Divorce is one of life’s most challenging transitions, affecting your finances, emotions, and future in ways that demand careful attention. At Christine Sue Cook, LLC, we believe that divorcing well tips in Pensacola start with understanding what you truly need-both emotionally and financially.

The path forward doesn’t have to be adversarial. This guide walks you through compassionate, practical steps that protect your rights while keeping your dignity intact.

Divorce forces you to confront two realities simultaneously: the practical details of your financial situation and the emotional weight of major life change. Clients who address both dimensions upfront make better decisions and move forward faster.

Start by collecting the last three years of tax returns, current bank and investment statements, mortgage documents, and any business valuations. This isn’t busywork-it’s the foundation that prevents costly mistakes later. Florida uses equitable distribution, meaning assets divide fairly based on what you can prove you own, not necessarily equally.

You must identify every asset and liability, including life insurance policies, accounts held in your spouse’s name, and business interests. High-value items like real estate or retirement accounts require professional appraisals; skipping this step often costs thousands in settlement negotiations. Understand the tax implications before you agree to anything. A financial advisor can model the long-term costs of keeping versus selling specific assets and show you how timing affects retirement accounts or investment income.

The financial side is concrete, but your emotional state directly influences financial outcomes. Research shows that emotions drive worse decisions-particularly around custody and property division. Keep your feelings separate from your legal strategy.

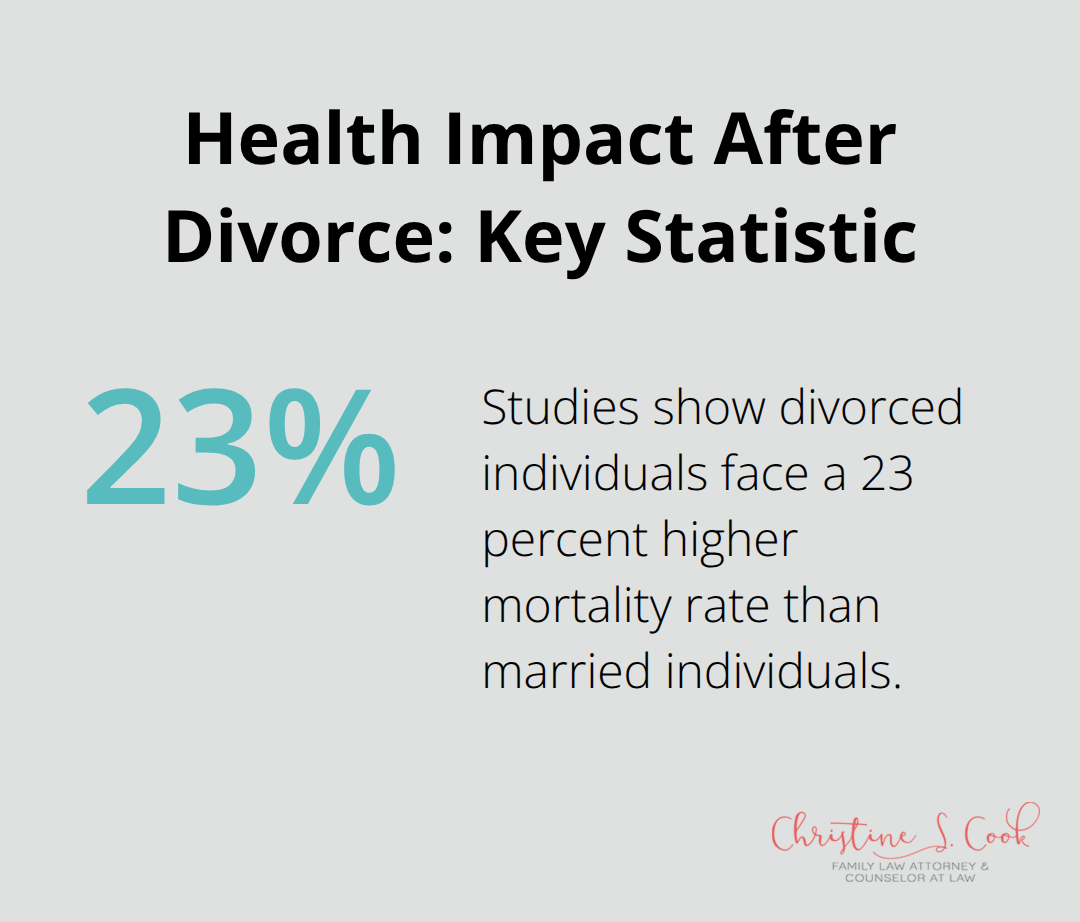

Divorced individuals experience stress-related health risks, with studies showing a 23 percent higher mortality rate than married individuals, so prioritizing self-care isn’t optional. Five minutes of aerobic exercise produces measurable anti-anxiety effects when you’re in crisis mode. This simple step matters more than you might think.

Track your involvement with your children now-the time you spend, activities you do together, and expenses you cover. This documentation supports custody discussions later and prevents disputes about who actually participated in your child’s life. Courts rely on concrete evidence, not assumptions.

You need a realistic support system to navigate what’s ahead. Pensacola has about 141 divorce-focused therapists offering in-person and online counseling options. Divorce counseling helps you process grief, anger, guilt, and anxiety while developing forward-moving strategies. If children are involved, co-parenting counseling teaches clear, cooperative communication with your spouse-the kind that protects your kids from conflict.

Initial sessions at local counseling centers typically cost around 175 dollars, with follow-up sessions at 125 dollars. These investments in your mental health directly reduce the emotional turbulence that leads to poor financial and custody decisions. With your financial picture clear, your emotions managed, and your support system in place, you’re ready to explore the approaches that will actually resolve your divorce.

Collaborative law and mediation represent fundamentally different approaches to resolving your divorce, and the choice between them shapes your timeline, costs, and relationship with your spouse moving forward. Mediated divorces typically cost $5,000-$9,000 total, while litigation can exceed $30,000 per person, a difference that matters significantly when you’re already managing the financial stress of separation. Collaborative divorce works through structured four-way meetings where both spouses, their attorneys, and neutral experts address issues directly rather than through court filings and discovery processes.

Mediation introduces a neutral third party who helps you and your spouse communicate about specific issues without the formality or expense of court proceedings. This approach excels when you disagree on particular points but share the goal of resolving them efficiently. Collaborative divorce includes neutral experts beyond attorneys, such as financial advisors and child specialists, who provide objective analysis on property division, tax implications, and parenting arrangements.

Collaborative divorce works best when both parties genuinely want an amicable separation, co-parenting remains a priority, and your asset complexity falls in the moderate range. Uncontested divorces in Florida typically finish in four to six weeks, while collaborative cases usually conclude in two to four months, giving you a realistic timeline for planning your fresh start. A financial neutral can model the long-term costs of keeping versus selling assets and show how the timing of retirement account division affects your future income.

If your spouse negotiates in bad faith or domestic violence is present, collaborative divorce typically fails and transitions to litigation, so honest assessment of your situation matters before committing to this path. Florida recognizes collaborative agreements as binding settlements, which protects you from post-agreement complications that sometimes arise in other informal processes.

The collaborative framework lets you structure settlements to fit your family’s needs, such as one parent keeping the home while the other receives assets of equal value, rather than forcing a one-size-fits-all court outcome. This flexibility means you control the outcome instead of accepting what a judge imposes. Your specific circumstances-whether you have minor children, significant assets, or complex business interests-determine which path makes the most sense for your situation and your family’s future stability.

Fair property division in Florida hinges on documentation and strategic timing, not assumptions about what’s yours. Florida uses equitable distribution, which means the court divides assets fairly based on what you can prove you own-not equally. This distinction matters enormously. A spouse who claims partial ownership of your business, retirement account, or investment property can drag out negotiations for months unless you have appraisals, valuations, and clear ownership records.

Professional appraisals for high-value assets aren’t optional; they’re the difference between settling quickly and losing thousands in contested negotiations. Before you sit down with your spouse or attorney, obtain written valuations for real estate, vehicles, retirement accounts, and any business interests. You must identify every asset and liability, including life insurance policies, accounts held in your spouse’s name, and business interests that others might overlook. A property division spreadsheet simplifies this process and ensures nothing gets missed.

Tax implications deserve equal attention to property values. Keeping the family home might feel emotionally right, but if your spouse receives retirement accounts of equal value, you’ll face substantial tax consequences when you withdraw those funds later. A financial advisor can model the real cost of keeping versus selling specific assets and show how timing retirement account division affects your income in ten or twenty years.

One parent keeping the home while the other receives investment accounts of equivalent value represents a legitimate settlement structure that works for many Pensacola families-but only if both parties understand the long-term financial picture. This flexibility means you control the outcome instead of accepting what a judge imposes based on incomplete information. Estate planning after divorce ensures your assets remain protected and distributed according to your wishes.

Child custody and support decisions require concrete evidence, not memories or best guesses. Courts use the best interests of the child standard, a legal framework that guides decisions regarding child custody and visitation. Florida’s child support formula uses both parents’ incomes and parenting time, so knowing the precise calculation gives you realistic expectations for negotiations.

Shared parental responsibility is presumed in Florida, requiring both parents to jointly decide major issues affecting the child-but if you cannot agree, the court will impose an arrangement based on documented evidence of each parent’s involvement. Create a detailed proposed parenting plan early, including custody arrangements, visitation schedules, and decision-making processes, before formal negotiations begin. This proactive approach prevents the court from controlling your family’s structure.

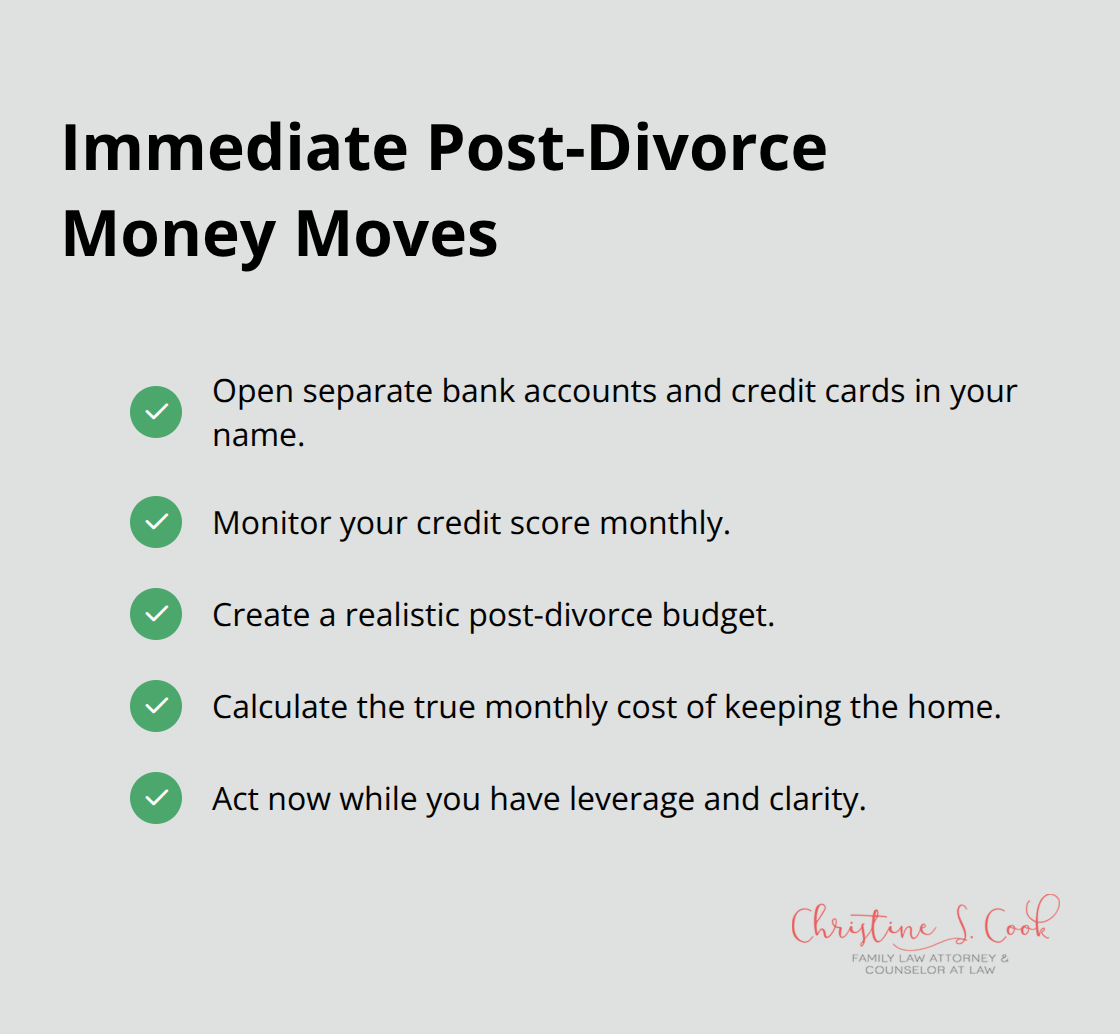

Post-divorce finances demand immediate, concrete action. Open separate bank accounts and credit cards in your name alone before the divorce finalizes; waiting until after creates complications with credit history and financial independence. Monitor your credit score monthly using free services, as divorce often triggers disputes that damage credit if you don’t address them promptly.

Create a realistic new budget based on your actual post-divorce income and expenses-not what you hope to earn or think you should spend. If you retained the family home, calculate the true monthly cost including property taxes, insurance, maintenance, and utilities; many people discover the home is financially unsustainable within months of divorce. Your fresh start depends on decisions you make now, while you have leverage and clarity about your financial situation.

Divorcing well tips in Pensacola start with making decisions from clarity rather than crisis. You’ve gathered your financial documents, understood your emotional needs, explored collaborative approaches, and protected your rights through documentation and strategic planning. These steps transform divorce from something that happens to you into something you actively shape, and the resources available in Pensacola support every dimension of your transition.

Divorce counseling helps you process the emotional weight of separation while building resilience for what’s ahead, and co-parenting counseling teaches you and your spouse to communicate respectfully about your children. Financial advisors model the long-term consequences of settlement choices you’re considering right now, and these investments prevent costly mistakes that accelerate your path forward. Your fresh start depends on taking action immediately: open separate accounts, gather your financial records, document your parental involvement, and create a proposed parenting plan before formal negotiations begin.

At Christine Sue Cook, LLC, we guide Pensacola families through this transition with compassion and strategic expertise. We combine collaborative law techniques with strong court representation when necessary, and schedule a free consultation to discuss your specific situation and the practical steps that make sense for your family. Your fresh start begins with one conversation.