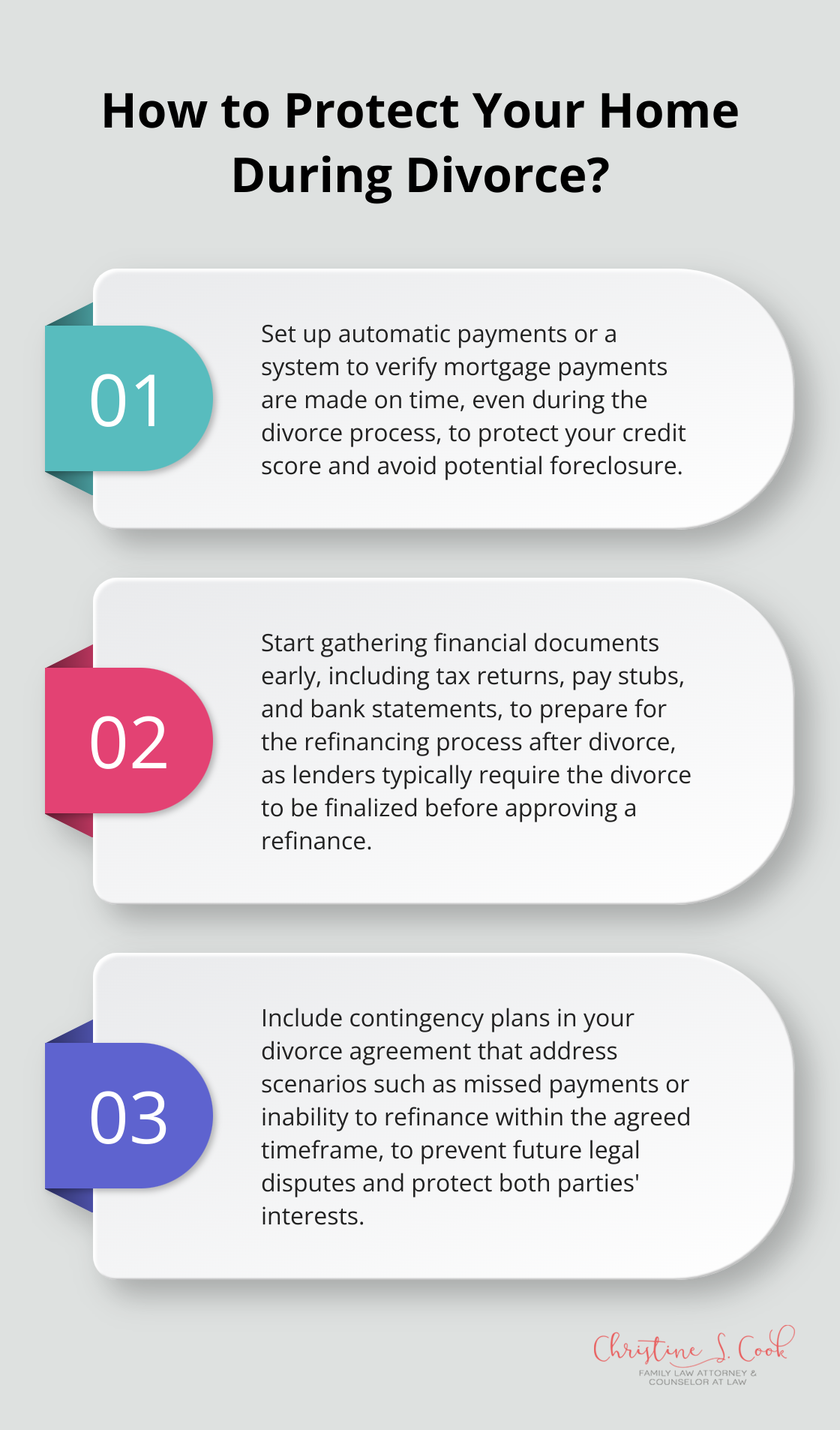

Regardless of which option you choose, you must protect your credit during and after the divorce. Make sure all mortgage payments are made on time, even if you’re in the process of selling or refinancing. If possible, set up automatic payments or a system to verify that payments are being made.

As we move forward, it’s important to consider the potential benefits and challenges of refinancing your mortgage after divorce. This process can offer a fresh start but also presents unique hurdles for newly single individuals.

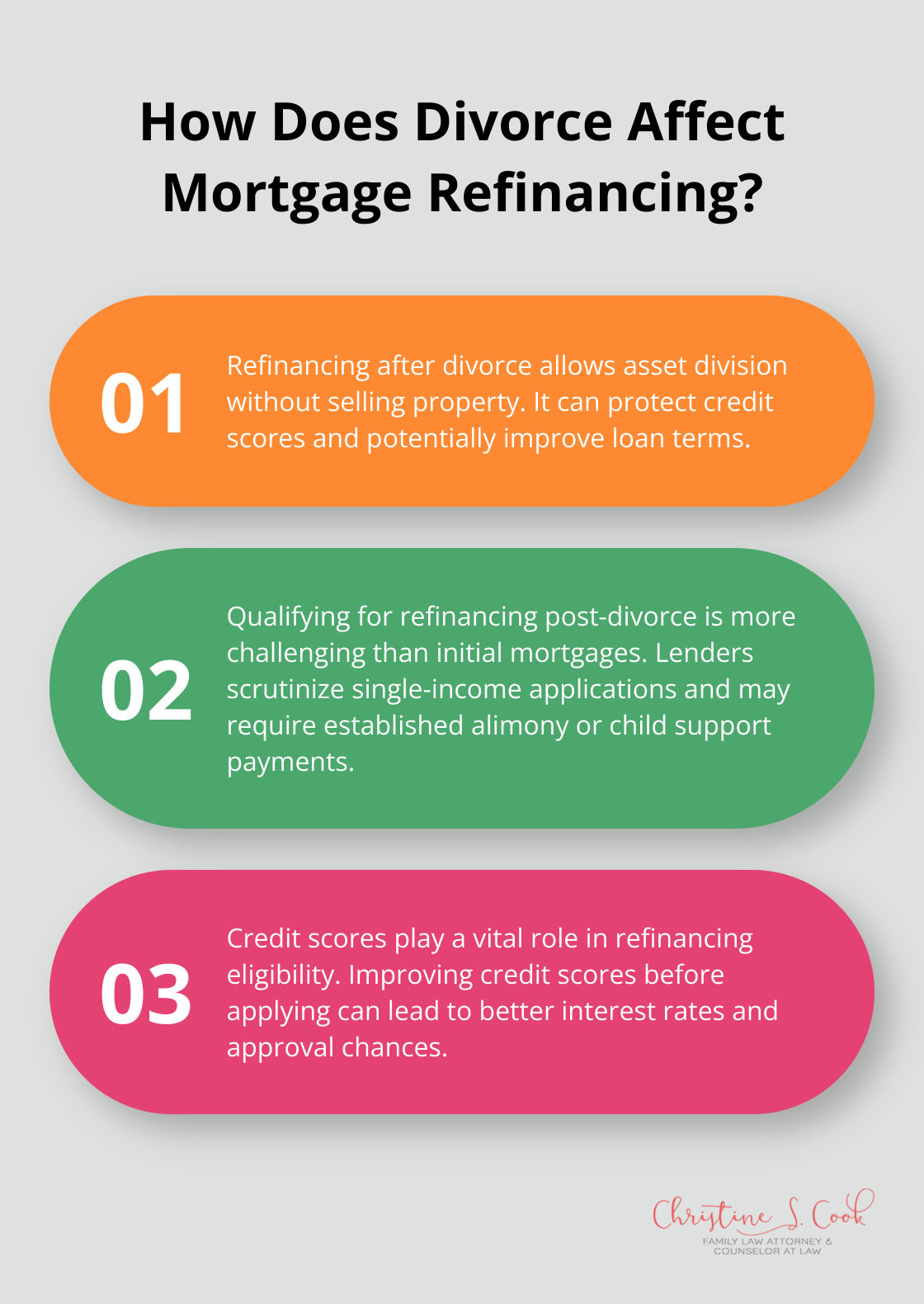

Refinancing after divorce offers several advantages. It allows divorcing couples to divide their real estate assets and liabilities cleanly without having to sell the property. This can protect your credit score from potential payment issues in the future. Refinancing might also lead to better loan terms, potentially lowering your monthly payments or interest rate. Additionally, it provides an opportunity to tap into home equity, which might be necessary to buy out your ex-spouse’s share of the property.

The refinancing process after divorce can present more challenges than your initial mortgage application. Lenders will scrutinize your financial situation closely. When you refinance, the former spouse remaining on the mortgage needs to qualify for the new loan using only their income and assets. If you rely on alimony or child support as part of your income, most lenders require these payments to be established for at least six months before considering them in your application.

Your credit score plays a vital role in refinancing. If your score has decreased during the divorce process, you might face higher interest rates or struggle to qualify. Take steps to improve your credit score before applying for refinancing. This might include paying down debts, disputing any errors on your credit report, and ensuring all bills are paid on time.

One common challenge in post-divorce refinancing is qualifying based on a single income. If you previously qualified for your mortgage with two incomes, you might find it difficult to meet the same standards alone. This is where working with a mortgage professional experienced in post-divorce situations can prove invaluable. They can help you explore all available options, including FHA loans or other programs designed for single applicants.

Another potential hurdle is the home’s appraised value. If your home’s value has decreased since purchase, you might not have enough equity to refinance. In such cases, you might need to explore alternatives like a cash-in refinance (where you bring money to the closing to meet the lender’s equity requirements).

Timing is also critical in refinancing after divorce. Many lenders require that your divorce be finalized before they’ll approve a refinance. This requirement ensures that all property division and financial responsibilities are clearly defined before new loan terms are set.

Try to start the refinancing process as early as possible. Begin by gathering all necessary financial documents, including tax returns, pay stubs, and bank statements. Be prepared to explain any gaps in employment or unusual financial transactions that occurred during your divorce.

Refinancing after divorce is not just about securing a new loan; it’s about setting yourself up for financial success in your new chapter. With careful planning and expert guidance, you can navigate this process successfully and establish a stable financial foundation for your future. As we move forward, it’s important to consider the legal aspects of mortgages in divorce settlements, which can significantly impact your financial future.

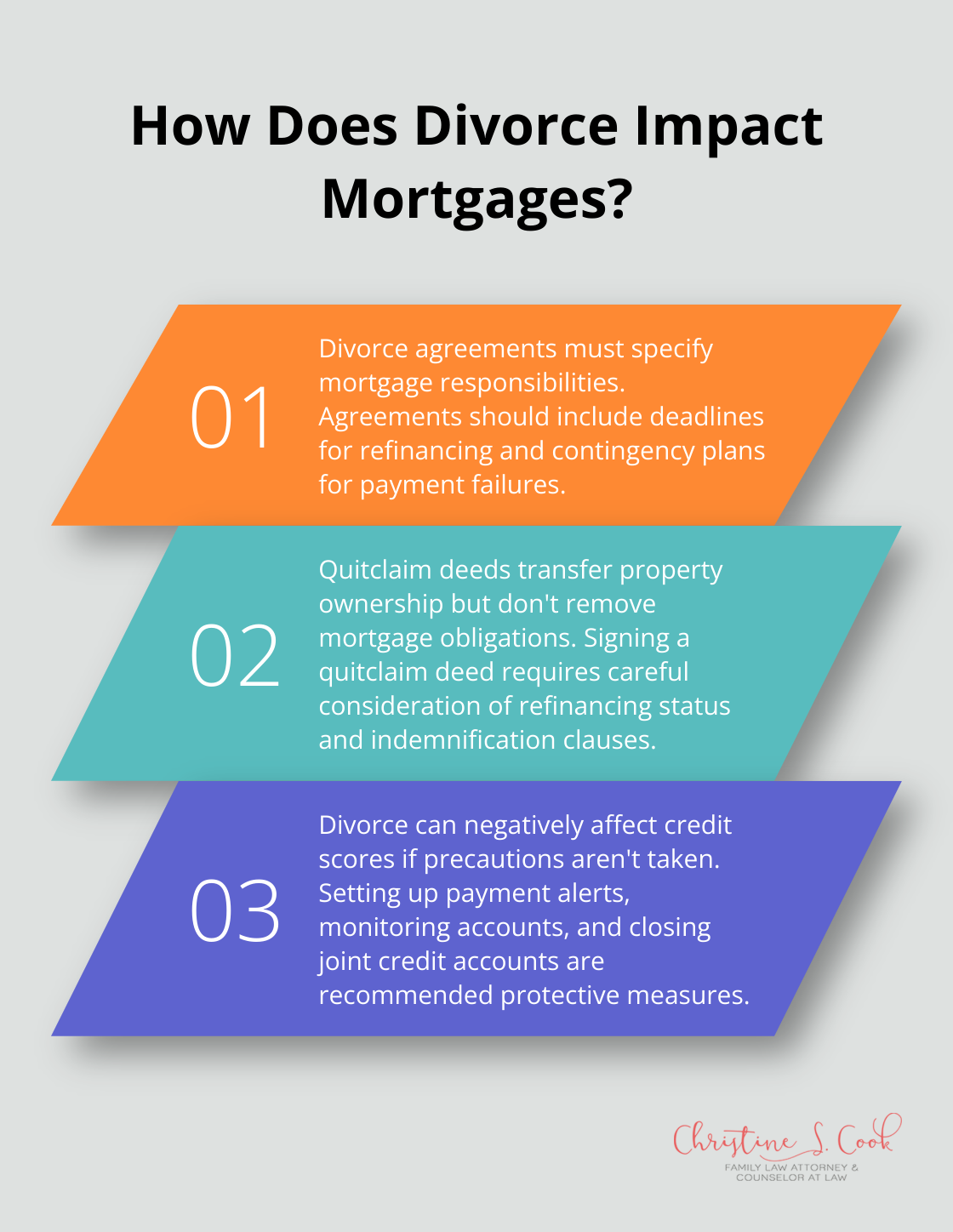

Your divorce agreement must state who will pay the mortgage and how you will handle the property. This clarity prevents future disputes and protects both parties’ interests. If one spouse keeps the house and assumes the mortgage, the agreement should specify a deadline for refinancing the loan into their name alone.

Include contingency plans in your agreement. Address what happens if the responsible party fails to make payments or if refinancing isn’t possible within the agreed timeframe. These scenarios need attention to avoid potential legal battles later.

Quitclaim deeds transfer property ownership in divorce, giving one party sole ownership of the property. This allows that party to sell or manage the property as they see fit. However, it’s important to note that a quitclaim deed doesn’t remove the other spouse from the mortgage obligation.

Before you sign a quitclaim deed, make sure the mortgage has been refinanced or you have strong protection in your divorce agreement. Some individuals negotiate clauses that require the spouse keeping the house to indemnify the other against any mortgage-related claims.

Divorce can damage your credit score if you don’t take precautions. Even if your ex-spouse agrees to take over the mortgage payments, late or missed payments will still affect your credit if your name remains on the loan.

To protect yourself, set up payment alerts or request access to the mortgage account to monitor payments. Some people establish escrow accounts for mortgage payments during the transition period (this can provide an extra layer of security).

Close joint credit accounts and establish credit in your own name as soon as possible. This builds your individual credit history and limits your liability for your ex-spouse’s debts.

Lenders aren’t bound by your divorce decree. They can still pursue you for payments if your name is on the mortgage, regardless of what your divorce agreement says. This underscores the importance of refinancing or selling the property if possible.

In cases where immediate refinancing isn’t feasible, some couples include clauses in their divorce agreements requiring periodic credit checks or proof of payment. This ensures the responsible party meets their obligations.

Navigating the legal aspects of mortgages during divorce often requires expert guidance. Family law attorneys (like those at Christine S. Cook, LLC) can provide invaluable assistance in drafting comprehensive divorce agreements that address all aspects of mortgage and property division. They can also advise on the best strategies to protect your financial interests throughout the divorce process and beyond.

Navigating mortgages during divorce requires careful planning and expert guidance. Joint mortgages remain the responsibility of both parties, regardless of divorce agreements. This fact emphasizes the need to address mortgage issues promptly and thoroughly in your divorce settlement.

Refinancing after divorce can offer a fresh start but also presents unique challenges. The legal aspects of mortgages in divorce settlements play a significant role in securing your financial stability. Clear agreements about property division and mortgage responsibilities help prevent future disputes.

At Christine S. Cook, LLC, we specialize in family law and can provide expert advice tailored to your unique situation. Our team understands the complexities of divorce proceedings and can help you navigate mortgage and divorce questions. We encourage you to seek professional guidance to protect your interests and make informed decisions about your financial future.